The Full Story:

Last week, we discussed that, while the market’s math supported a year-end rally, the barrage of negative headlines overwhelmed the positive mathematics, leading to the rally’s incarceration. Liberation would only occur through improved headlines (for immediate resolution) or further declines in investor sentiment (for deferred resolution). Fortunately, recent headlines turned jubilant and liberated our rally!

Over the past week, the Dow gained 1600 points and the S&P 500 advanced by 6%. To further boost your weekend mood, we will share below some of the happy headlines with some technicolor commentary. Enjoy!

Last week, we received word that the US economy grew 4.9% in the third quarter. Consumer spending (amplified by Swifty Stimulus) powered the bulk of that advance. For US GDP growth to continue growing, consumers must continue spending.

While savings depletion and credit usage add to spending, it’s jobs and wages that drive it. Therefore, strength in the job market drives strength in spending, strength across the economy, and strength in corporate earnings.

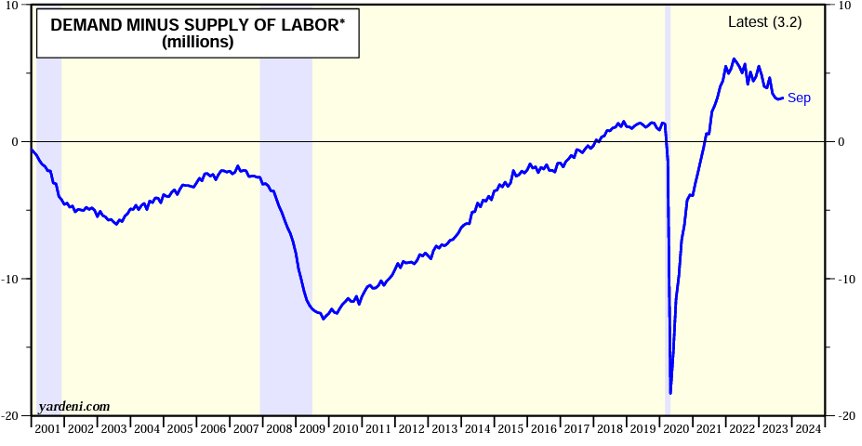

The headline above refers to the Job Openings and Labor Turnover Survey released on Wednesday by the US Bureau of Labor Statistics. According to the report, job openings rose slightly over the previous month to 9.6 million, equating to 1.5 jobs available for each unemployed worker. This remains a very strong job market, but the market has trended back toward more balanced conditions between worker supply and worker demand as the following chart demonstrates:

Powell has cited reclamation of equilibrium between labor supply and labor demand as one of his primary objectives. As you can see, while demand still outstrips supply, conditions are trending towards desired equilibrium.

As referenced in the headline, while jobs remain plentiful, quit rates and layoffs have hit pre-pandemic levels. Quit rates matter to economists because they measure worker confidence. You will only ballad, “take this job and shove it” if you know that another, better paying job is available.

The less workers believe that the grass is greener, the fewer quits and wage renegotiations. Employers also pink-slipped 1% of laborers, consistent with a steady but forgiving environment. So, while the economy added jobs in September, quit rates and layoff rates suggest easing wage pressures. This Goldilocks report gets a 10 out of 10.

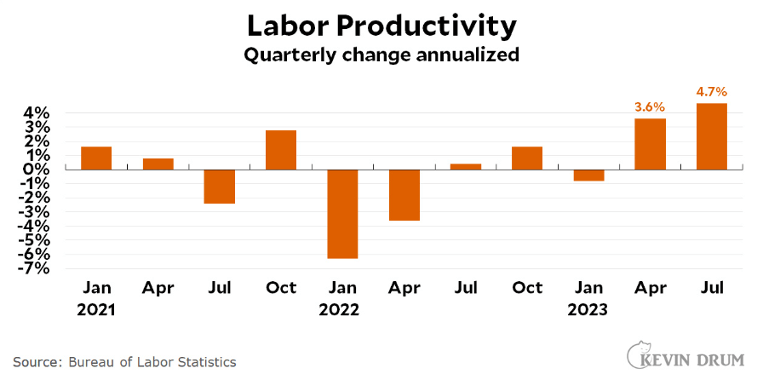

Reinforcing the JOLTS suggestion of softening wage conditions, the Labor Department also released its quarterly report on productivity and unit labor costs. Within the 3rd quarter, unit labor costs increased 3.9%, but labor productivity surged by 4.7%. This means corporations generated 4.7% more stuff and only had to pay workers 3.9% for it. That translates into a decline in unit labor costs of 0.8%!

In economics, nothing provides more benefit to society than increasing productivity. Productivity gains power quality of life gains as less input generates more output. Productivity in the US has surged over the last two quarters to its highest levels in 15 years (save the pandemic surge due to mass layoffs) as labor and supply shortages forced companies to innovate processes and renovate organizational structures:

Mix in the early integration of AI, and the US may have just entered a major productivity upgrade cycle. As corporations become more efficient, economies grow without corresponding inflation growth. This Goldilocks report also receives a 10 out of 10.

