The stock market hit new highs again this week as earnings rose, oil fell, and rates retreated. While we talk about “the market” each week, it’s been a bit since we have disaggregated it for discussion. For our own purposes we disaggregate “the market” into the following categories: geography, investment style, market cap (company size), and sectors. This week let’s do a brief survey of the disaggregated returns and draw some conclusions.

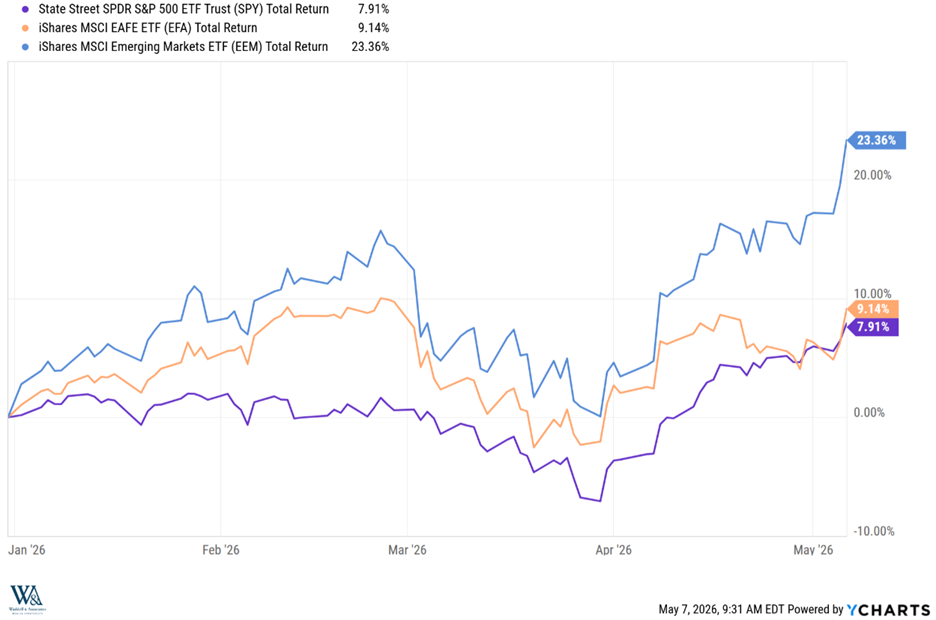

Geography

Despite the headlines that Epic Fury has inflicted more pain on the offshore economies than our own, the investment returns read otherwise. While the US market (represented here by the S&P 500) has risen 8% year to date, the developed international markets (represented by the EAFE) have risen 9%, and the emerging markets (represented by the MSCI EM) have risen 23%. If we disaggregate further, even more surprises arise. For instance, the Israeli stock market (ETF: EIS) has climbed 24% this year, perhaps because wars ultimately have winners. International investors must also consider currency fluctuations. Typically, geopolitical frictions trigger capital flights to quality, boosting the USD. This happened in the initial phases of Epic Fury, but this has since reverted with the US Dollar down 0.5% on the year, adding a slight uptick to international return calculations. In all, the Geographic returns remind us that headlines and bottom lines often do not correlate.

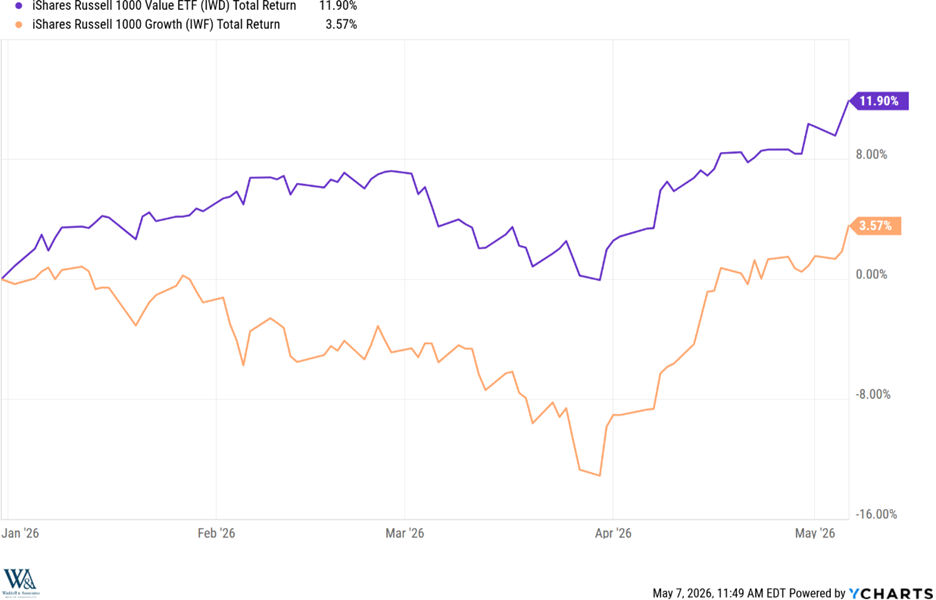

Investment Style

Investment bias essentially established two investment styles. Those who want to invest in what’s cheap today became known as “value” investors and those who want to invest in what will become bigger tomorrow became known as “growth” investors. Berkshire Hathaway is the largest holding in the value index above (ETF: IWD), while NVIDIA is the largest holding in the growth index above (ETF: IWF). Because the AI trade has become so dominant growth indices rely heavily on NVIDIA and the Magnificent 7 for direction. These stocks struggled early in the year as investors questioned the viability of the capex spending and the trajectory for their earnings. This created an advantage for the more “knowable” value style companies trading at lower P/E’s with lower earnings expectations thresholds to overcome. However, enthusiasm for growth has returned with the war winding down, rate cuts on approach, and stellar earnings results from the Magnificents. As clearly shown, there are no “right” investment styles, only oscillations between them.

