Oil Prices?

Iran has recently increased its defiance. Trump has recently increased his threats. Onshore oil prices peaked this week roughly 10% below their wartime high while offshore oil prices peaked 10% above their wartime high. The longer the conflict lasts, the more depleted oil inventories become, and the more upward pressure exerts on price:

Oil traders have to balance supply restriction and demand destruction, with conflict resolution odds, to project prices into the future. Here are the changes across the Brent crude futures curve:

Brent futures price in more Middle East disruption given its seaborn nature. Here in the US, we quote West Texas Intermediate prices as we supply our own oil onshore, largely insulating us from the Middle East disruption. This has created a $10 per barrel savings for US citizens compared with the curve above. Nonetheless, across the curve, prices have shifted higher, accounting for falling confidence in swift war resolution. In sum, probability has risen that oil prices will be higher for longer as negotiation impasses persist, increasing stagflation risks and stock market vulnerabilities.

Capex Pace?

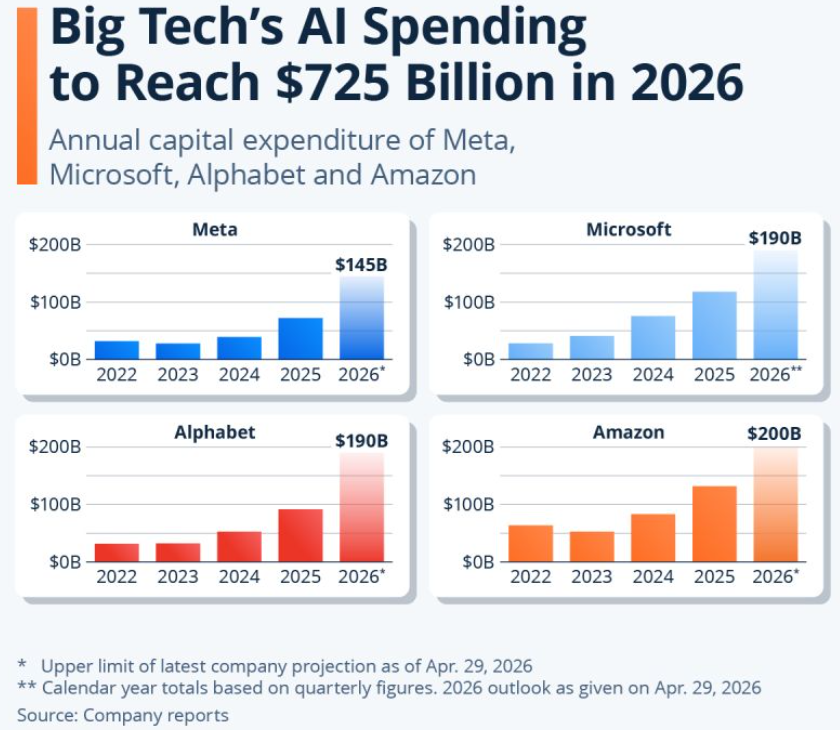

Five of the Magnificent 7 (Apple, Amazon, Google, Meta, Microsoft, Nvidia, Tesla) reported earnings this week. Each reported better earnings than analysts expected, as usual. More importantly, the cohort raised their AI capital expenditures estimates for 2026 from roughly $650 billion to $725 billion. Note not only the scale, but also the significant acceleration this year:

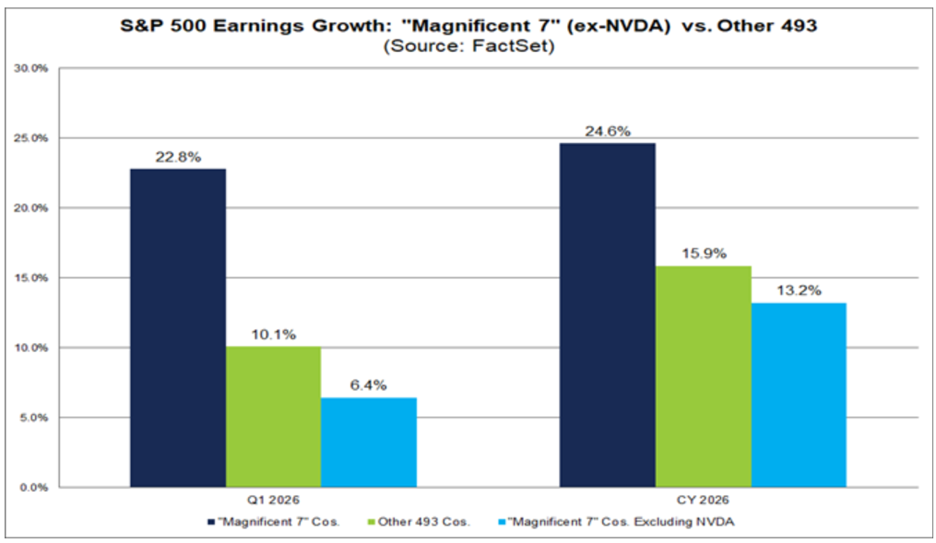

To help size the magnitude of this investment, consider that the US Economy grew 2% in the first quarter of 2026 and capital expenditures accounted for 70% of that growth rate. This rising tide lifts all boats seen in the earnings surge for non-tech companies that supply tech companies with copper, cables, concrete, etc. In fact, the highest sector level returns this year do not belong to technology (who will win?), but to energy, materials and industrials (everyone wins!). While Mag-7 earnings have fueled the market advance over the last couple of years, the Non-Mags have begun catching up. Stripping Nvidia from the calculation, Non-Mags earning growth will likely outpace the Mag-7 earnings growth rate for 2026:

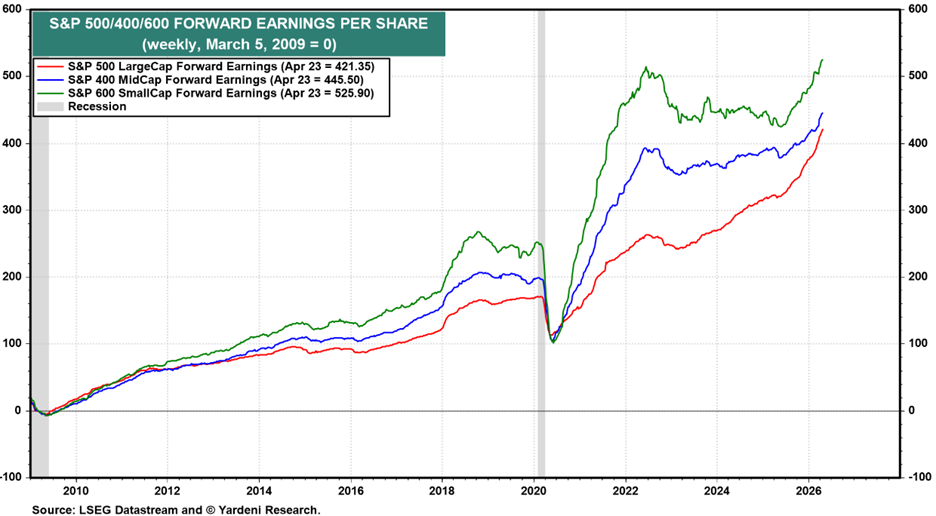

This AI Capex driven earnings cornucopia doesn’t only exist within the S&P 500 Large Cap universe, but also within the S&P 400 Mid Cap and S&P 600 Small Cap universes as well:

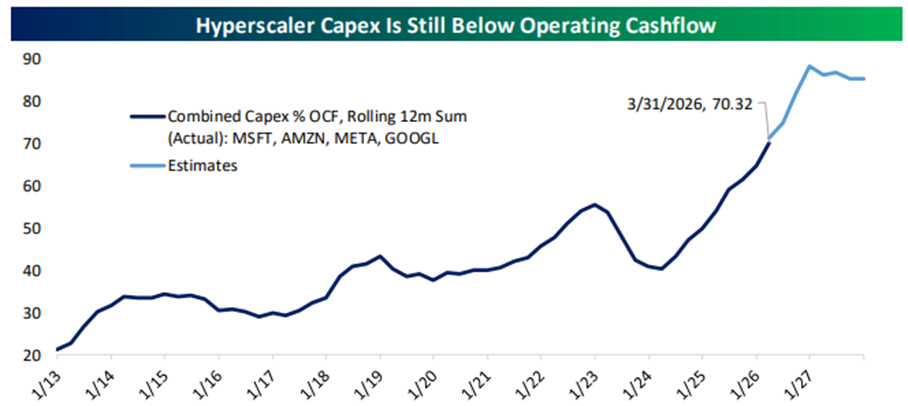

Frankly, I am not sure I recall a time with this much earnings power present so ubiquitously. The risk arises when considering how much financial capacity the Mag-7 have for spending at this level. Fortunately, they run very high profit margins and generate significant cash flow allowing them to largely self-finance (source: Bespoke):

Meaning, while Capex spending levels may seem atmospheric, they have yet to peak. In sum, probabilities have risen that AI capital expenditures will be higher for longer as the AI arms race persists, increasing economic, earnings and investor prospects.

So, which matters more to markets, oil prices or capex pace? With markets closing the month out at all-time highs, it seems resolved that the AI Capex cycle being higher for longer matters more than oil prices being higher for longer.

Bonus Data Point: US Households spend $650 billion directly and indirectly on oil annually; roughly $100 billion less than the Magnificent 7 will spend on AI capex in 2026.

Have a great weekend!

-David

Sources: JP Morgan, Emre Akcakmak (East Capital Group), Statista.com, Yardeni Research, Bespoke, FactSet Earnings Insight

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.