The conflict in the middle east has largely confused investors and commentators. We have been through many of these military market shocks before and gained well-earned perspective. To gauge investment impact and assess the case for reallocation, we focus less on battlefield maneuvers and more on key indicator maneuvers. This week, I will quickly share our war room dashboard and our investment battle plan.

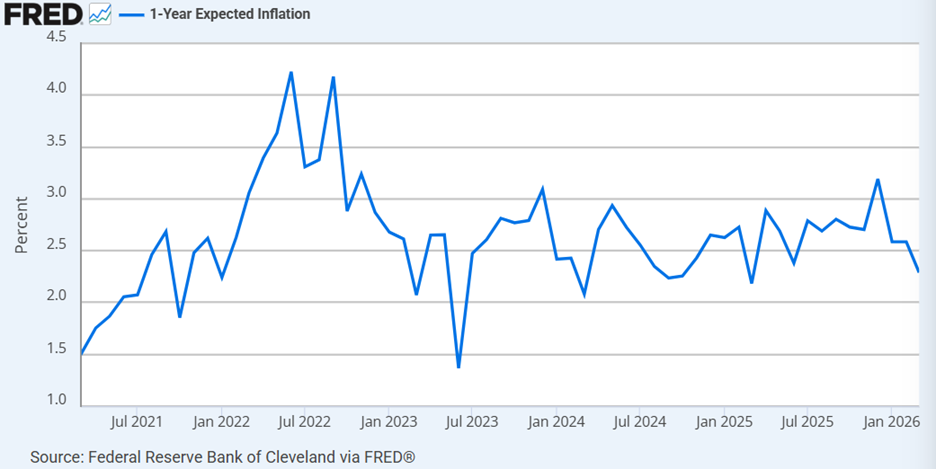

Inflation Expectations

The Fed’s 1-Year Expected Inflation measure reveals a market that perceives the conflict in Iran as temporary. We received several backward-looking inflation indicators this week that were also largely benign. Most notably, consumer price inflation (CPI) fell to 2.4% year-over-year, its lowest reading in 5 years. This number will surely rise in the next report reflecting higher gasoline prices, and the Fed will most certainly not cut rates next week, but for now inflation expectations sees war driven inflation as transitory.

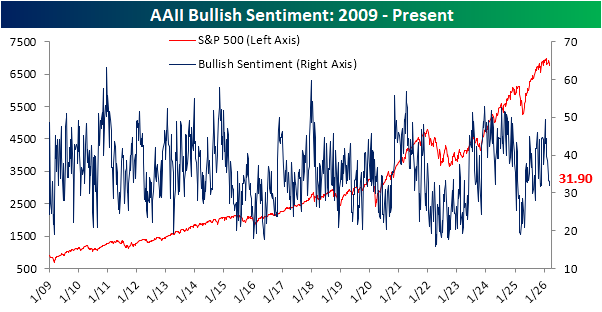

Investor Sentiment

Aggregate measures of investor sentiment have declined sharply since the war began, but they have not reached capitulation levels. I favor the AAII Bullish sentiment indicator most at times of stress. Whenever the number of retail bulls (the surveyed participants who believe the market will rise) falls anywhere near 20%, an upward market turn typically follows.

With 31.9% still bullish, while we have corrected the froth from 50% a month ago, we have not reached the moribund levels that signal panic, or an imminent advance.

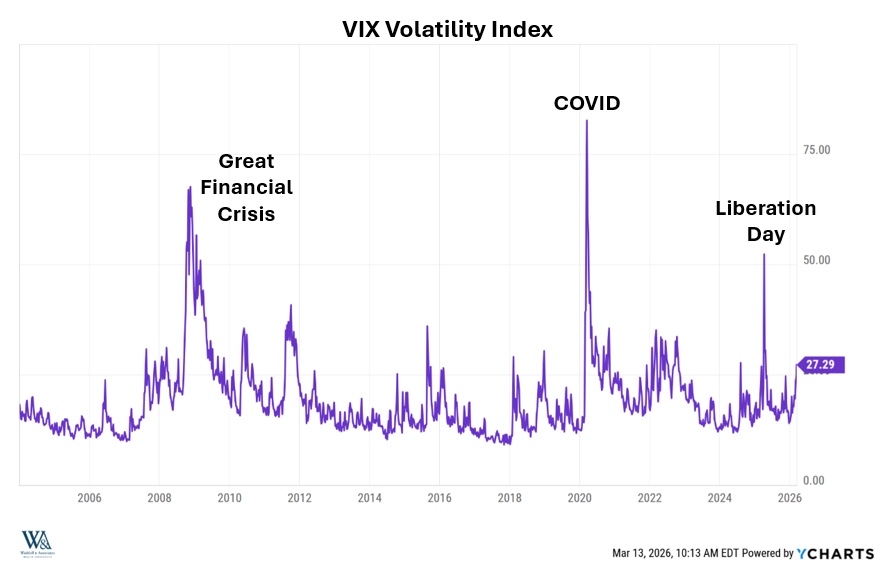

Volatility

The VIX volatility index provides another investable measure of sentiment. When panic hits, the VIX spikes, but panic typically overestimates negative possibilities presenting a great buying opportunity for investors. For instance, after Trump’s Liberation Day announcement, the VIX spiked above 50 and we became enthusiastic buyers. Trump scaled down tariff rates through negotiations, and the S&P 500 went on to hit new highs. Currently, the VIX sits at 27—elevated, but not panicky:

