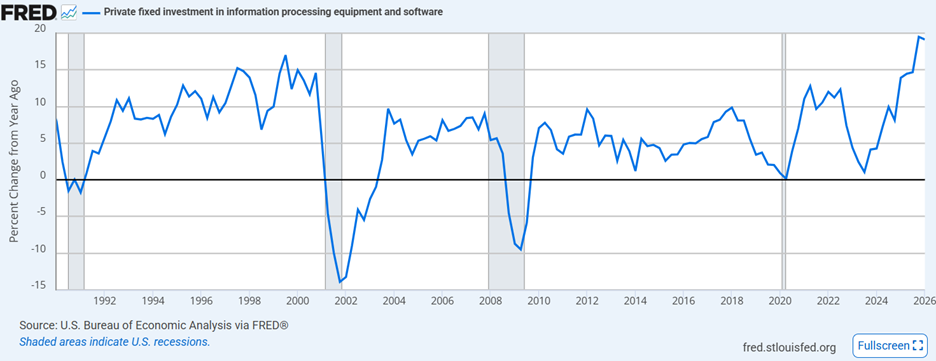

Markets hit new highs again this week as powerful earnings releases and promising war negotiations cheered investors. The AI Revolution rivals any in world history as demand projections for computing power seem infinite. During the industrial revolution, companies competed for workers. During the AI revolution, companies are competing for compute. Some might even say blindly so as not to be left behind, leading to frenzy-like activity. In line with this thesis, consider the profound growth rate in IT investment today across the US economy:

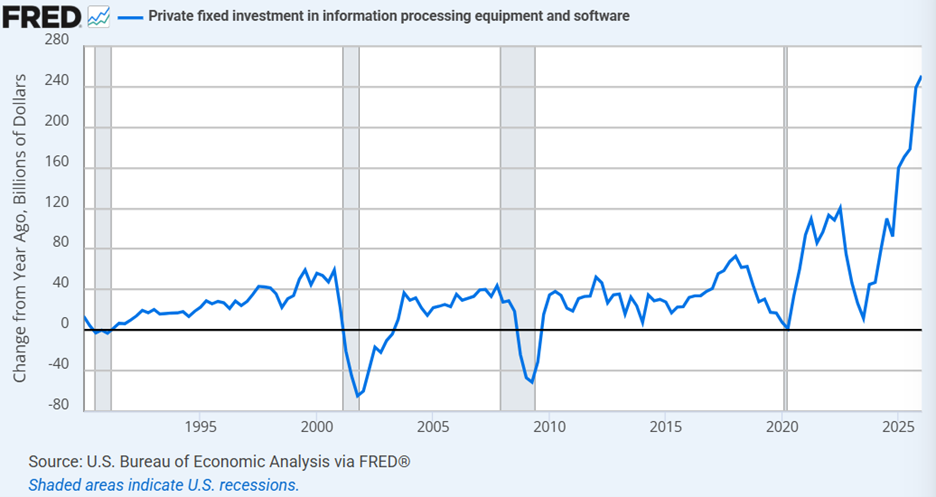

In the mid-1990’s, IT investment grew between 10-12% annually, reaching a peak to offset the Y2K threat at 17%. Following COVID and the inception of the virtual office economy, IT investment grew 10-12%. Today, IT investment is growing by nearly 20%, well above any rate seen over the period. Moreso, that growth rate comes on top of an already sizable base. When adjusting the chart above for dollar change rather than percentage change, the investment scale becomes even more notable:

