The Full Story:

The market advanced for an eighth straight day through Wednesday, the longest streak since 2021. From here, some consolidation feels appropriate, and the rapid rise left some price gaps that need backfilling. A poor 30-year Treasury auction and more hawkish comments from Chairman Powell provided selloff sauce to close the week. However, powerful extended rallies tend to backfill and then continue as the below chart chronicles:

For this week, let’s zoom out a little further to see where the best risk/reward opportunities reside within this market for investors placing longer-term bets.

Allocation Deliberation

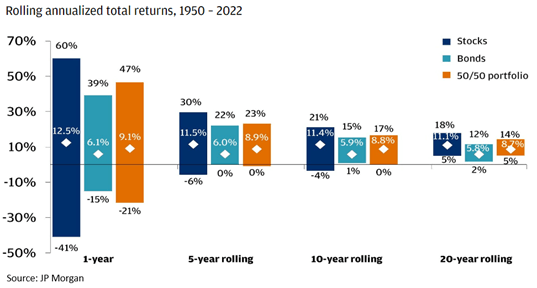

In the short run, markets are largely driven by tastes and preferences, making them particularly hard to predict. Fortunately, in the long run, as Buffett famously quipped, markets become a “weighing” machine rather than a “voting” machine. The outcomes become more predictable, and investable, as the below chart demonstrates:

Since 1950, stocks have risen as much as 60% and fallen as much as 40% within 1-year periods. A return dispersion of 100%. Over the course of 20-year rolling periods, they have compounded as much as 18% and as little as 5%. A much narrower return dispersion of 23%. Also, note there have been no negative periods! As they say, it’s not TIMING the market; it’s time IN the market that counts. For long-term allocators, being invested in stocks makes dollars and sense. But which stocks?

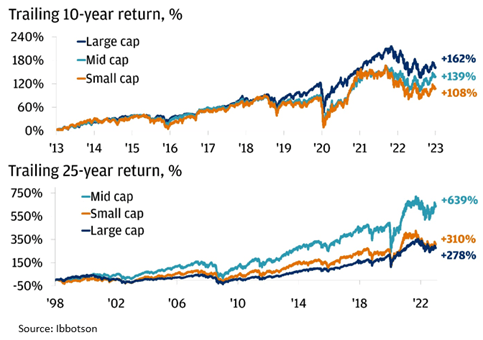

Buffet advocates investors hold Berkshire Hathaway while he is alive and then an S&P 500 large-cap index fund when he is dead. That’s reasonable advice, as it keeps investors invested and in a proven compounding machine. But should long-term investors expand allocations beyond the S&P 500? Over the last ten years, no. But over the last 25 years, yes:

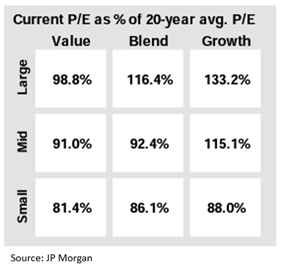

At this point in time, how can investors know which index will perform best over the next 10-25 years? Many argue that the best indicator for future returns is entry point valuations:

Currently, large caps sport valuations 16% higher than their 20-year average, while small caps hold valuations 14% lower than their 20-year average. By this comparison, investors should prioritize exposure to small-cap stocks over large-cap stocks within their portfolios.

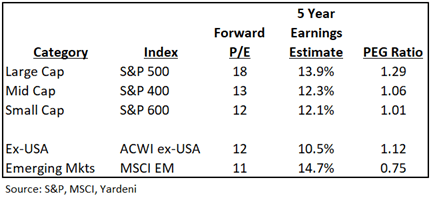

Many also argue that earnings growth makes for the best indicator of future returns. By this measure, investors should prioritize large-cap stocks over small-cap stocks as analysts expect large-cap earnings to compound at 13.9% over the long term while small-cap earnings compound at 12.1%. While it may surprise some that the large caps have a higher expected earnings growth rate than the small caps, much of that can be explained by the breakaway earnings power of the of the infamous Magnificent 7 stocks (Apple, Meta, Microsoft, Nvidia, Amazon, Google, Tesla). These stocks comprise 30% of the large cap index. Therefore, their earnings growth rate heavily influences the index growth rate, and their monopolistic power provides a significant advantage.

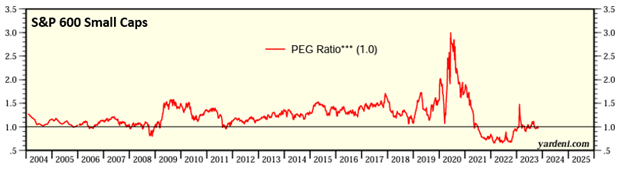

While we should all agree that time in the market makes dollars and sense, those who favor entry point valuations and those who favor earnings growth expectations disagree over where to invest now. Wouldn’t it be nice if we could combine the two measures to break the tie? Fortunately, we can. The P/E to growth ratio (PEG) divides current valuations by expected growth rates to calculate how much investors pay per unit of earnings growth. For example, at a PEG of 1.0, investors pay $1 in value for each $1 of earnings growth. Seems fair. But, if valuations climb or earnings rates fall, investors may have to pay $2 in value for each $1 of earnings growth. Seems pricey. Conversely, if valuations fall or earnings rise, investors may only pay $.50 for each $1 of earnings growth. Bargain! Let’s calculate the current PEG ratios on offer and see what computes (while our focus is on US large and small caps I have added the internationals in for kicks, inference clear):

By combining valuation and earnings growth, we find that while large caps may have faster earnings growth, the valuation discount in small caps makes them 30% more attractive. But while smalls hold the advantage in comparison with large caps, we also need to compare their current PEG with their own historical PEG to finish our analysis:

Based upon their own PEG ratio history, smaller cap stocks indices offer historic value. For investors placing savvy longer-term capital to work…the forgotten small caps should receive large consideration.

David S. Waddell

CEO, Chief Investment Strategist