The Full Story:

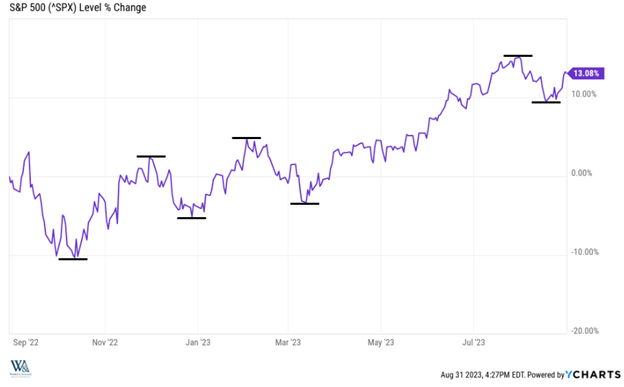

The books closed on Thursday with the S&P 500 1.7% lower for the month of August. This may not feel like a victory for investors, but the S&P stood 5.5% lower mid-month and rallied 4% into month’s end. The combination of weak seasonal trends, inflated investor sentiment, and surprisingly higher longer-term interest rates drew the drawdown.

We view the decline as constructive. We also viewed the spike in yields as temporary, given historic Treasury issuance that overwhelmed Treasury demand following the debt ceiling freeze, low tax receipts, and various demand depressants.

However, many saw the run-up in yields as structural rather than technical, which drove retail investor bullishness down from 50% at the start of the month to 33% by month’s end. While bullishness remains slightly higher than we would like at this point, it does read below its long-term average of 37.5%, making market sentiment neutral now rather than hostile as it was at the start of the month (remember sentiment is a contrarian indicator, i.e., more bulls = bad).

As we anticipated, the 10-year Treasury interest rate peaked mid-month at 4.36% and has drifted lower to 4.09% to close out the month. Lower sentiment and lower rates go a long way to improving return expectations for September despite its checkered past.

Durable rallies exhibit higher highs and higher lows as they progress. As seen in the chart below, there have been three sizable pullbacks since this rally started nearly a year ago. Each pullback began at higher highs and ended with higher lows. Had this one broken the pattern, more confusion and concern would have entered our analysis. Fortunately, the higher highs and higher lows pattern persisted, making August a very positive down month!

Easing Labor Pains

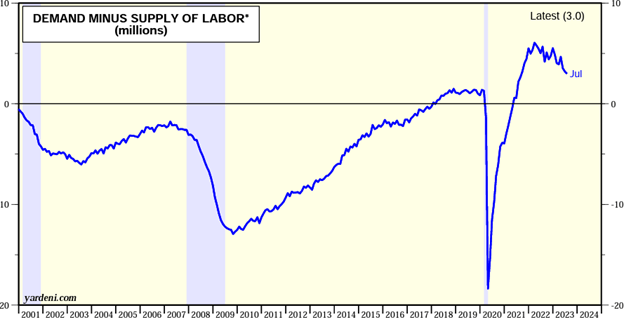

While the disinflation trend pleases the Fed, they have expressed displeasure with the continuing strength of the labor market. This week, we received lots of labor data to interpret before the Fed’s next rate decision date in 17 days. The Job Openings and Turnover Survey release provided encouraging data depicting a decelerating jobs market. Job openings fell to 8.8 million in July after peaking at 12 million in March of 2022, while the US labor force has ticked higher to cycle highs. This increase in labor supply and decrease in labor demand provides trend reassurance for the Fed:

As the demand and supply for workers pursue pre-COVID equilibrium, wage pressures and inflation pressures should further ease. On Friday, the Department of Labor released its monthly jobs report. In August, employers added 187,000 workers to the payroll, while the unemployment rate ticked higher from 3.5% to 3.8%. A surge higher in labor force participation accounts for the higher unemployment rate despite job gains as COVID savings diminish and student loan payments resume.

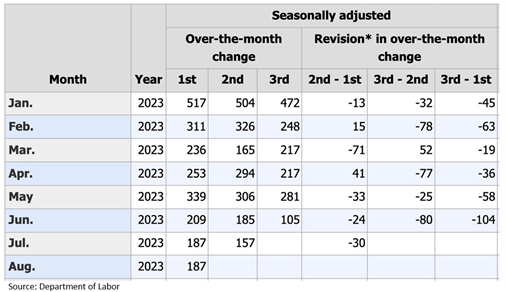

While the increase in supply is encouraging, the increase in demand may be overstated. Each labor report contains job count revisions to previous reports. These revisions can increase or decrease counts significantly. Note the revision trends so far for 2023:

Every month of 2023 has seen downward revisions in payroll counts. For instance, the 209,000 job gains first reported for June have been revised lower by 104,000 jobs to 105,000. Therefore, while the headline job gains for August slightly exceeded expectations, the uptick in participation and the downward revision trends express Fed-friendly labor market weakness beneath the fold.

According to the futures markets, the odds of a September rate hike have fallen to 7%. While September typically provides investors with losses, neutral sentiment, persistent economic growth, disinflation trends, and labor market rebalancing may stoke a September surprise.

Have a fantastic holiday weekend!

David S. Waddell

CEO, Chief Investment Strategist