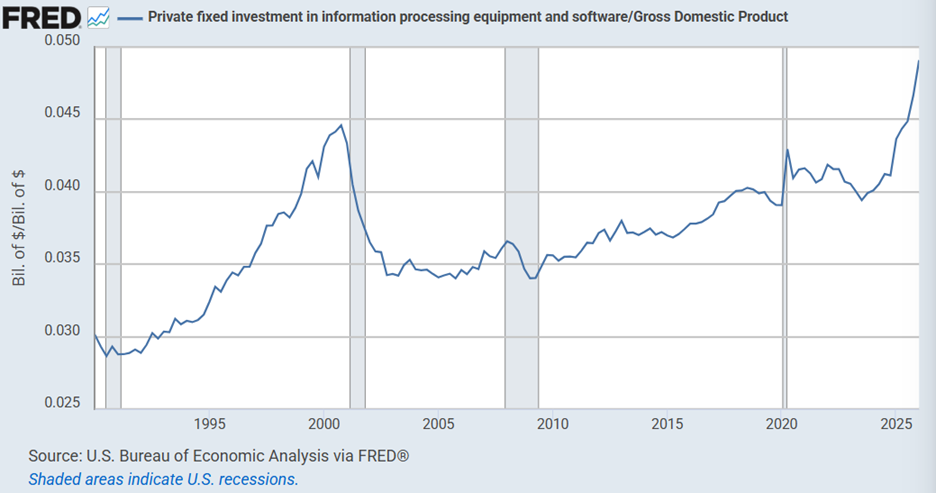

And because of the historic magnitude of this investment cycle, the influence and economic stimulus of IT investment within the US economy continues to grow in magnitude as well:

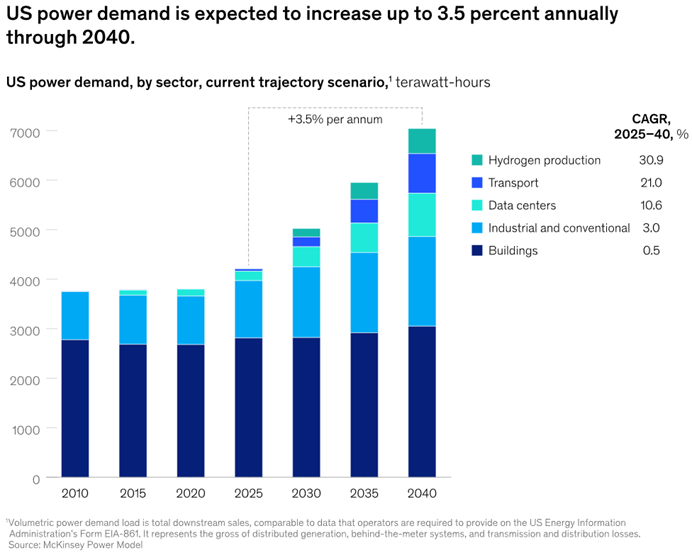

IT investment now accounts for 5% of the entire US economy. In other words, the US is allocating $1 out of every $20 the economy produces to IT investment. In addition to becoming such a large allocation, IT investment has become the largest contributor to US GDP growth, contributing 67% of Q1 GDP growth, far beyond anything seen before. And because the investment boom is largely hardware related, it trickles down the entire supply chain from high tech fliers to infrastructure and power suppliers. Consider the sheer amount of electricity demand being created by the AI revolution:

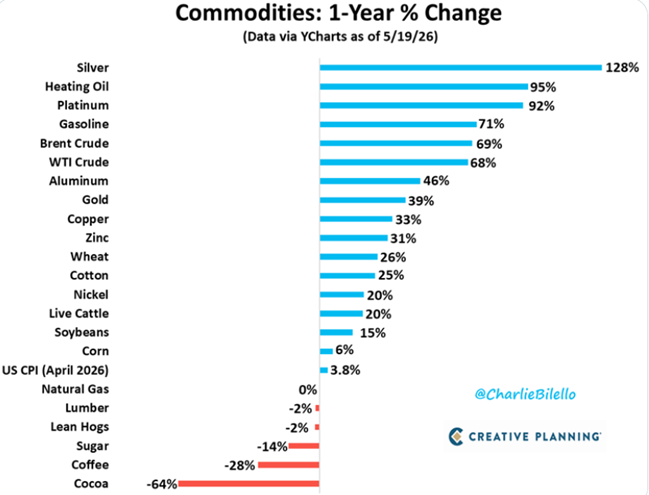

All this hardware, construction, and power demand creates supply shortages and price pressures across various commodities:

