Will the US and Iran enter the middle east conflagration and ignite WWIII? Will our distraction and disfunction compel China to invade Taiwan? Will a November government shutdown lead to Treasury downgrades and defaults? Will higher rates lead to an economic hard landing? Will the winter chill in Europe drive up energy costs? Will Joe Biden and Donald Trump be the nominees for President in 2024? Will a disruption in the oil market drive inflation even higher? Will the Fed raise rates despite rising economic threats? Can the Miami Dolphins really win the AFC?

While bull markets always climb a wall of worry, this current wall has risen far faster than the climbers, leading to higher uncertainty and lower price levels. Since the end of July, the 10-year Treasury yield has risen by 25%, the U.S. dollar by 7%, and Oil by 5%. Concurrently, the large cap S&P 500 fell 10% and the small cap Russell 2000 fell by 20%.

These extreme moves across asset classes are in line with the extreme moves in headlines. However, for the purposes of this week’s blog, let’s resist the qualitative debates bridling the market and survey the quantitative data to get a more grounded sense of conditions.

The Economy Math

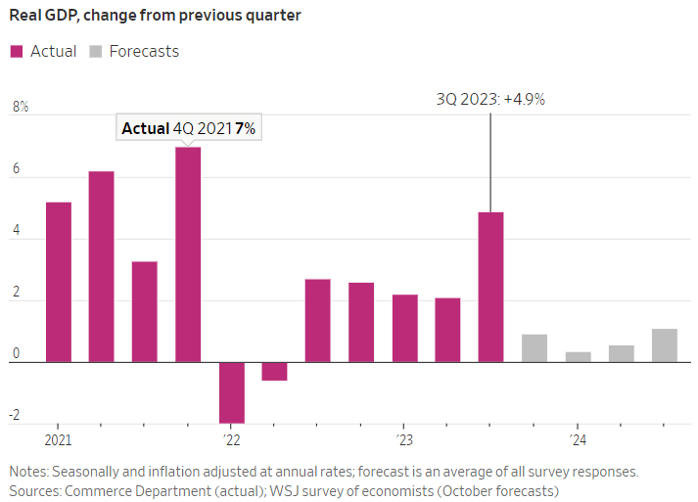

The US economy grew 4.9% in the 3rd quarter after growing 2.1% in the 2nd. Robust consumer spending levels powered the advance. Thank the Swifty Stimulus. (For those not on social media, that’s a reference to Taylor Swift’s concert tour, which generated $5 billion+ in economic activity). Few economists expect this pace to continue, and Taylor’s tour will end, but for now, the US economy is growing… Swift-ly:

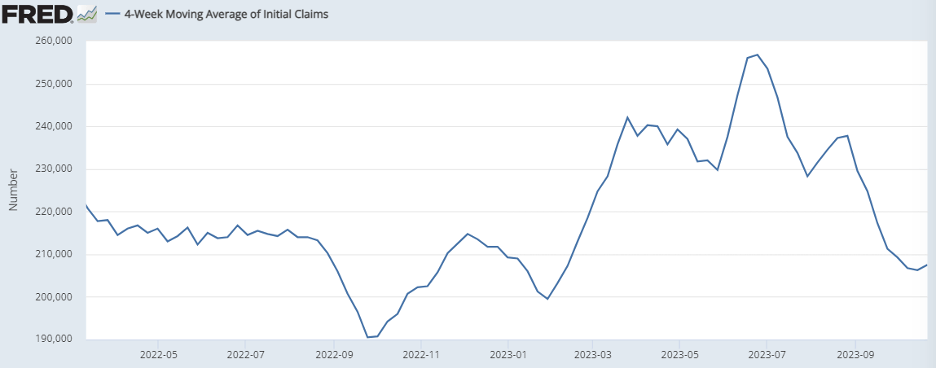

As we discussed last week, this more-than-doubling of GDP growth over the last quarter explains the sudden 25% rise in Treasury yields, but for the economy to continue expansion as the Treasury yields suggest, consumers need to continue their spendthrift ways through the holiday season. This requires income. As of the end of September, the U.S. unemployment rate of 3.8% remained at historical lows. Since then, we have not seen any material change. In fact, unemployment claims, as highlighted below, have fallen over the past month:

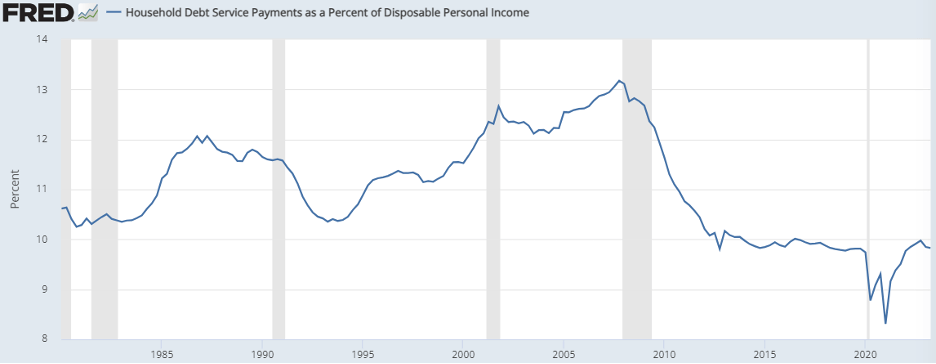

While wage inflation rates have slowed, the most recent readings remain at rates twice as high as pre-pandemic levels. Additionally, although markets have contracted, household net worth remains near record levels. Lastly, while higher rates increase debt-carrying costs, current household debt service levels remain near historic lows:

Consumer distress tends to follow corporate distress, and a quick check of high yield credit spreads reading 4.3% also remains in line with pre-pandemic levels. While layoffs may indeed be forthcoming, the U.S. economy continues to post 1.5 job openings for each unemployed worker. Based upon this analysis, consumer spending capabilities remain intact, which will continue to support GDP Growth.

