While attention fixates on the difference-maker in a hotly contested election, investors shouldn’t overlook the true October surprise this year. For the month of October, the S&P 500 traded within a 2.5% range and ended the month down less than 1%.

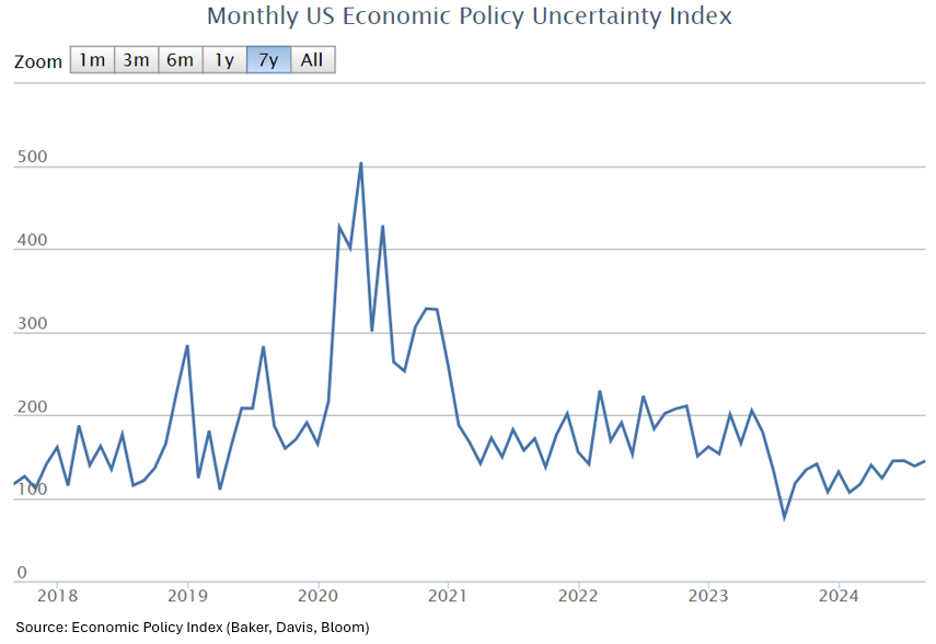

A Spooky History

October has a history of spooky market behavior. General volatility levels rank 34% higher in October compared to the other months and three of the last four trading days with losses of more than 10% occurred in the month of October. With Trump vs. Harris worldviews overheating social media feeds, conflicts raging worldwide, and a mixed bag of economic data, conditions were set for a potentially red October. So why the lullaby? First, while Trump and Harris seem far apart, neither of their economic policies seem to be causing much concern:

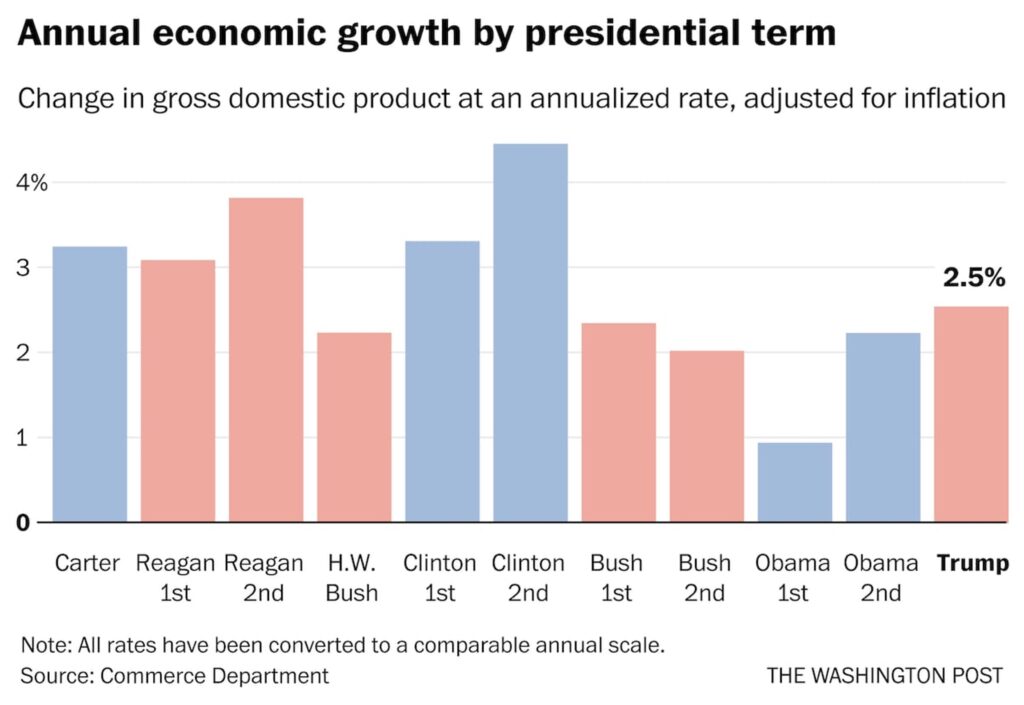

Perhaps that’s due to expectations of a divided Congress, or recognition that Presidents themselves have much less influence over economic growth than widely assumed. Consider the GDP growth rates listed below (Trump rates are pre-COVID):

The Truth About the Market and Elections

Outside of Obama’s first-term clunker, the US economy has grown 2%+ under every president dating back to Herbert Hoover. Turning to the stock market, the performance differentials between presidential administrations are just as inconclusive:

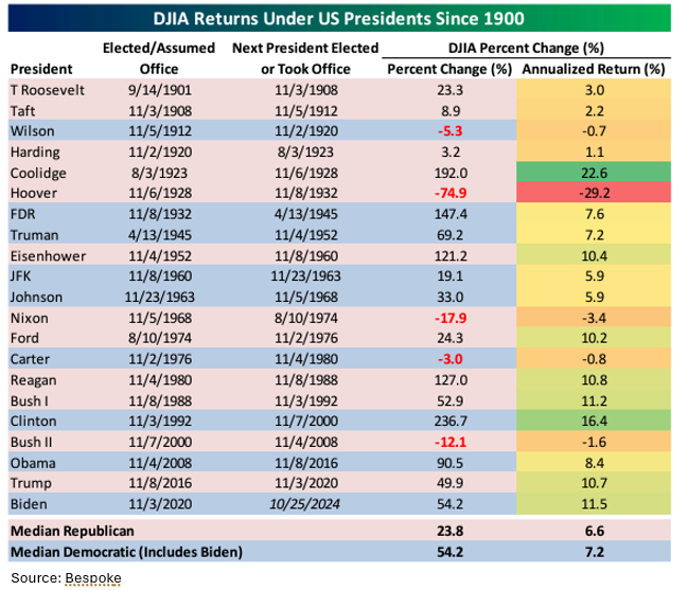

Looking at the price returns for the Dow Jones Industrial Average going back to 1900, Republican Presidents have rewarded investors with 6.6% annualized gains while Democrat Presidents have rewarded investors with 7.2% annualized gains. I haven’t done the statistical work, but I suspect that the -30% return under Hoover accounts for the differential. How did the Dow perform under President Trump? It rose 50%. How did the Dow perform under President Biden? It rose 50%.

We Invest in Companies, not Governments

I do not know who will win the Oval Office on Tuesday. I do know that I have received a flood of queries surrounding the implications for investors. Based on the history presented above, the implications are immaterial. What powers the US economy and investor returns is not presidential policies, but trillions of micro decisions made by an industrious, ingenious, and innovative population. Our hard-coded system of laws, property rights, and protections provides 338 million Americans with the incentives to pursue prosperity and retain the rewards. So, stress less about Tuesday. We invest our client assets in companies, not governments, and with our dynamic, ever-growing economy, earnings continually rising, and AI contributions just beginning, the future is bright no matter who takes Tuesday.

Happy November!

-David

Sources: Economic Policy Index, Department of Commerce, Bespoke

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. Past performance does not guarantee future results.