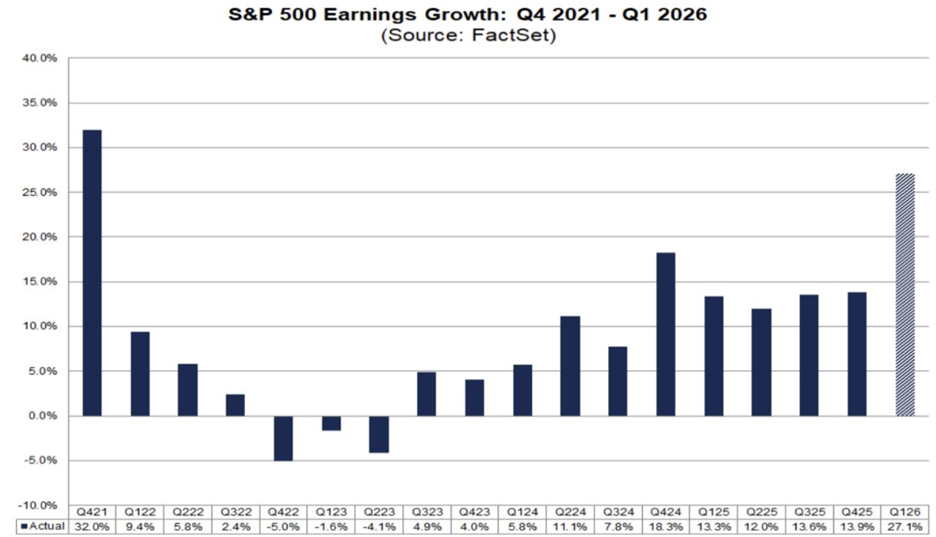

This brings us to corporate earnings, which surged in the first quarter to levels seldom seen outside of post recessionary turns:

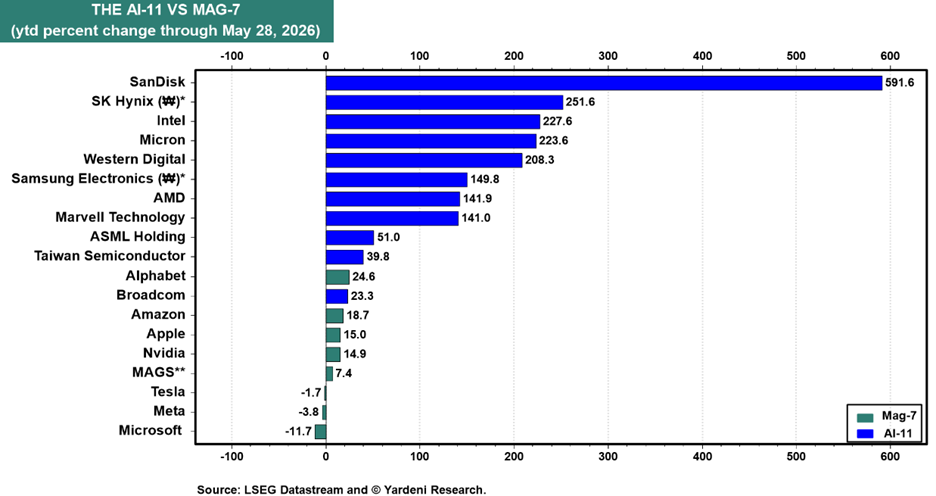

Excited yet? The combination of insatiable demand for compute, deep pools of earnings and capital to finance CAPEX, and shortages across the economy have unlocked generational levels of corporate profits and investor returns. Lastly, given the “structural” nature of the AI Revolution rather than the “cyclical” nature of typical technology cycles, valuations for more cyclically oriented companies like Micron and SanDisk should rise to levels of less cyclical companies like Microsoft and Apple. This perspective calls not for a rally in these cyclical players but a complete repricing given their transformation from episodic businesses into stalwart annuity businesses!

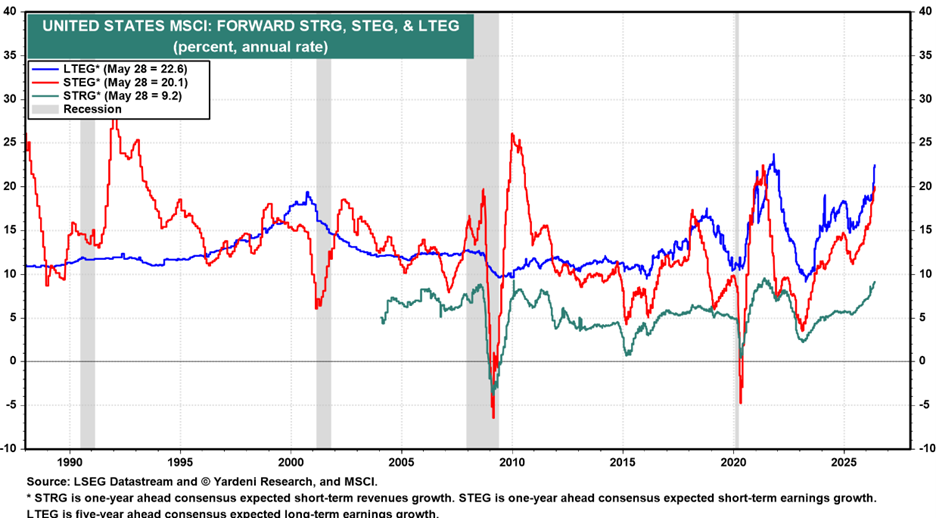

Furthermore, analysts have mapped the “structural not cyclical” earnings benefits across the entire US market complex.

