The Full Story:

On Wednesday of this week, the Federal Reserve released the results of its annual bank stress test. This exercise tests bank solvency against a range of historic hypothetical horribles, including a 6.4% rise in the unemployment rate, a 38% drop in residential real estate values, a 40% drop in commercial real estate values, and various and sundry financial anomalies. Per the results, every one of the 23 large banks passed with well more than adequate capital levels. While investors should feel comforted that the banking system tests well, if risk-averse lending increases their fortitude, shrinking credit pools could increase recession odds. This week we dig inside the banking system’s credit activities to identify which direction credit and recession odds are flowing.

Bank Funding (Liabilities):

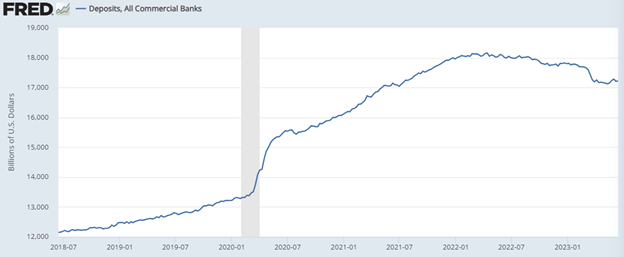

Banks fund the lion’s share of their lending operations with deposits. Recall that relentless deposit outflows precipitated a series of bank failures back in March that required a government tourniquet, leaving depositor confidence shaken. Additionally, the 5% yield gap between sweep cash and money market funds adds further outflow incentive. Nonetheless, after the initial interruption, bank deposits have stabilized and remain well above pre-pandemic levels:

Bank Credit (Assets):

Banks categorize credit at granular levels, but to assess macro conditions, let’s focus on loans to the government, businesses, personal real estate, commercial real estate, and consumers. Banks also loan to each other and use funds for in-house trading accounts, etc., but these “other” categories have idiosyncratic drivers, so we’ve excluded them.

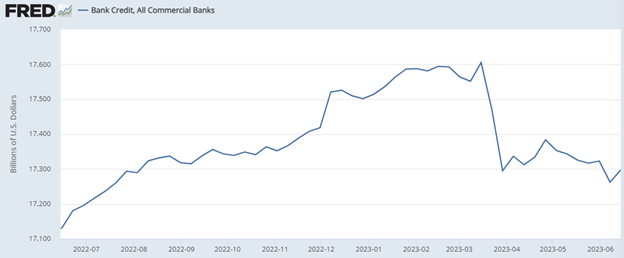

First, let’s look at the trend in bank credit values overall:

As seen above, total bank credit has declined from $17.6 trillion prior to the failure of Silicon Valley Bank to $17.3 trillion today. Let’s now evaluate each sub-category to locate the sources of reduction:

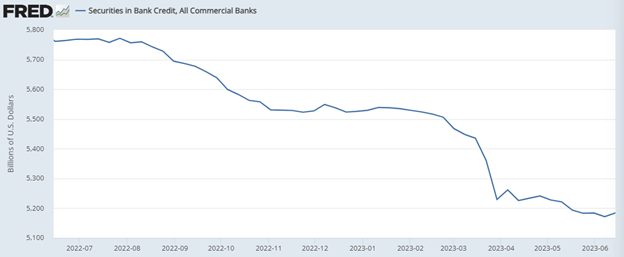

Loans to Government (Securities):

Over the past year, as the Federal Reserve increased interest rates to battle inflation, the value of securities on bank balance sheets (mostly Treasuries) fell significantly. Since the SVB failure, banks have shed $250 billion in securities asset value accounting for 80% of credit reduction.

