The Full Story:

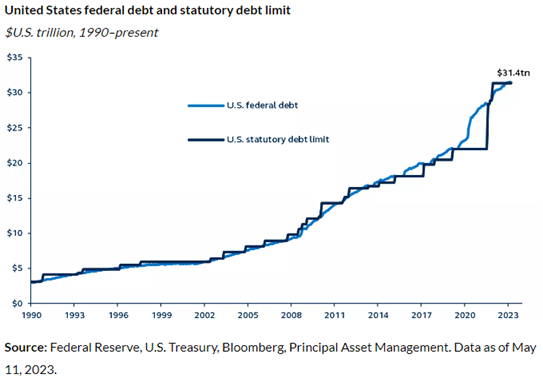

In 2008 and 2009, the Government took unprecedented actions to offset the Great Financial Crisis. Congress authorized the distribution of nearly $1 trillion in fiscal stimulus, while the Federal Reserve cut interest rates to zero and printed and injected $1 trillion+ in quantitative easing. This level of Government intervention in reaction to a “100-year economic event” shocked many market observers. Books filled shelves with writings about fiscal recklessness, financial profiteering, and Government overreach. Bailout Nation, Contagion, Endgame, The Big Short, The Sellout, and countless more sit on my shelves in a strong rebuke to what led to and what prevented the GFC. Occupy Wall Street Protests hit the streets, and the Tea Party hit the hill. Suddenly everyone became hyper-aware and hyper-sensitive to the Government deficits and accumulated debt. Warnings of hyperinflation, record interest rates, and collapsing dollars captivated audiences and nurtured the public animus that metastasized into the Obama vs. Tea Party debt limit stalemate in 2011. Ultimately, the parties found common ground, but not before Standard and Poor’s downgraded US Treasury debt, not upon fundamental merits, but in recognition of legislative dysfunction. Therein lies the crux. The chart below captures not only how much debt the US has accumulated since 1990 but also how many times legislators have fought and agreed to raise the limit.

Therefore, as the post-COVID debt ceiling crisis rages, the right question to ask is… does the US have a debt problem or a legislative problem?

The Fiat Effect

President Nixon closed the gold window in 1971, effectively ending the US Dollar’s convertibility into gold. This removed many legislative and monetary restraints and forced the Federal Reserve and Congress into the fiat backstop role gold had played to date. Unsurprisingly, the stock of accumulated debt rose significantly over the next 50 years. In fact, when Nixon closed the gold window, the US Treasury owed bondholders $400 million versus $31 trillion today. Over the same period, US GDP grew from $1 trillion to $25 trillion. Therefore, while the economy grew by 25x, US Treasury debt grew 82x. This should have profoundly impacted currency values, inflation rates, and interest rates, as widely espoused. But did it?

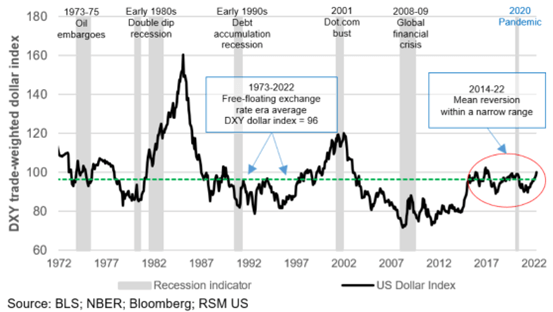

The US Dollar

While US debt climbed 82x over the period, the US Dollar vacillated within a range of 60% higher to 30% lower. Today, the dollar sits slightly below its 1971 divorce from gold level and right at its 50-year average.