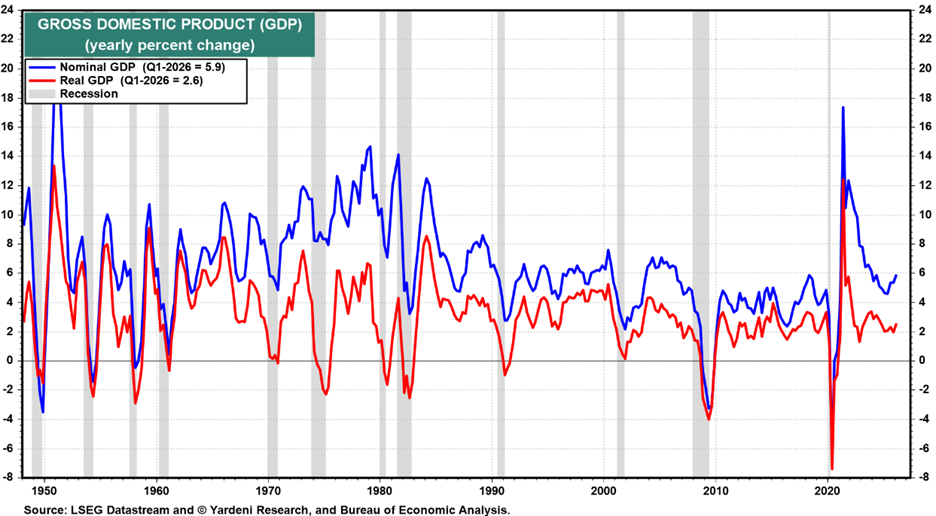

Of all the charts presented, this is perhaps the most profound. According to analysts, over the next 5 years (the blue line) US public companies will experience earnings growth of nearly 23% annually. This requires an historic combination of revenue growth and profit margin growth to get there. Corporate revenues, or sales, largely track nominal GDP growth (growth + inflation since revenues are quoted gross of inflation). In Q1, US nominal GDP grew a spirited 5.9%, towards the top end of its recent range:

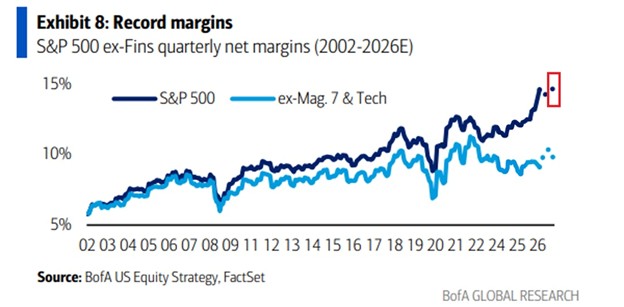

To accommodate the revenue growth required over the next five years, nominal GDP would have to rise substantially back to levels we haven’t seen since the 1970s. Absent that level of nominal GDP growth, profit margins would have to expand substantially, which has been occurring in tech land but not as obviously in non-tech land:

