We entered 2026 as we almost always do, bullish but fearful. Bullish because, on average, equity markets appreciate 75% of the time in any given year and appreciate 85% of the time without a recession. The combined fiscal, monetary, deregulatory and AI Capex stimulus should insure against recession and corporate profit margin expansion and earnings momentum should ensure continued gains for investors. Fearful, because supply shortages across the economy (labor and semiconductors) might overwhelm productivity benefits leading to stubborn, if not elevated, inflation levels. This could force Trump’s handpicked Fed to tighten policy, rather than loosen it, as ordered. Higher inflation doesn’t necessarily mean lower stock prices. In 2021, inflation rose from 1.3% to 7.1% while the S&P 500 rose 28%. However, it does increase performance disparity within the market, making selectivity more important. Higher rates increase the cost of debt and threaten higher valuations, leading us to favor companies with lower debt levels and lower P/E’s. In short, our strategy entering the year: expect continued gains, expect inflation risks, select accordingly.

The War Impact

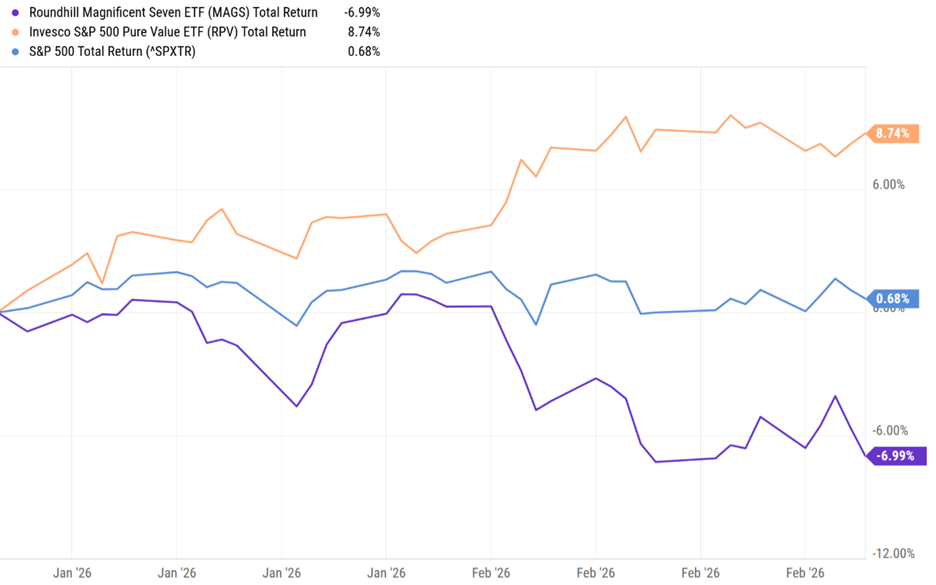

Prior to the first air raid in Iran, capital rotations within the market endorsed our view. Note the performance differential between the S&P Pure Value ETF sporting a 12x P/E vs. the MAG 7 with a 28x P/E, through February:

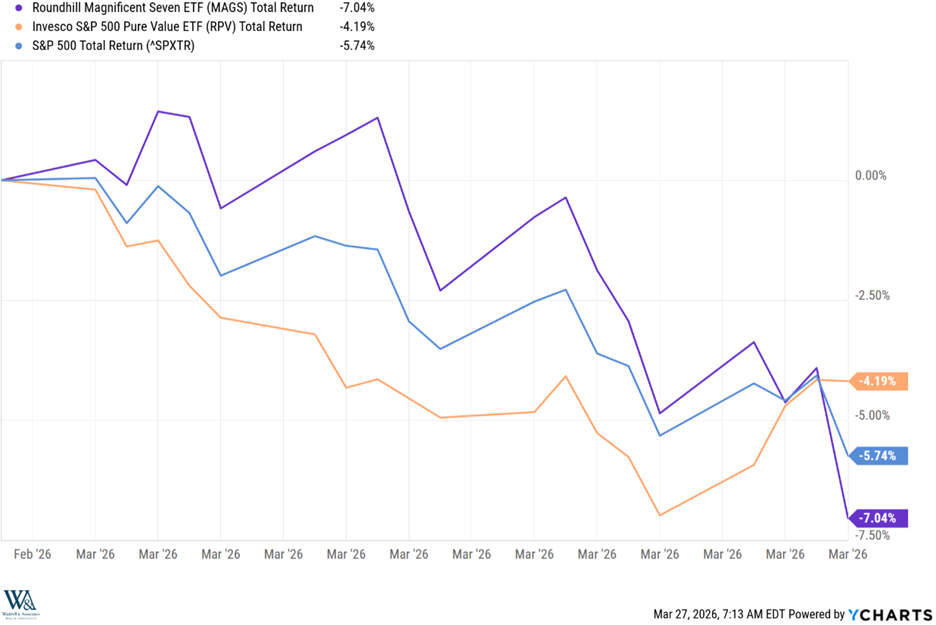

A 16% performance disparity between these high P/E and low P/E cohorts before the war, within an S&P up 1%, well articulates the point. How about since Epic Fury began:

Clearly, the war hasn’t helped investors. Initially, the higher P/E Mag 7 cohort made a relative comeback (purple line) as investors crowded into comfortable earnings growth bunkers, only to rethink valuations and rotate back to safety (orange line). For the trained eye, this chart conveys the uncertainty present in the marketplace. Will earnings growth persist? Will inflation levels rise? Will economic growth decay? Will the S&P 500 violate technical levels leading to an algorithmic washout? When and where will this market bottom? Where can I hide out until then?

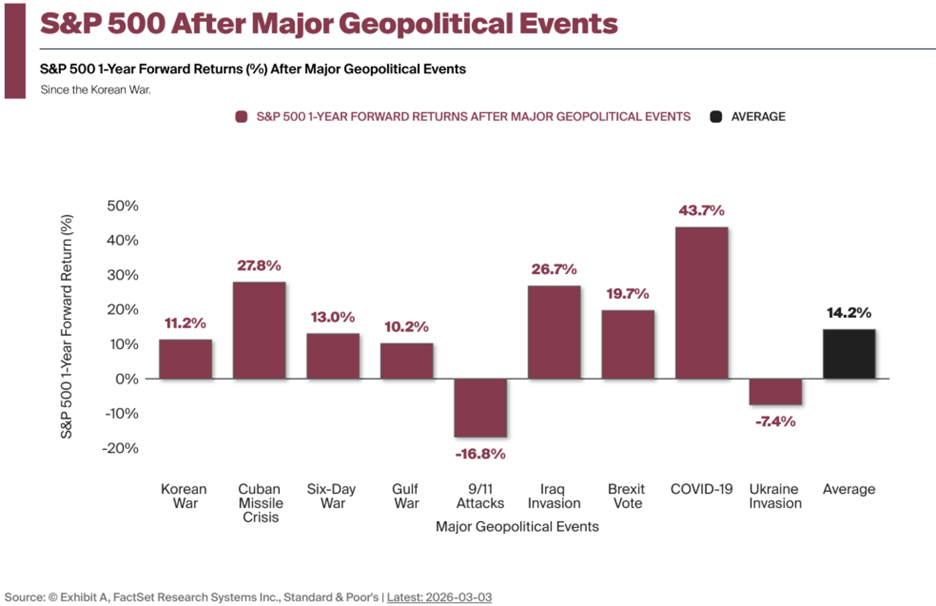

Seeking clarity, I posed these questions to Chat GPT. Chat doesn’t know. So goes the fog of war. Therefore, we can only draw on experience. First, our base case outlook gained validation prior to the conflict and therefore should sustain post. Rotating capital within or across asset classes amidst the fog of war makes little sense as demonstrated above. These are binary moments where investors either raise liquidity (sell everything) or deploy liquidity (buy everything). Trying to game a market being gamed by Truth Social isn’t strategic, its gambling. In unknowable moments, there is safety in stability. Second, because of the anxieties they create, investors often overestimate the economic implications of geopolitical events. Remember the European panic ignited by Russia’s invasion of Ukraine in 2022? European equities actually outperformed American equities that year. In fact, if you look at past geopolitical events, markets tend to absorb inital shocks and rebound smartly:

