The Full Story:

As anticipated, our government has resolved the 2023 debt ceiling issue by not addressing our debt issue. Let me explain.

- The US government will spend $6.2 trillion in 2023. Within the $6.2, the Medicare, Medicaid, and Social Security entitlement programs account for $3.8 trillion. The national defense budget accounts for $800 billion. The interest due on the Treasury debt accounts for $640 billion. The sum of these line items totals $5.2 trillion. Politically, these items are “non-negotiable.”

- This year, the government estimates it will receive $4.8 trillion in tax revenue.

- Therefore, the “non-negotiable” budget deficit equals $400 billion.

- Within ten years, the growth in the entitlement programs, the defense budget, and interest payments elevates this annual “non-negotiable” deficit to $1.4 trillion, 3.5x larger than today.

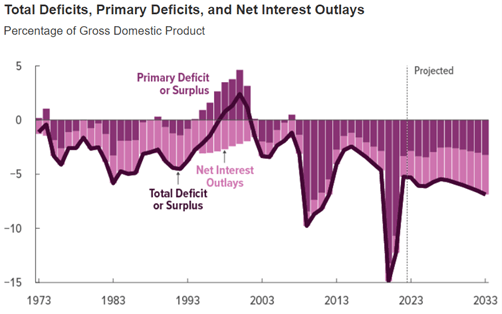

- The “negotiable” items, known as discretionary spending, amount to $900 billion. This is just 14.5% of total government spending. Therefore, capping discretionary spending for two years, as negotiated, has nearly zero impact on our national balance sheet. As calculated by the Congressional Budget Office (CBO), here is where deficits are headed:

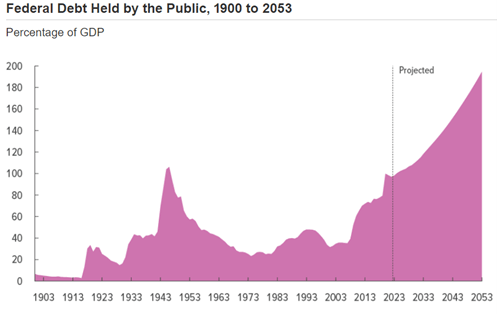

And just to further salt the wound, here is CBO’s estimate of total government debt to GDP over the next 30 years:

Great job, guys!

Friday’s unemployment report contained many contradictions. While US employers reported adding 339,000 new employees, US households reported their unemployment status deteriorated from 3.4% unemployed to 3.7% unemployed. This divergence has led to intense head-scratching, but for our purposes, it’s academic. They use two different survey methods that periodically disagree. What matters most to the Fed is the trajectory of wages. As we entered 2023, we anointed average hourly earnings as the most important data point for the year. With 12 months in the year, that means 12 innings in our Wage Bowl (yes, I realized I mixed metaphors, hang with me). The Fed declared wage inflation the root cause of persistent inflation and, therefore, the target of their tightening. Should wages fall more than they rise, Fed policy will loosen… WIN. Should wages rise more than they fall, Fed policy will tighten… LOSE. It’s binary. Now, let’s check the score!

Wages have fallen sequentially in three of the reports while rising in two, for a slim advantage. However, the current level of 4.3% stands .5% below the December season opener for a wage inflation decline of 10%. Furthermore, the 4.3% level matches the lowest level since July of 2021, before all of this inflation consternation began. The Fed wants this number to fall to 3%. At the current pace, that would occur in about a year, assuming economic growth remained at this level. Any deceleration in the economy would lead to a further slowdown in wage inflation. So, if the Fed is in a hurry, they can force recession, but why be in a hurry when the trend is your friend? This reinforces the case for a rate pause in June. The market agrees as the odds of a June rate hike have fallen to 35%. If that proves true, it’s time to dust off our “what happens historically when the Fed pauses” playbook:

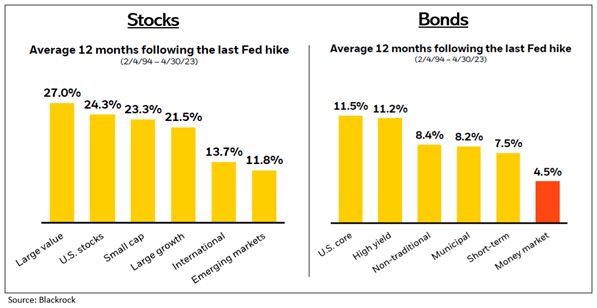

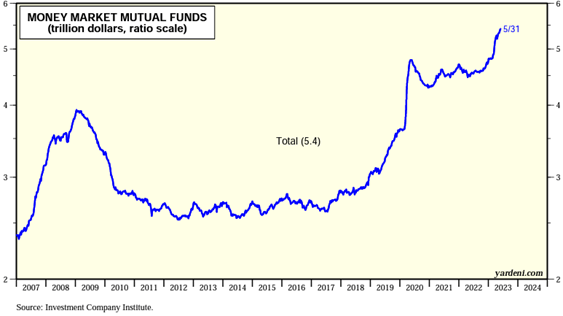

Over the last 30 years of data, rate pauses have proven highly profitable for investors. US stock investors have seen 24% average gains, while US bond investors have seen 11% gains. Both of these well exceed the historical return on money market funds over the time period. That’s something to ponder with Money Market Funds currently at historic levels:

They say history doesn’t repeat itself, but if it rhymes, this rally has plenty of fuel to burn.

Have a great weekend!

David S. Waddell

CEO, Chief Investment Strategist