Markets have finally fulfilled their seasonal promise of declining as we approach All Hallows Eve. Those who have known us for a long time know that we tend to dollar cost average capital received mid-year into Halloween given typical summer doldrums and early fall apprehensions. We altered our emphasis on seasonality a bit this year given the Trumpian overlay, but historical odds favor September/October swoons that initiate November/December boons. Will that occur this year, or is our only fear the fear itself?

The Fear to Fear

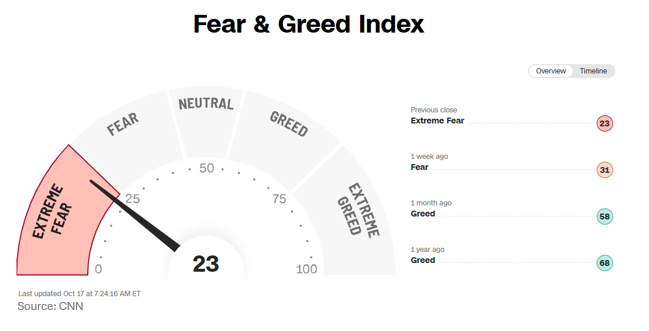

CNN business compiles several sentiment readings into a simple gauge measuring fear and greed. The current level marks the most fearful since Liberation Day. Most underlying factors show short-term shivers driven by recently harrowing headlines, but longer-term measures like market breadth reveal a more concerning rot.

Technically Stanky Breadth

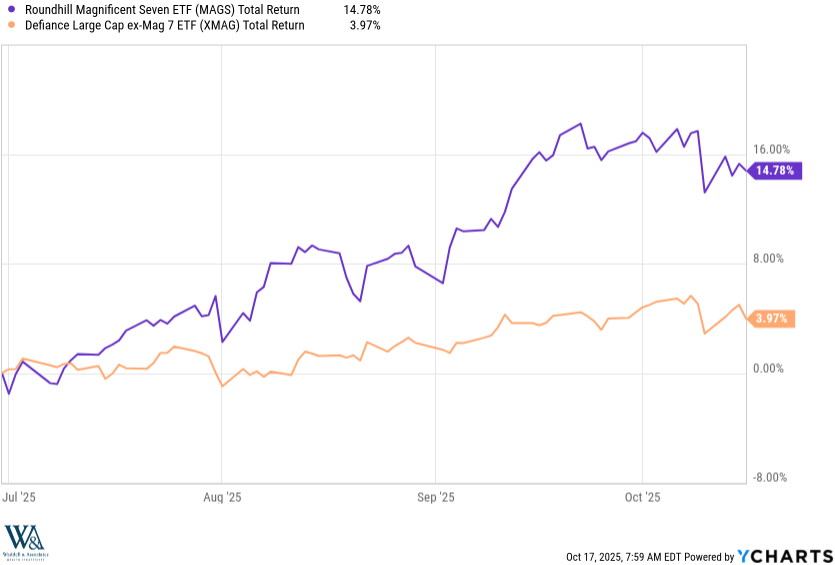

Market breadth measures trader conviction. More confident markets show more bet diversification and higher breadth, while less confident markets show more bet concentration and lower breadth. With the Mag 7 now commanding over 35% of total S&P 500 capitalization, moves higher in that cohort alone can drive indices to new highs despite a sideways drift for the remaining 493, as the chart below indicates:

With the 493 trending sideways, any Mag 7 misstep can exacerbate downside dips, which has been the case over the past week. A lack of non-Mag conviction paired with Mag 7 jitters presents the perfect target for a technical sell-off.

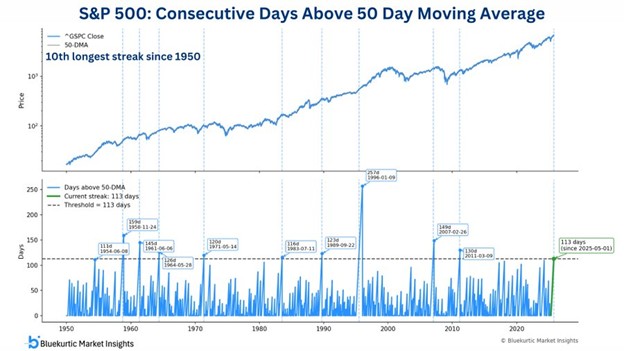

The recent rally off the April lows has strung together a string of superlatives. For instance, the amount of time the S&P 500 has spent above its 50-day moving average rivals some of the longest streaks in last 50 years. The last unblemished rally of this duration occurred nearly 15 years ago making this a rally in search of retraction. Tech bubble blabber, Trumps tariff tantrum, shutdown shutters and credit consternations provide ample kindling for technical burn-off:

The chart above plots index movement off the highs. While the non-Mags in orange may not have captured the buying momentum of the Mag 7 on the upside, they also didn’t capture the selling momentum on the downside, suggesting fundamental breadth may not be as concerning as technical breadth.

Fundamentally Minty Breadth

As Buffet famously said in referencing sentiment and technical market factors, “in the short run the market is a voting machine, but in the long run it’s a weighing machine.” Translation: markets react to technical influences but ultimately follow the fundamentals.

From a fundamental perspective, earnings production for the Magnificent 7 has been otherworldly compared with everything else, making their outperformance since the October 22 lows well-earned. However, as we peer forward, earnings breadth should improve markedly. Note that in 2026, the expected earnings differential between the Mag 7 and non-Mags within the S&P narrows, drawing more attention to the valuation differential of 30x for the Mag 7 vs. 20x for the non-Mags. Advantage non-Mags. Further down the cap spectrum, the S&P 1000 small and midcap index could see even faster earnings growth at a valuation of 15x vs. 30x. Advantage Smidcaps. In fairness, markets have tended to underestimate the strength of Mag 7 earnings growth and overestimate the strength of non-Mag earnings growth since this bull began, but that may be changing:

For the first time since 2021, analysts are raising their forward revenue and earnings estimates on over 85% of S&P 500 companies. In our opinion, this accounts for the stimulus smorgasbord of monetary stimulus, fiscal stimulus, de-regulatory stimulus, currency depreciation stimulus, and AI capital expenditure stimulus on approach. That’s a wide array of stimulus programs supporting a wide array of earnings programs as seen in the early reporting this earnings season. Fifty-one of the S&P 500 companies have reported so far with 82% of those outperforming estimates. A third of S&P 500 financial companies have reported earnings, 90% have outperformed estimates, and none are in the Magnificent 7.

Lastly, while the rally in Gold has attracted fascination of late, it’s the rally in Small Caps despite bad technical breadth that deserves it more. While the Mag 7s have well outperformed the non-Mags since July, the Russell 2000 small caps have well outperformed them both:

Enjoy your Sunday!

-David

Sources: YCharts, Yardeni Research, Franklin Templeton, Bluekurtic Market Insights, CNN Business

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.