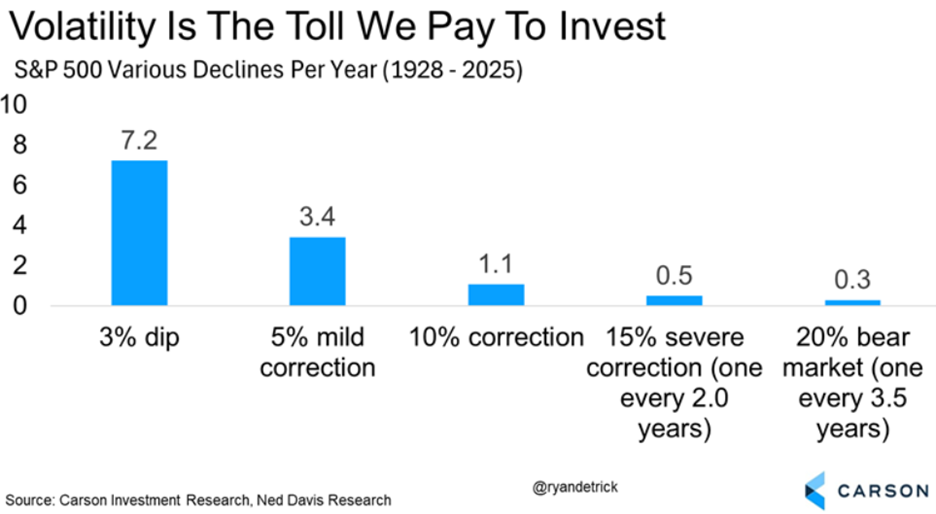

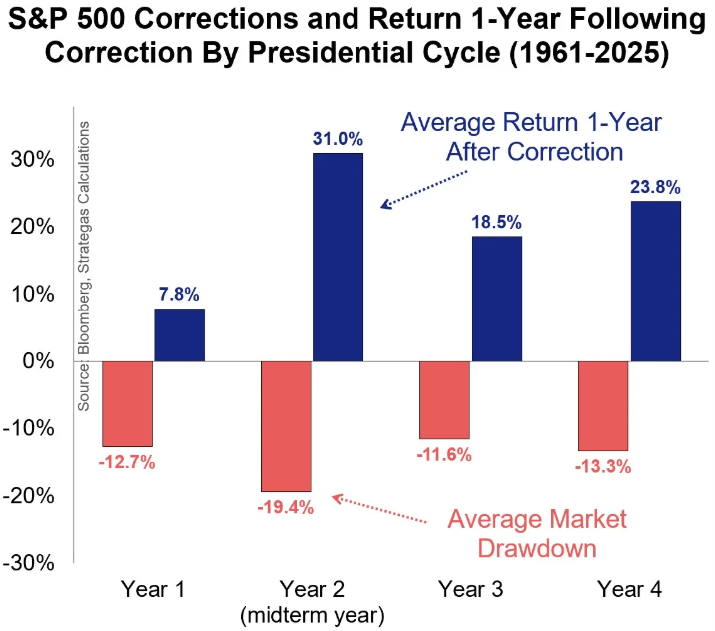

The two down years include 9/11, which occurred during the Dot-Com collapse, and the Ukraine invasion which occurred alongside 9% inflation. Those events may have agitated the markets decline, but they didn’t cause it. With our current backdrop of economic and earnings momentum we have a far sturdier foundation reflected in the markets limited drawdown to date. Consider the probabilities of drawdowns in any given year:

In any given year, on average, the market declines by 3% 7.2 times, 5% 3.4 times, and 10% at least 1 time while appreciating 75% of the time. Do I expect this market to pierce the 10% drawdown level, probably. Do I expect a 15% decline, maybe. Neither would be unusual or insurmountable, especially for a mid-term election year:

Should this market decline accelerate, we will refer to our down-market playbook and reprise our activity seen in April of 2025. We will sell positions to harvest tax losses, locking in future tax benefits, and we will redeploy capital opportunistically anticipating recovery. Remember, down markets have benefits. The valuations that so concerned investors entering 2026 have corrected, making the menu of buying opportunities longer:

In sum, it’s misguided to trade headlines within the fog of war. Should markets move to extremes, mispricing may create opportunities, but any transactions must comply with overall strategic outlooks. Under-trading geopolitical events has produced far higher investment returns for investors than overtrading. Be patient, be opportunistic, and stay the course.

Have a great week!

-David

Sources: YCharts, Factset, Carson Investment Research, Baird, Yardeni Research

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.