While we spend much of our energy looking forward, and we will devote many watts to our upcoming Halftime Outlook, it seems appropriate, and it is indeed satisfying, to look back at a very profitable 2024 first half.

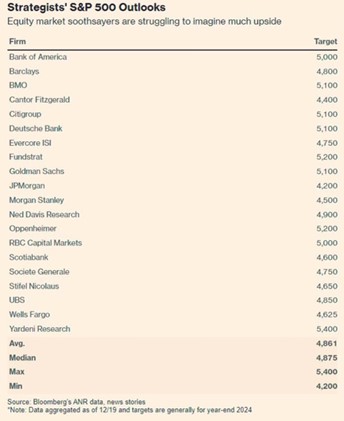

Recall that as strategists, we entered the year taking the “over” on performance. We anticipated that Wall Street’s lukewarm optimism and the market’s tendency to rise more rather than less would pleasantly surprise investors. At the start of the year, Wall Street expected a measly gain for the S&P 500 of 4% for 2024. Fearing that consumer exhaustion, sticky inflation, lofty valuations, and punitive interest rates would limit economic momentum and cap market appreciation, here were the tepid targets:

America’s biggest bank, JP Morgan, had the lowest target, expecting the S&P 500 to close 2024 at 4200 after finishing 2023 at 4770, for a loss of 12%. Ed Yardeni, one of Wall Street’s finest sages, foresaw a more uplifting gain of 13% to 5400. The consensus averaged a forecasted gain of less than 2%. We did not put forth a number other than to observe that without a recession, and with the earnings recession ending, the market had a higher probability of upside surprise than downside surprise and that prevailing pessimism only increased favorable odds. As of 2024’s halfway point, the S&P 500 stands at 5,460, 15% higher than the start of the year and 2% higher than Wall Street’s most optimistic forecaster… proving once again that in this business, when pessimism prevails, optimism pays!

Where the Gains Are

A substantial amount of this year’s gain for the S&P 500 can be attributed to the performance of the AI superstar, Nvidia. Nvidia appreciated 150% in the first half, reaching a market cap peak of $3.3 trillion, briefly making it the most valuable company in the world. Removing Nvidia’s gain from the S&P 500 removes about a third of the overall advance. Even still, a 10% first half advance ex-Nvidia still annualizes out to a 20% full year advance – a highly hearty pace. But the gains were not restricted to Nvidia and big cap tech. Beneath the large caps, the mid-caps (ETF: MDY) advanced 6% while the small caps (ETF: IWM) inched up 1%. Offshore, the All-Cap World Index ex-USA (ETF: ACWX) levitated nearly 6%, while the currency hedged version (ETF: HAWX) gained more than 11%. Emerging market indices (ETF: EEM) rose over 6% and more than 10% with the currencies hedged (ETF: HEEM).

Overall, it’s been difficult for stock investors to NOT make money in 2024. For bond investors, it’s been a little trickier with bond indices (ETF: AGG, LQD, HYG) mostly breakeven year-to-date. Commodity investors have enjoyed sizable gains in oil and precious metals, more than offsetting losses in natural gas and grains, delivering 6% gains overall (ETF: DBC). Any way you slice it, concentrated and balanced investors alike have more in 2024.

Have a great weekend!

-David

Sources: Bloomberg’s ANR Data

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. Past performance does not guarantee future results.