The world is in crisis. War rages. Tariffs disrupt. Allegiances fray. Protests seethe. Impeachment looms. Consumer confidence sits at record lows. US markets sit at record highs. How is this possible? Math. Forgive me for oversimplifying what should be more complicated, but the value of the market relies on only two variables: corporate earnings and how much investors are willing to pay for them.

Corporate Earnings

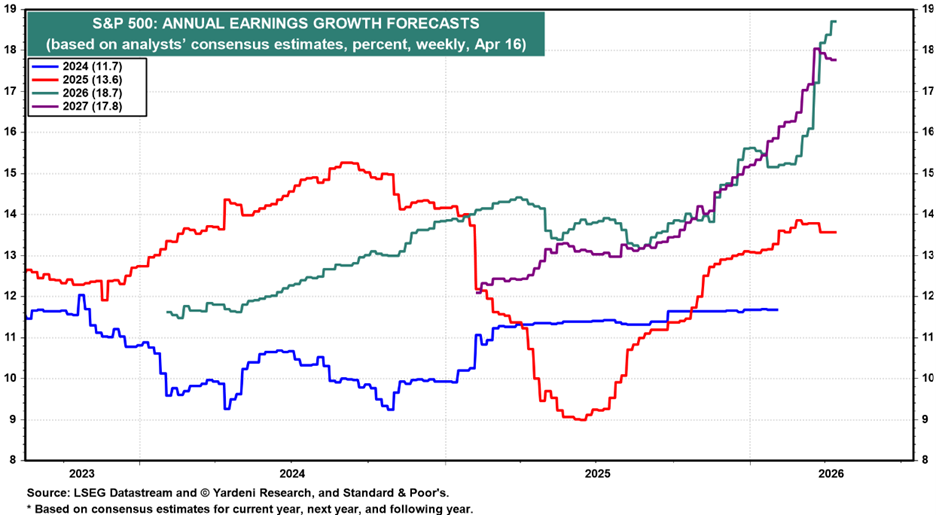

At the beginning of 2026, analysts expected around 15% annual earnings growth for the S&P 500 (the green line). Since then, analysts have marked up their earnings estimates to over 18%. Compare this with the 8.8% median growth rate over the last 20 years. Analysts also expect constituent revenues to increase nearly 10% this year while profit margins expand. Higher revenues, higher profit margins, higher earnings. Hat Trick! Seem unreasonable? So far, 9% of the S&P 500 companies have reported their first-quarter earnings. 90% have beaten expectations. Analysts have raised their revenue and earnings targets considerably since the war began. Should these assumptions prove correct, the S&P 500 will generate $323 in earnings this year. How much should investors pay for them?

Fair Value

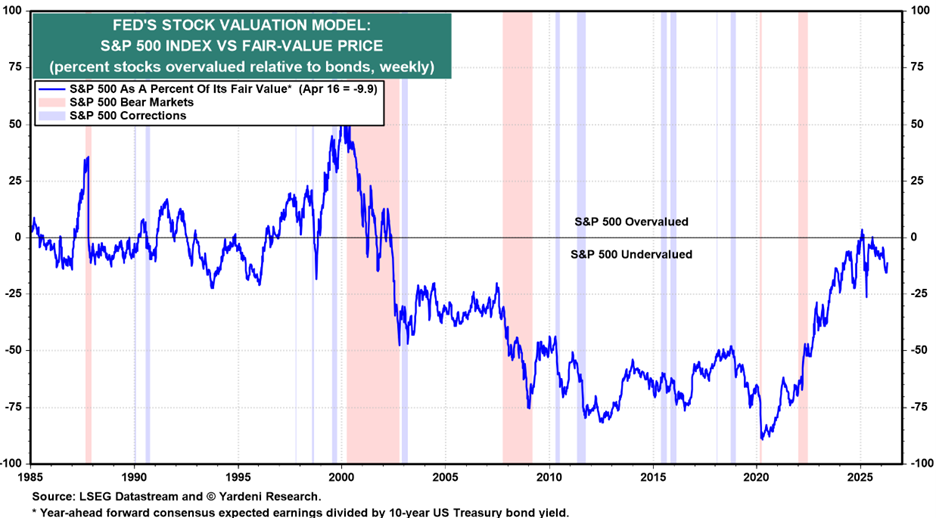

In finance, what investors willingly pay for earnings is known as “the multiple”. If a company earns $100 and you are willing to pay $1,000 for it, the company has a 10x multiple. If it’s a great company with higher-than-average prospects, perhaps you will pay 20x. As in real estate, all individual company valuation decisions are local. At the market level, prevailing interest rates largely determine multiples. To arrive at a fair-value multiple, simply invert them. For instance, a 10% interest rate environment supports a 10x multiple, while a 5% interest rate environment supports a 20x multiple. Today, the 10-year Treasury bond yields 4.25%, supporting a fair market multiple of 23.5x for the S&P 500. During the fog of war, the S&P 500 multiple fell to just over 19x, making the market meaningfully undervalued as seen above. Now, let’s do math! $323 in expected earnings multiplied by 23.5x produces a fair value estimate of 7,590. That’s 11% higher than last Friday’s close at 6,817, and that doesn’t even begin to consider 2027’s earnings estimate of $378.

Mathing Iran

Anytime the government increases spending without raising taxes, fiscal deficits increase. Economists call increased deficits economic “stimulus”. By many estimates the war in Iran increased deficit spending $1 billion a day. That’s stimulus. Conversely, higher oil prices tax the economy. Gasoline increased 35% per gallon due to production and transportation disruptions. On average, US households spend around $50 a week on gas. A 35% increase equates to an additional $15 a week. The war has lasted 6 weeks, costing the US consumer $90 extra dollars at the pump, so far. Fortunately, this tax season, IRS refunds increased 11%, generating an additional $350 for each filer, on average. This stimulus more than offsets the drag at the pump, making the consumer hit from $100 oil largely a non-event, leaving earnings expectations intact.

The Math

Concerns over wartime inflation drove interest rates up from 4% to 4.44% at their apex. This put mathematical downforce on fair value multiples from 25x to 22.5x, overshadowing the resilience of earnings. Certain stocks (tech stocks) with above-market multiples corrected most, while those more reasonably priced corrected least. However, overall valuations entered the period below fair value raising the risk of overshot and increasing the potential for rapid recovery. The multiple for the S&P 500 ended last year around 23x and bottomed recently at 19x. That’s a 17% discount!

With war waning, increased earnings expectations combined with decreased valuations enable a double positive. Higher earnings times higher multiples powered these higher highs. It’s just math!

Have a great Sunday!

-David

Sources: Yardeni Research

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.