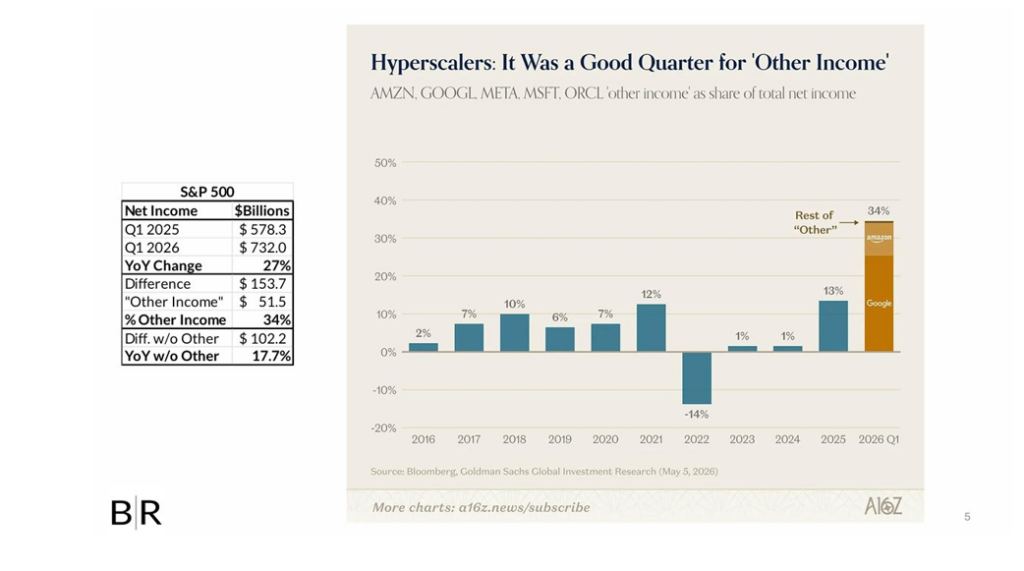

For profit margins to surge enough from here to overcome nominal GDP and revenue constraints, non-tech participants will need to double their operating efficiencies to meet these wildly ambitious forward earnings forecasts. Possible perhaps, but not probable. Lastly, corporations could source additional earnings power from “other income” and accounting adjustments. For instance, last quarter the circular financing within the hyper-scalers (swapping cloud capacity for Anthropic and Open AI stock), led to mark-to-market gains that accounted for perhaps a third of overall Q1 earnings growth:

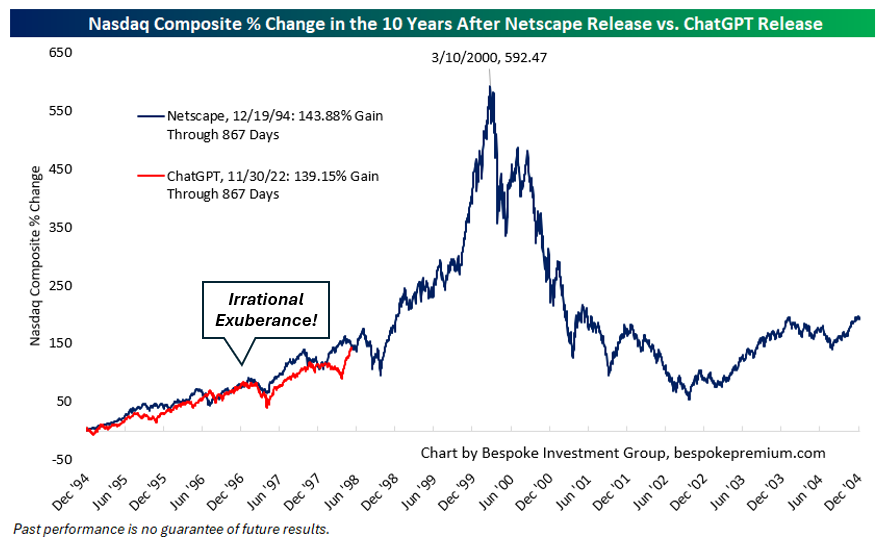

As long as these trillion-dollar startups double their valuations each year over the next five years, “other income” accounting adjustments will contribute significantly. Consider the mark-to-market benefits for the Japanese Nikkei at the end of the 1980s! Absent this accounting alchemy, revenues and margin expansions will likely fall far short of analyst expectations and terms like “insatiable demand” and “unlimited pricing power” will once again become siren calls leading investors into the rocks. While that seems inevitable to us, the timing of comeuppance remains unknowable. Recall that Greenspan labeled the last episode of market exuberance “irrational” three years prior to its demise. While today’s AI Revolution may not be immune to cyclicality, it’s clearly a super cycle poised to run beyond rationality, if it hasn’t already. We will monitor the macro cues for what’s reasonable and watch the unreasonable, from afar.

Have a great weekend!

-David

Sources: Federal Reserve Bank of St. Louis, McKinsey & Company, Charlie Bilello & Creative Planning, Factset, Yardeni Research, Bank of America Research, Bianco Research, Andreessen Horowitz, Bespoke Investment Group

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.