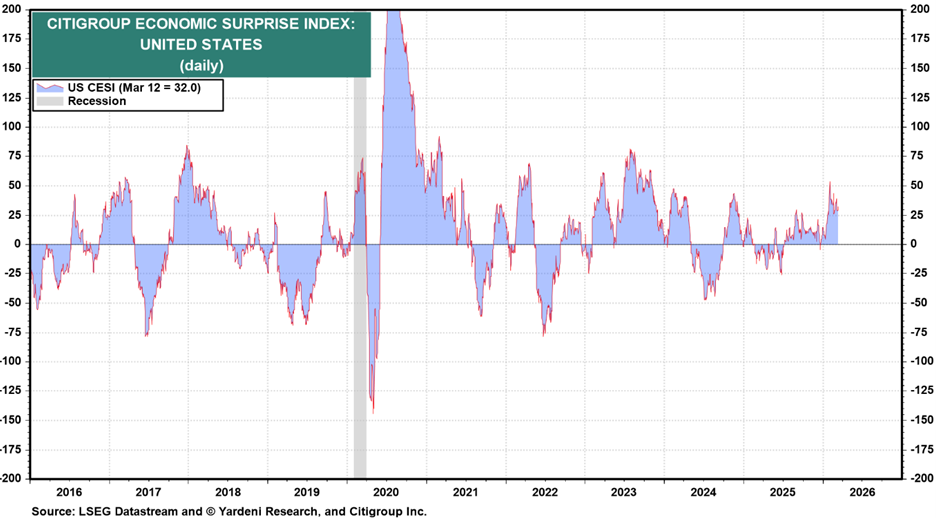

The Favorable Fundamentals

When military conflicts and geopolitics command attention, investors tend to lose track of the fundamentals. One can claim that this conflict negates the usefulness of using recent trends to predict future trends, but economic movements contain deep inertia. Prior to the bombing campaign, US economic releases had been steadily surprising economists to the upside:

Simultaneously, Wall Street analysts have been consistently raising forward earnings expectations:

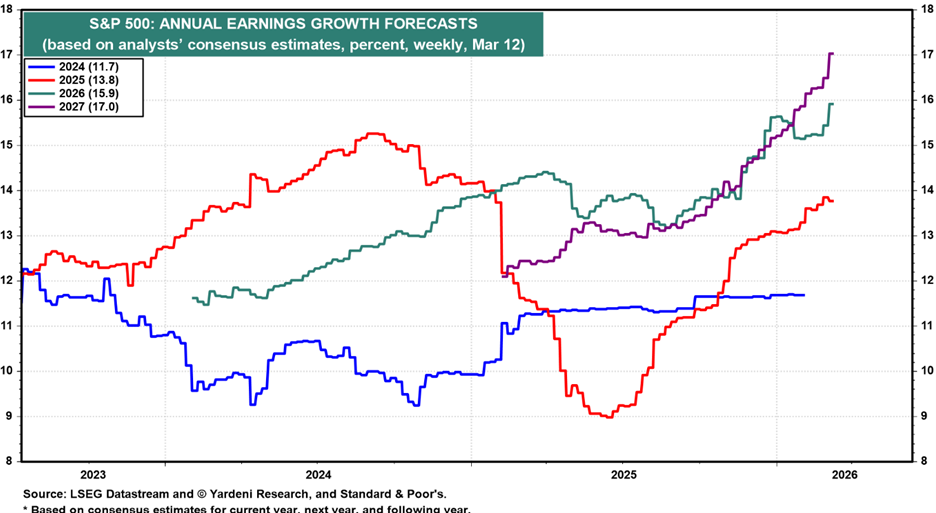

Let’s take a moment here. The chart above chronicles S&P 500 earnings estimate changes over time for the years 2024, 2025, 2026, and 2027. Earnings grew 11.7% in 2024, ending near the high end of the expected range. Earnings grew 13.8% in 2025, also ending near the high end of the expected range. Earnings estimates for 2026 and 2027 have been climbing and now sit at the highest levels of their expected ranges at 15.9% and 17% growth, respectively. This powerful earnings expectations up-force has undoubtedly muted the Iran conflicts downforce. This earnings inertia explains the measured sentiment response and the less than 5% drawdown in the S&P 500 from recent highs.

Have a great week!

-David

Sources: Federal Reserve, YCharts, Yardeni Research, Bespoke Investment Group

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. References to political figures or policies are for informational purposes only and do not represent an endorsement by Waddell & Associates. Any forward-looking statements reflect current opinions and assumptions and are subject to change without notice; actual results may differ materially. Past performance does not guarantee future results. Waddell & Associates may use artificial intelligence tools to help generate or summarize content; all outputs are reviewed by our team for accuracy and relevance.