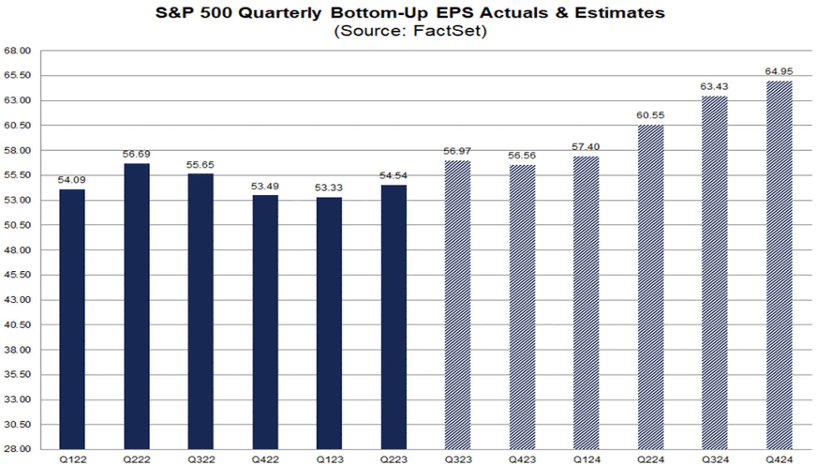

Strong economic growth, high productivity and lower wage pressures should alchemize into higher corporate earnings reports. And so, they have! S&P 500 earnings likely hit record levels last quarter. So far, 341 of the 500 companies within the S&P 500 have reported with aggregate earnings growth now projected at 3.4% versus the -1% anticipated before the reporting season began. Furthermore, the resumption of growth rather than declines should continue unabated next year as seen in the estimates below:

Using simple arithmetic, if we annualize the Q4 2024 projection of $65 in earnings per share for the S&P 500, we get $260. With interest rates cooling back toward 4.5% on the 10-year, the market could easily support a 19x P/E.

Multiplying $260 by 19 produces a potential price level near $5,000 for the index next year. We closed Friday near $4,350. After three consecutive quarters of negative earnings growth, the initiation of positive growth this quarter, and for quarters to come, receives another Goldilocks 10 out of 10.

Of all the happy headlines this week, none provided more rally fuel than this one. A fierce debate has broken out among economic disciplinarians around the ability of the global marketplace to finance ballooning fiscal deficits in the US. The spike in long-term interest rates over the past quarter corresponded with a large surprise in scheduled treasury auctions, and underwhelming demand for longer dated maturities. Fortunately, the Treasury took notice.

On Wednesday, the Treasury announced that it will issue fewer bonds than expected this quarter and will weight issuance toward shorter dated maturities, removing upward yield pressure on longer-dated maturities. The yield on the 10-year bond dropped from 4.8% to 4.57%, sparking a stock market surge as lower yields accommodate higher valuations and lower funding costs boost earnings potential. We do not comment on the Treasury Refunding releases often, but this Goldilocks market mover received a 10 out of 10.

Bravo, Chairman Powell! Your FOMC comments and press conference provided EXACTLY what this rally needed to break out of jail. To summarize his comments:

- Disinflation across the economy remains on trend.

- Labor market growth remains on trend.

- Labor inflation has now returned to levels consistent with our 2% inflation target.

- Labor demand and supply factors are rebalancing, a healthy precondition for disinflation.

- GDP growth rates are averaging out below potential, a healthy precondition for disinflation.

- We do not see a recession on the horizon.

- Longer-term inflation expectations remain near our 2% target.

- The recent rise in the dollar, the rise in yields, and the fall in the stock markets have tightened financial conditions organically, reducing tighter policy requirements.

- We do not see any need to raise rates further or cut rates at this time.

- We do not believe the events in the Middle East will impact the economy.

Standing ovation, please! Often, Fed Chairs tilt their comments to punish or reward markets. What made this testimony so compelling was Powell’s synthesis of truth. As seen in the headlines above, his comments align with the positive indicators of growth and disinflation recently reported. The market needed a jolt of confidence, but this was no manipulation. I will end this section with the following Goldilocks revelation he made during his 10-out-of-10 press conference:

“Well, I think everyone has been very gratified to see that we’ve been able to achieve, you know, pretty significant progress on inflation without seeing the kind of increase in unemployment that has been very typical of rate-hiking cycles like this one. That’s historically unusual and a very welcome result.”

Indeed, Mr. Powell!

David S. Waddell

CEO, Chief Investment Strategist

Source: Yardeni, FactSet, Bureau of Labor Statistics

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. Past performance does not guarantee future results.