Thursday’s GDP release also contained an encouraging read on inflation. While the headline Personal Consumption Expenditures (PCE) inflation rate jumped 3%, the Fed’s preferred measure of core inflation only rose 2.4%, well within striking distance of the Fed’s 2% target.

Overall, the economy grew robustly in the third quarter while inflation continued its glidepath lower. In response, the futures market currently prices in an 80% probability that the Fed will not raise rates any further this year.

Corporate Earnings

Thirty percent of S&P 500 companies have now released their third quarter earnings results. Roughly 80% of these companies have beaten expectations. Blending actual results and expected results, analysts now expect S&P 500 earnings will grow by more than 1% for the quarter versus expectations of a 1% loss as the reporting season began.

While that’s good news, the market hasn’t rewarded companies for their successes. Historically, when companies exceed both revenue and earnings expectations, their stocks rallied 1.1% on the day of the release, on average. So far this quarter, companies that have exceeded revenue and earnings expectations haven’t seen any lift in share prices. Revealing that in the current environment, more than math is at stake.

TIA – There Is an Alternative

During the long period of time when the Fed used zero interest rate policy and quantitative easing to suppress interest rates, Wall Street created the TINA acronym to explain the stock market’s resilience.TINA stood for “There Is No Alternative” because with bonds yielded nothing, investors had to own stocks to generate returns.

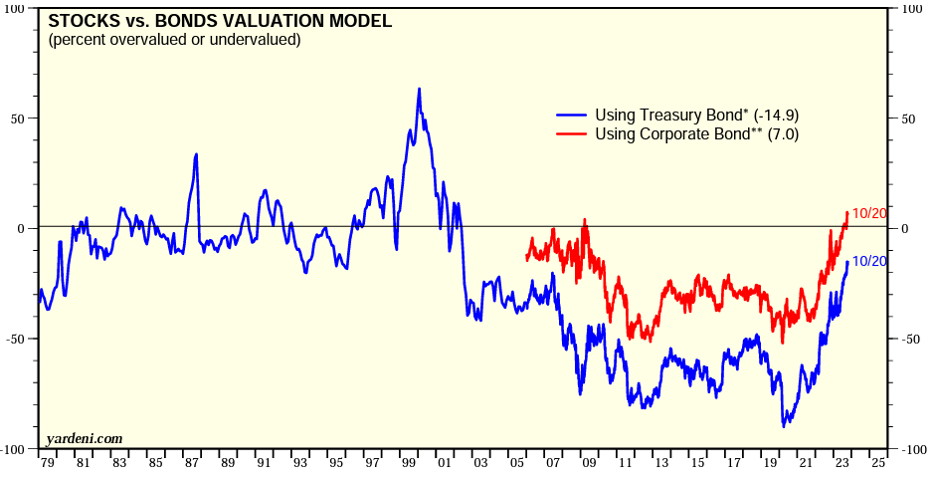

To quantify this argument, we can compare bond yields in the bond market with earnings yields in the stock market to reveal relative value. Consider the following chart:

The S&P 500 currently trades at 17.5 times earnings. Inverting this multiple derives an earnings yield of 5.7%. When bond yields sat in the low single digits, stocks had no competition. However, today, with Treasury bonds yielding 5% and corporate bonds yielding 6%, TIA – There Is an Alternative! Investors struggling with harrowing headlines are no longer forced into stocks to seek returns given their valuation parity levels with bonds.

This significant change certainly benefits investors, but it also removes marginal demand for stocks. A year ago, with bonds yielding less than 4%, a 6% earnings yield for stocks warranted thicker skin,but with yields equivalent today, skittish investors can simply defer equity purchase decisions until conditions clear.

However, mathematically, if earnings rise without rising share prices, the earnings yield advantage for stocks will grow. While analysts only see 1% growth in Q3, they see 11% growth in Q4, and 12% in 2024, making this moment mathematically attractive for more fearless allocators.

When Then?

Unfortunately, geopolitics has incarcerated our year-end rally. To liberate, we either need better headlines or much lower bullish sentiment levels. Last week’s AAII bullish survey rate stood at 29.3%, higher than levels hit in late September when our latest rally attempt began.

To provide further confirmation that fear has reached surmountable levels, we may also need the VIX volatility index to climb back towards its Silicon Valley Bank failure highs. The VIX topped closer to 30 then and sits around 20 now.

In sum, while the math reads favorable for stock market investors, the headlines do not. Combining headline anxiety with the 5-6% yields offered in bonds creates a formidable competitor for stocks. Until headlines improve, or sentiment drops to contrarian extremes… Santa remains sequestered.

Have a great weekend & Happy Halloween!

David S. Waddell

CEO, Chief Investment Strategist

Source: Wall Street Journal Survey of Economists, Fred Database, Yardeni

This communication and its contents are for informational and educational purposes only and should not be used as the sole basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to the accuracy, completeness, or correctness of said information. Past performance does not guarantee future results.