For those who watched our 2024 halftime report, you will recall our concern that the greatest risk for investors resided within the tension between the backward-looking Federal Open Market Committee and its forward-looking Chairman, Jerome Powell. While Powell seemed to defer to the committee and its inertia over the past few months, he broke away on Friday with conviction. Here are some of his comments made at Jackson Hole that had me dancing at my desk:

“Our restrictive monetary policy helped restore balance between aggregate supply and demand…”

Translation: The economy has normalized. Monetary policy should normalize.

“My confidence has grown that inflation is on a sustainable path back to 2 percent.”

Translation: I’m in charge now. I will cut rates.

“All told, labor market conditions are now less tight than just before the pandemic in 2019—a year when inflation ran below 2 percent…”

Translation: In 2019, the Fed Funds rate averaged 2.16% in a tighter labor market with no inflation. I have substantial room to cut rates.

Markets responded quickly to Powell’s remarks as the probability of a .50% rate cut in September rose, indicating a more dovish statement than anticipated. The U.S. Dollar weakened, longer term interest rates dropped, and small cap stocks surged. Powell has formally pivoted. Investors must now formally pivot as well.

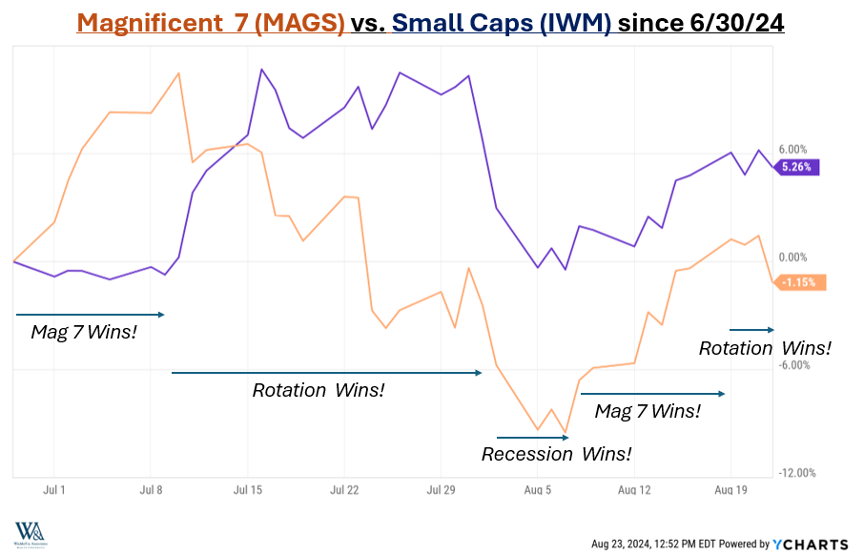

I recently discussed with Frank Holland at CNBC that the market has been vacillating between three primary trading strategies recently. The first strategy is the “Magnificent 7 trade” supported by status quo conditions of stable economic growth and limited earnings breadth (Mag 7s win). The second strategy is the “rotation trade” supported by disinflation, rate cuts, and earnings dispersion beyond the Magnificent 7 (small caps win). The third is the “recession trade” supported by restrictive monetary policy inertia and employment report undershoots (everything loses). To determine which trade holds advantage, let’s review the contest between small caps and the Magnificent 7 since 6/30:

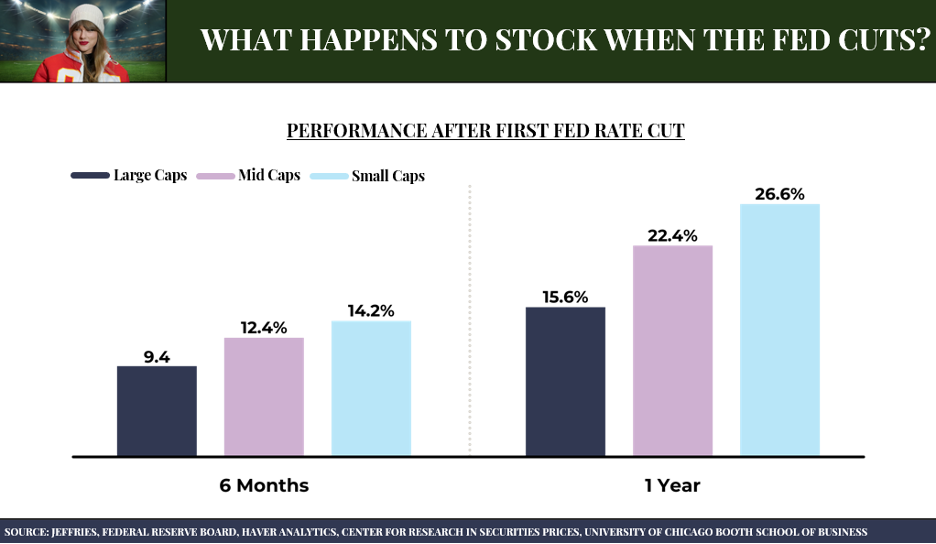

Over the last two months, markets have appeared indecisive as all three strategies have held leadership positions. First, the Magnificent 7 trade continued its first-half leadership into the early second half. Next, the rotation trade surged dramatically on a weak inflation report. Then, confusion over a weak employment report and the busted Yen carry trade led to a temporary ascension for the recession trade. Next, a return of economic confidence revived the Magnificent 7 trade. Finally, the Powell pivot reignited the rotation trade. For the entire period, the “rotation trade” has the lead as Small Caps outperformed the Magnificent 7 group by 6%. We expect this will continue since history favors small cap stocks during Fed rate cut cycles:

Clearly, rate cuts power small cap outperformance, but small cap rallies haven’t been trustworthy in years. This has left them unloved and under-owned, only adding even more rally capacity to them. Much of this neglect has been a function of the “potential” for rate cuts, rather than the promise of rate cuts, or rate cuts themselves. But with Powell’s newfound rate cut conviction, investors must gain conviction in the “Rotation Trade” to best play… the Powell payday!

Have a great week!

-David

Sources: YCharts, Jeffries, Federal reserve Board. Haver Analytics Center for Research in Securities Prices, University of Chicago Booth School of Business

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. Past performance does not guarantee future results.