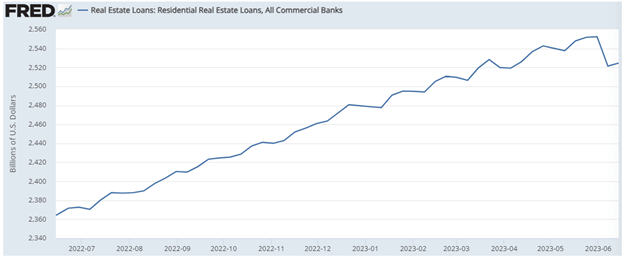

Loans for Personal Real Estate (Consumer Real Estate Loans):

Despite the relentless rise in interest rates, credit remains robust for residential real estate.

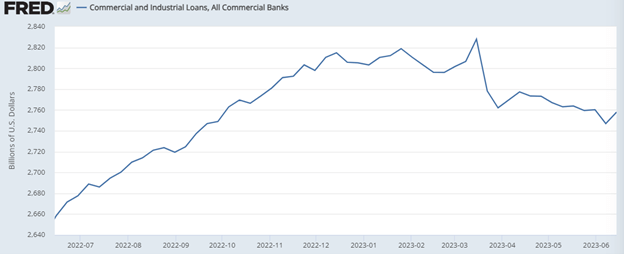

Loans for Business (Commercial and Industrial):

Here we do see more credit reticence post SVB. This comports with the tightening of lending standards on commercial and industrial loans often cited by economists and marginally higher delinquency rates. However, business lending only accounts for 16% of credit overall, making the post-SVB drawdown of $70 billion manageable.

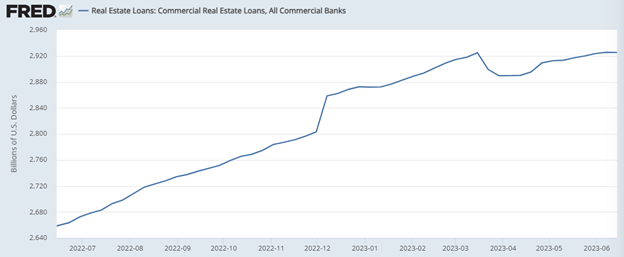

Loans for Business Real Estate (Commercial Real Estate):

Surprised? Yes, since the failure of SVB, total credit values for commercial real estate have RISEN. While many have concerns about credit conditions beneath commercial real estate (particularly office and urban core retail), banks have underwritten these lines very conservatively. Before the housing crisis, banks underwrote nearly all the acquisition costs for homebuyers… remember the No Income, No Job, NINJA loans?! Any decrease in value left the homeowner with negative equity and banks positioned to absorb the losses. Today, banks require real estate developers to contribute significant levels of equity, insulating them from sizable losses. To underscore this point, the Fed’s recent stress test marked commercial real estate holdings down 40%, far more than the markdowns seen during the Great Financial Crisis, and yet, all the banks tested passed.

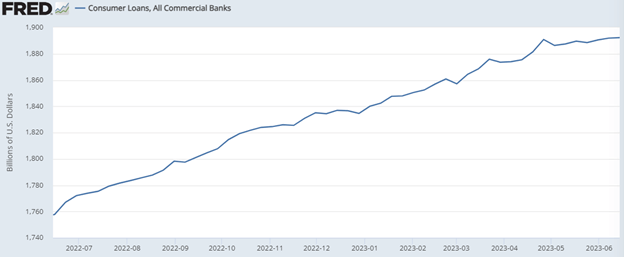

Loans for Consumers (Consumer Loans):

Consistent with the credit conditions for personal real estate, the taps remain wide open for consumers. This makes sense given the excess savings, low unemployment rates, and rising real disposable incomes for US households. While rates have risen, debt service levels for US consumers stand 27% below where they stood before the great recession, making today’s consumers much more creditworthy.

In sum, while bank assets (loans) have declined by $308 billion since the failure of SVB, the declines reside within loans to the government ($251 billion) and loans to businesses ($71 billion). Credit values for consumers and private and commercial real estate remain robust, and loan growth rates remain above pre-crisis levels… providing continued ballast beneath the US economy.

Have a great weekend!

David S. Waddell

CEO, Chief Investment Strategist