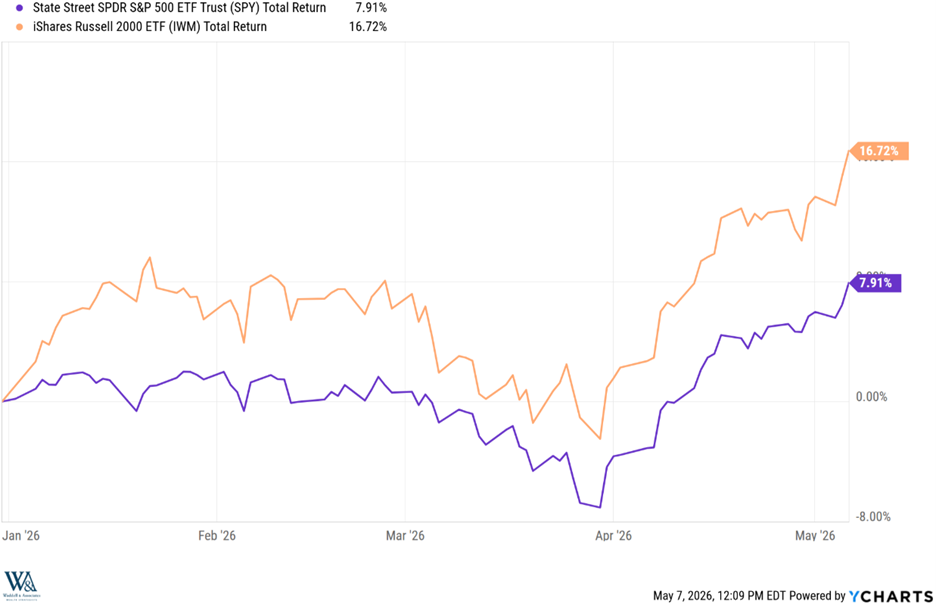

Market Capitalization

In theory, smaller companies grow faster than larger companies due to scale advantages, which should support higher investment returns. While this has been true over a long period of time, it has not been true over the last mega tech decade. Over the past 10 years the S&P 500 large cap index (ETF: SPY) has returned 320% for investors while the Russell 2000 small cap index (ETF: IWM) returned 194%. That yawning divide has left many who believe in reversion to the mean to favor small over large more recently. Their bets have been rewarded as the smalls have gained 17% on the year versus 8% for the bigs. Will this continue? Perhaps. The combination of economic acceleration and lower short-term interest rates should support the small co earnings complex, while valuation convergence continues. But should the macros deteriorate, it’s likely the smalls will as well. They historically trade as volatility enhancers which can be great on the upside… but less great on the downside.

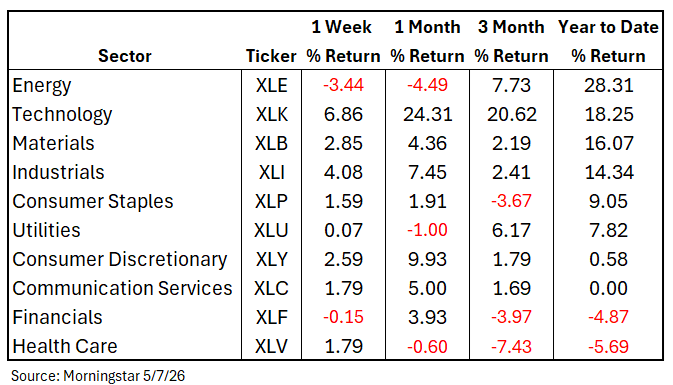

Sectors

Sectors often make the best thematic tracing vehicles. Think the economy is going to accelerate? Consider owning those most cyclically oriented like energy, materials, and industrials. Think the economy will recess? Consider owning those most defensive like consumer staples, healthcare, and utilities. These tend to be reliable bets unless something peculiar occurs like regulatory changes for healthcare or AI Capex demands making utilities behave like growth stocks. On the year, the cluster of energy, technology, materials, and industrials in the lead suggests a broad-based economic advance. Consumer discretionary has lagged amidst concerns over energy spending displacement and financials lack an AI narrative and the promise of rate cuts. From here, resolution in Iran will pressure energy lower, but other cyclicals higher. Financials look cheap with loan volumes rising and rates falling, perhaps poised for a move. Healthcare performance resembles the healthcare sector overall: sluggish and confusing.

Taken together, the complex shows some return variations but conformity with a theme. The US economy isn’t recessing anytime soon, the capex cycle isn’t ending anytime soon, and this bull market isn’t ending anytime soon.

Have a great weekend and Happy Mother’s Day!

-David

Sources: YCharts, Morningstar

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.