The Full Story:

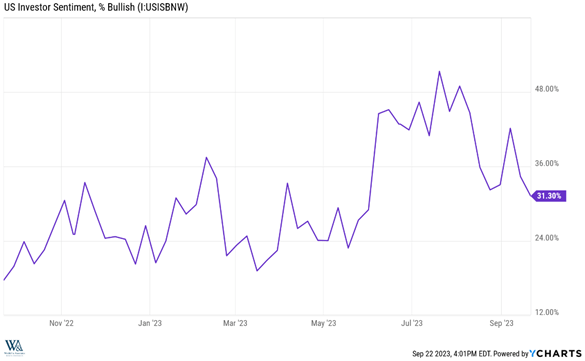

Markets continued their downward trend this week as the Fed released its economic forecast, and Chairman Powell defended his position of not raising rates while also not cutting them. Many interpreted the Fed’s optimistic economic outlook as a tone-deaf policy mistake more likely to increase recession odds. This interpretation pleases us. Investor sentiment levels have fallen meaningfully since their frothy July peaks from 51% bullish to 31% bullish but still haven’t quite reached levels needed (20-25%) to cue a robust Santa Claus rally:

We remain in a sentiment and seasonally driven drawdown period until further notice. Given the importance retail investors place on Government histrionics, the upcoming shutdown shenanigans might just punctuate this sentiment correction. Offering support for our viewpoint, interest rates, oil, and the US dollar have shot sharply higher in September while the S&P has shed less than 4%, and we remain only 6% beneath the July highs. If the worry beads of an oil shock, rate shock, currency shock, government shutdown, and the UAW strike have only managed to knock this market down 6%, there must be more momentum and resiliency in this economy than suspected. We agree. And that’s what the Fed said.

Summarizing the Fed’s Summary

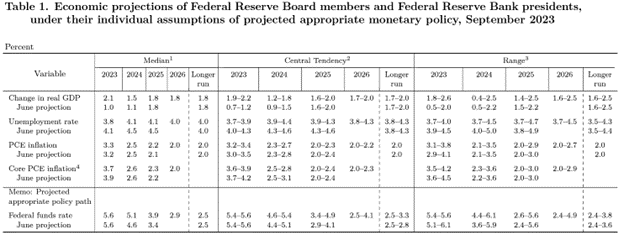

Each quarter, the Fed releases a summary of economic projections. This report anonymously details each of the 17 FOMC members’ outlooks on GDP, unemployment, inflation, and interest rates. The table below contains the details for the meticulous. For the rest of you, don’t grab your readers; I will highlight what’s important underneath:

Let’s start with GDP. In June, the Fed expected full-year economic growth of 1% for 2023 and 1.1% for 2024. Now they expect 2.1% for 2023 and 1.5% for 2024. That’s a 100% upgrade in their view for this year and a 50% upgrade for next year. Wow!

For unemployment, the Fed projected a 4.1% rate at year-end and a 4.5% rate at year-end 2024, down from 4.1% and 4.5%, respectively. Great!

On inflation, the Fed projected a reduction in core PCE inflation from 3.9% to 3.7% for 2023, and 2.6% to 2.6% for 2024. Outstanding!

So, according to the Fed, the economy will be stronger than expected, unemployment less than expected, and inflation marginally less. Yahtzee! A more resilient and robust economy should carry a higher interest rate regime.

The Fed’s projection for their own policy rate remained 5.6% for this year but rose from 4.6% to 5.1% next year and from 3.4% to 3.9% in 2025. On this point, the market panicked, focusing on the higher rate regime rather than the robust economics. This “Ready, Fire, Aim” reaction was fine by us as the misread suppresses sentiment further despite the Fed’s confirmation of strengthening fundamentals. In his comments, Powell cautioned Fed watchers to treat these quarterly future casts as guesses, not plans. He reiterated his focus on the monthly CPI inflation and unemployment reports to direct policy, and paid no attention to the SEP as a policy tool. The September Employment Report arrives October 6th, and the September CPI report arrives October 12th–right about the time we expect sentiment to bottom.

Have a great weekend!

David S. Waddell

CEO, Chief Investment Strategist