The Full Story:

On Thursday of last week, I served on a panel at an Institutional Investor conference in Boston to answer the question “Are we in a recession?”. In my response, I concentrated not only on coincident economic indicators, but also on the more relevant consequences for investors. To investors, the word “recession” conveys more than economic contraction, it conveys corporate earnings compression and investment portfolio drawdowns. Therefore, in practice we have three recessions to assess, economic recessions, earnings recessions, and market recessions.

Economic Recession

Economists look at a host of economic data to gauge the strength and breadth of economic activity. Ultimately, these indicators all filter into Gross Domestic Product (GDP) which measures total spending within the US by households, businesses, governments, and foreigners. Let’s look back over the growth path for the US economy over the past 2 years, for orientation:

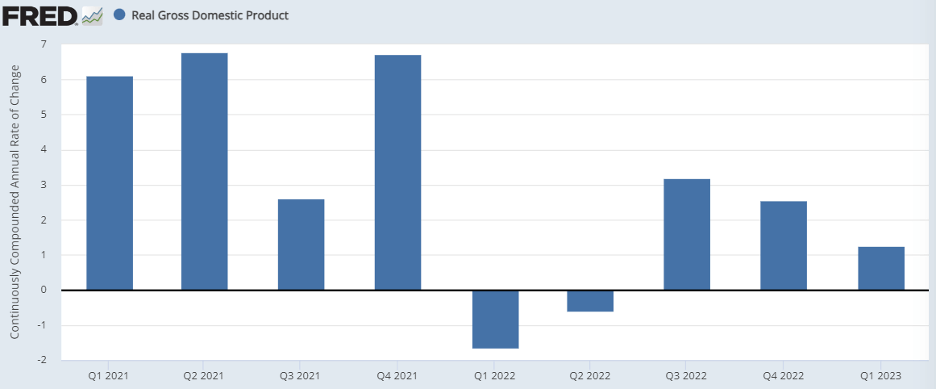

US GDP grew 6% in 2021, fueled by stimulus and cabin fever after the COVID growth collapse. Entering 2022, the economy contracted in real terms as inflation growth rates exceeded economic growth rates. Economists did not consider this an “official” recession due to the robust employment market and high consumer spending levels. Nonetheless, the two consecutive quarters of negative GDP met the traditional “recession” rule of thumb.

The reason I cite this is that the three-recession sequence isn’t as bewildering if you credit the economy with recessing early in 2022. Since then, however, inflation growth rates have fallen faster than economic growth rates leading to a rebound in real GDP growth, up 3.2% in Q322, 2.6% in Q422, 1.3% in Q123 and on pace for another lower, yet positive reading for Q223. Taken collectively, the US economy has achieved less than a 1% growth rate over the last six quarters. While we have yet to officially enter recession, we wouldn’t have to slow much to enter one. Remember, the Federal Reserve called for recession as the antidote for our inflation infection. With recession as policy, no one would be surprised by its arrival… and in fact, in some ways we have already accounted for it… as follows.

Market Recession

Stock market performance today reflects investor projections of the future. When the Fed declared its war on inflation a year ago, investors had to incorporate recession projections into market prices. Historically, over the last 12 recessions, the S&P 500 fell 24% at the median. Consequently, between January and October of 2022, investors marked down US stock prices 25%. Mission accomplished! With the market recession accomplished, the market recovery could begin. Referring back to history, following those recessions, stocks rose 26%, at the median, over the next 12 months. As of Thursday’s close, the S&P stands 23% above its intraday October low. Mission nearly accomplished! While the economic recession hasn’t occurred yet, the market recession already has.

Earnings Recession

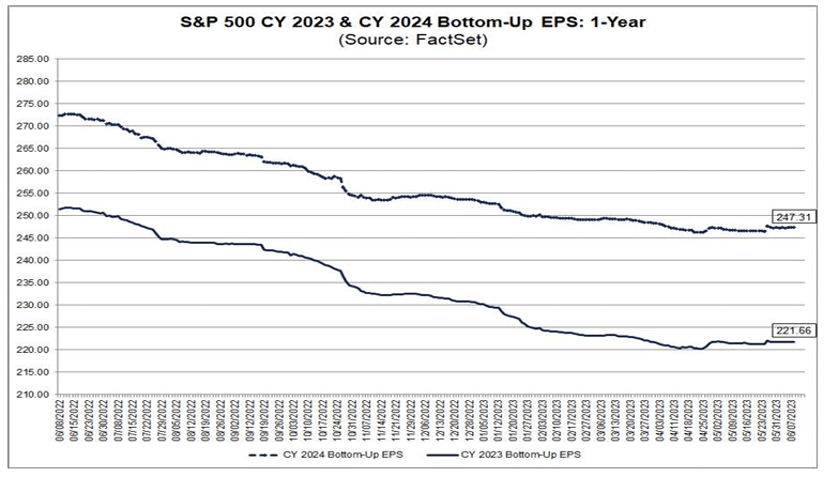

Once the Fed declared recession as a policy, analysts began marking down earnings expectations. Non-inflation-adjusted earnings (the only way they are reported) peaked in Q222. Typically, in recessions, S&P 500 earnings fall 13%, at the median. Knowing this, analysts quickly marked down earnings expectations 10% off of those peak levels. While earnings have declined, the declines have been more minor than feared. In fact, last quarter could mark the nadir with earnings contracting only 6%. Analysts peering into next year see earnings rising 12.4%. Perhaps those numbers are too high as the future is hard to predict. However, it’s the trend that spends and analysts have been raising forecasts, further underpinning this market rally:

While still within an earnings recession, analysts believe we are closer to the end than the beginning.

Enjoy your Sunday!

David S. Waddell

CEO, Chief Investment Strategist