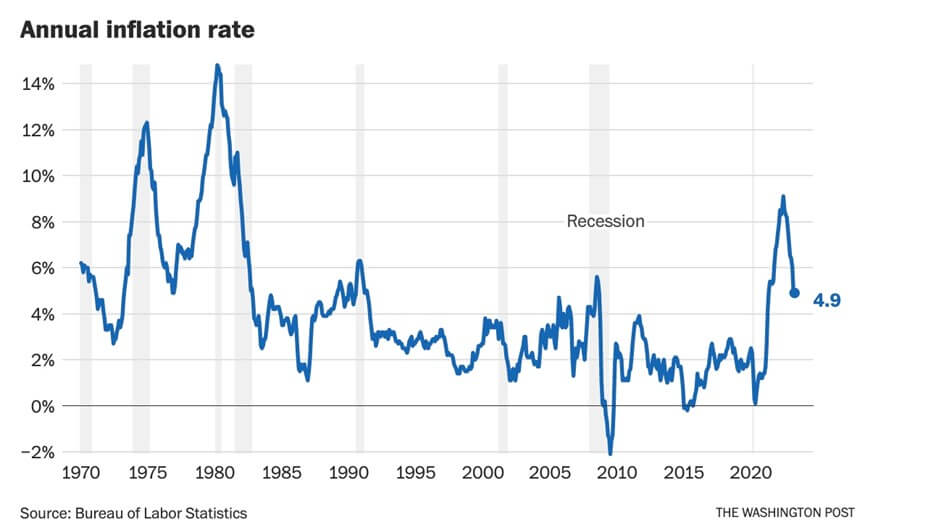

US Inflation Rates

While COVID profligacy led to a recent spike in inflation, the Consumer Price Index today sits well below its 1970 comparison. So, while US Treasury debt levels climbed 82x over the period, average US inflation rates have fallen significantly.

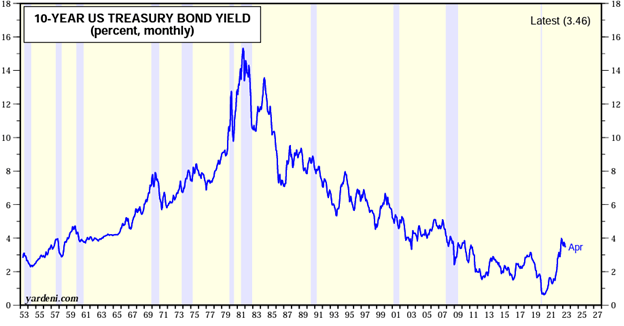

In alignment with the trajectory of US inflation rates, US interest rates have fallen since the 1970s, interrupted only by the COVID stimulus shock. So, while US Treasury debt levels climbed 82x over the period, US Treasury rates have fallen significantly.

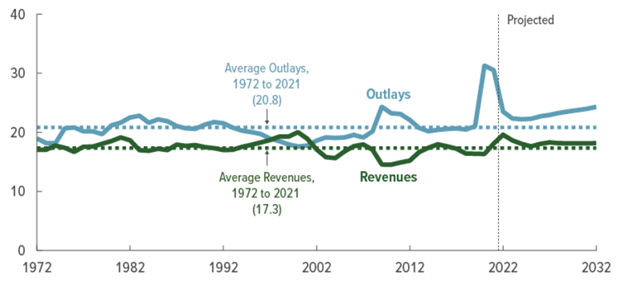

Remember, US Treasury debt grows only if the government spends more than it receives in tax revenues. Surprisingly, the percentage of each stream when compared with the size of the economy hasn’t changed that much since the 1970s:

As you can see, tax revenues have hugged their long-term average for the last 50 years. In fact, under Bill Clinton and Newt Gingrich (remember that shutdown?), the US ran a budget surplus into the year 2000. Since then, most of the debt accumulation has occurred in reaction to the GFC and COVID. Going forward, the CBO does project spending will rise more than revenues as Medicare, Medicaid, and Social Security consume more of Federal finances without scope for equivalent offsets in discretionary spending. These programs require reform to adhere to our fiscal norms of 3% average deficits, which get conveniently erased by 3% average inflation.

In summary, the 82x spike in US Treasury debt has negative cognitive consequences but few obvious economic ones. The US Dollar has vacillated higher and lower within a range but sits at its long-term, post-gold-standard average today. US inflation rates have fallen from 6% in 1970 to 4.9% today on their way back to their pre-COVID 2% levels. US interest rates have fallen from 7.5% in 1970 to 3.5% today on their way back to their pre-COVID 2.5-3% levels. Meanwhile, the US economy grew 25x. Arguments can certainly be made that more Government means less productivity and that crowding out the private sector has societal consequences, and I believe that narrative. Still, it’s virtually impossible in economics to prove “what would have been.” Will the US Government reach a point where the global financial markets capitulate, expel the US dollar from their reserves, drive inflation to Weimar levels, and drive interest rates stratospheric? Maybe. But consider that Japan has a debt-to-GDP ratio of 230% versus our 130%, and issues 10-year Government bonds with interest rates of .4%. US Government debt dynamics do not resemble household debt dynamics. Our Grecian moment may exist… but it’s a long way from here.

So, while economists largely agree that the long-term path for US debt accumulation is “unsustainable,” no one knows where the limit lies. Furthermore, while the debt limit fosters annual political conflicts over sustainability, the debt limit always rises and will continue without sweeping entitlement reform. In reaction to political pressures, President Obama tasked the Simpson-Bowles Commission with designing a fiscal path to stabilize the debt. They did just that. Unfortunately, the political will did not exist at the time to turn the recommendations into legislation. But someday, this may change either through courage or through crisis. But for now, the US debt load causes more political problems than economic ones.

Have a great Sunday!

David S. Waddell

CEO, Chief Investment Strategist