The Full Story:

Long-term interest rates have drifted higher this month as the US Treasury issued record amounts of bonds to fund the Federal Government’s yawning deficit. Simultaneously, demand for Treasurys has receded due to the Fed’s quantitative easing, commercial banks’ hesitation to take maturity risk after SVBs failure, Japan’s rate increase satiating marginal yield demand, China’s interventions to support the Yuan, and retail cash sorting into money market funds. Translation: More Treasury supply and less Treasury demand forces interest rates higher. But—higher interest rates alone do not cause problems, higher interest rates that come as a surprise do.

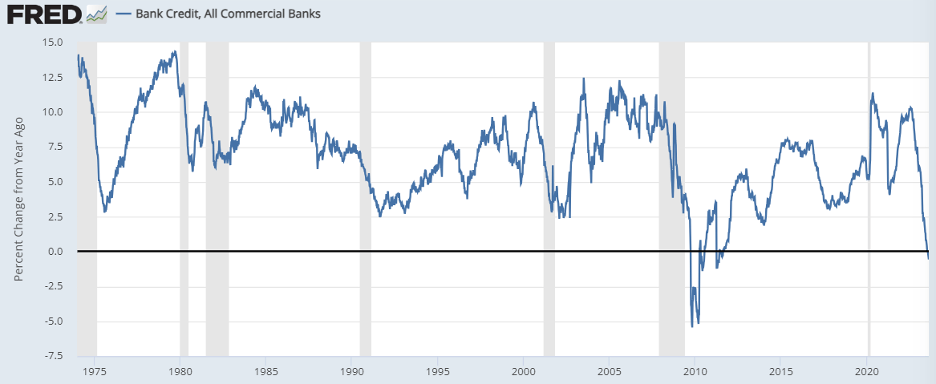

Falling inflation and the Fed’s projections of rate cuts in 2024 should be driving rates lower. Higher rates could catch players offside, creating systematic risks. Recently, Fitch downgraded the US Treasury while Moody’s and Standard and Poors downgraded several banks. Over the last month, the regional bank index (KRE) has fallen 8% while the S&P 500 fell 5%. Over the past year, the bank index has shed 30%, while the S&P gained 7%. Interest rate hikes pressure banks. Pressured banks lend less, transferring pressure to businesses and consumers. Bank credit growth has now tipped negative on the year, adding a clear and present danger for economic growth:

Last year at Jackson Hole, Jerome Powell verbally slammed the brakes on monetary policy. He forecast “pain” for economic participants, promoting recession as the antidote for inflation. Over the next year, the Fed increased rates from 2.5% to 5.5% and shrank their balance sheet by $700 billion. Inflation fell from 8.5% to 3.5% over that timeframe while GDP grew 2.6%. Contrary to Powell’s comments last year, recession wasn’t required to reduce inflation. Therefore, hiking rates further only poses risks to the banking system and economy without clear reward. Should Powell double down on tough talk now and support higher rates to ice inflation, or should Powell try and relieve some of the rate stress plaguing the financial system given inflation’s downward bias? On Friday, Chairman Powell took the microphone at Jackson Hole once again. Here is what he said:

“I Get It”

Powell struck a largely neutral tone. He committed to a 2% inflation target and suggested more inflation would require more austerity. This satisfied the hawks. However, he also acknowledged that monetary policy has reached restrictive levels. Furthermore, he acknowledged that REAL interest rates (rates minus inflation) have risen dramatically with inflation falling.

The rise in REAL interest rates amounts to organic monetary tightening, reducing the need for policy tightening from the Fed. He referred to the auto and goods sectors as examples of rising supply levels driving desired disinflation while also citing a helping hand from falling rents. My read, Powell sees disinflation as more likely than reinflation. The data will have to prove him wrong, which is a much more constructive bias for the markets than the inverse.

On the economy, Powell recognized the reduction in lending and bank credit, and the connection between slowing credit trends and slowing economic trends. He did not suggest that recent rate increases have increased systematic risks, which made him seem willing to tolerate current yield levels.

In all, Powell pacified both market hawks and doves with his neutral stance. This was the right strategy. However, by our interpretation, Powell now sees disinflation as more likely than reinflation. He recognizes that rising real rates will suppress demand further and he acknowledges that monetary drag filters through the economy with a lag. This all reduces incentive for further tightening… unless upcoming data proves overwhelmingly otherwise. In short, Powell gets it.

We will receive July PCE data on August 31st and August CPI data on September 13th. The Fed meets again on September 20th. The market currently places odds of no hike at 80%. On this, we can agree.

Have a fantastic weekend!

David S. Waddell

CEO, Chief Investment Strategist