The Full Story:

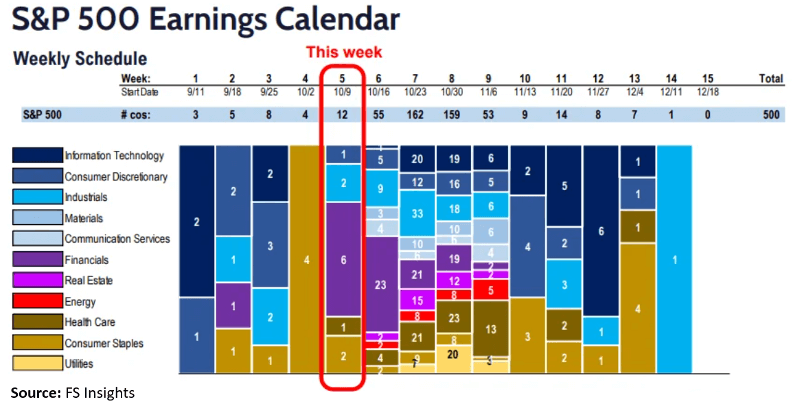

The negative-sentiment-to-positive-fundamentals Santa Claus rally we called for last week began with a bang as the Dow rallied nearly 500 points through Wednesday. Unfortunately, the weight of war, a stubborn inflation print, and a lukewarm Treasury auction tripped up the sprinting Dow, reclaiming 200 of those points by the week’s end. Nonetheless, the rally has started and will now rely on earnings results for continuance. Earnings began to trickle in this week, but the bulk of the earnings results arrive over the next three weeks, as seen below.

So far, so good. On Friday, JP Morgan, Wells Fargo, and Citigroup kicked off the season with upside surprises. Despite the apparent headwinds, combined, revenue for the three banks rose 14% over the past year. Funding costs have risen, the trio paying depositors 2.6% on average, but this remains well below prevailing lending rates.

Charge offs have also risen and credit card balances are rising, but management commentary conveyed consumer confidence and reduced “hard landing” expectations. Non-banks will dominate next week’s releases along with industrials which should lend further support. At the moment, analysts still suspect earnings will contract for the quarter, but with continued upside surprises, it will take very little to flip positive after three consecutive negative quarters. Note the pattern below of recent pleasant quarterly surprises:

What’s up with Inflation?

The September Consumer Price Inflation report released Wednesday received the brunt of the drawdown blame. We disagree. While headline and core inflation remain well above the Fed’s 2% target at 3.7% and 4.1% year over year, by removing lagging shelter inflation, both measures collapse to 2.0% on the nose. Shelter inflation rose 7.1% in September, but every other, more immediate measure shows rapid disinflation, if not deflation, in shelter expenses.

For anecdotal evidence, look up homes for sale in your neighborhood on Zillow and count up the price reductions. I am typing this week in Nashville where the Zillow Values Index reports Nashville values have fallen 2.6% over the past year. That’s a far cry from the 7% inflation tabulated by the Fed. This timing reality mismatch has not been lost on Fed officials. Numerous voting members have cited the current Fed Funds rate as sufficient. Accordingly, the Fed Funds futures market prices in a less than a 30% chance of another rate hike by year end. So, with inflation continuing its decent and Fed officials signaling peak Fed Funds, what does deserve this week’s drawdown blame?

Auction Malfunction

On Thursday, the US Treasury auction of $20 billion in 30-year bonds failed to generate enough investor demand. This led to a 0.12% surge higher in yields for the 30-year and a sympathetic surge 0.10% higher for the 10-year. Treasury demand shortfalls continue to be the markets’, and our own, primary concern moving forward. With inflation falling, longer-term rates should drift lower, but meager tax receipts and higher government spending continue to force rates higher as demand wanes. Note that the amount of Treasury issuance chronicled below through September already exceeds full year totals, outside of the 2020 stimulus surge:

Going forward, government deficit projections offer little comfort, and rising yields drive rising interest expenses in a compounding vicious cycle. Washington political histrionics also deter bidders, as Speaker shuffles and shutdown brinkmanship tempts ratings agencies to further cut our grade. Unfortunately, forecasting Government fiscal behavior, debt market absorption rates, and global central bank policy shifts simultaneously is nearly impossible, and particularly frustrating for this market strategist.

Fortunately, markets discount the future and the current levels in long term yields contain the knowledge of deficit ramps, interest rate burdens and policy frameworks. The 10-year yield did close the week at 4.63%, below its October 6th high of 4.89%, no doubt a contributor to this week’s rally for equities. As long as yields behave reasonably, earnings upside should drive equity market upside. I just wish public sector behavior was as readily forecastable as private sector behavior. Anyone with that crystal ball please contact me, immediately.

As we collectively process the horrific and heartbreaking events dominating the news cycle this past week, it is impossible to ignore the fear and anxiety that many in our communities are facing. The loss, grief, and apprehension for loved ones’ safety are profound. Our heartfelt sympathies and support are with our clients, team members, and friends, who may be experiencing the impacts of this deeply disturbing and tragic violence. We share in your grief and pray for the safe return of those who are missing.

David S. Waddell

CEO, Chief Investment Strategist