The Full Story:

As expected, markets hit an air pocket after rallying strongly through the first six weeks of the year. With investor sentiment high as a spy balloon, it only took a few hotter-than-expected economic and inflation missiles to bring it down. That’s the irony of the market today. The market wants a mild recession because the Fed wants a mild recession. Without one, a stronger and more resilient economy goads the Fed into continually tightening policy, which increases the odds of a not-so-mild recession. So, perversely, positive economic surprises make for bad news. Note the following:

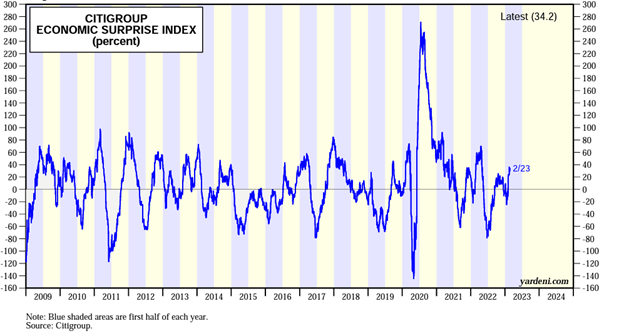

The Citigroup Economic Surprise index represents the sum difference between official economic results and forecasts. A number greater than zero conveys a period of better-than-expected economic data, while a number less than zero conveys a period of worse-than-expected economic data. Notice that from the 3rd quarter of last year into January of this year, the Surprise percentage fell from +20% to -20%. This corresponded with a near 20% advance in the S&P 500. However, over the past couple of weeks, the index has shot higher from -20% to +34%. While that’s great news for Main Street, it’s bad news for Wall Street. The surprising economic results drove the US dollar, interest rates and rate expectations higher, while driving sentiment, valuations, and stock market indices lower. But if the economy grows instead of shrinking, are we sure that’s bad?

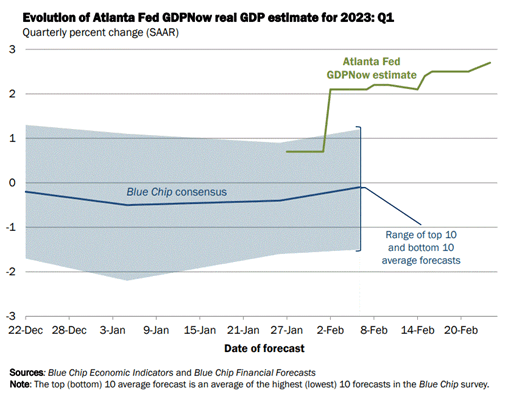

The Atlanta Fed updates its growth estimate for the current quarter with nearly every economic release. As expected, their forecast has risen as the positive economic surprises have risen:

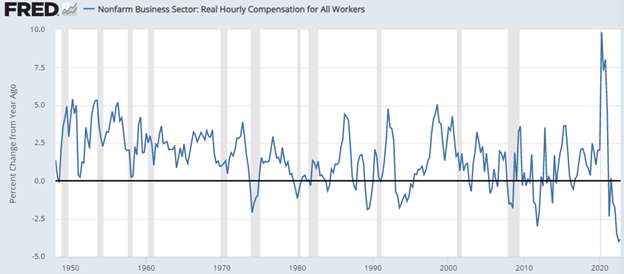

Per the Atlanta Fed’s estimate, the economy is on pace for a 2.7% growth rate in the first quarter compared with the Blue Chip economist’s flat to negative forecast for the quarter. This also follows a 2.7% GDP growth rate in the fourth quarter, hardly the stuff of recessions. Adding 6% inflation back to real GDP of 2.7% provides a nominal GDP growth rate of 8.7%. That rate better correlates with the corporate revenues opportunity as revenue and earnings reports do not subtract inflation. Therefore, more robust corporate revenues in the first quarter should ballast corporate earnings. If you haven’t hit your econ tolerance threshold yet, I have more. Headline inflation of 6% runs above wage inflation at 4%. That spread benefits corporations, not employees, further ballasting earnings.

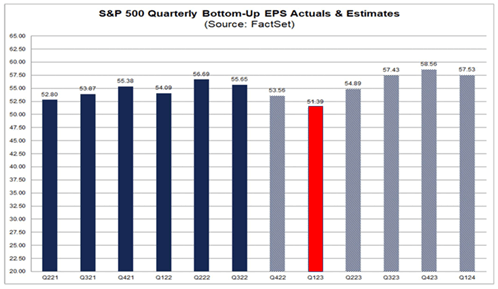

Therefore, the combination of stronger-than-expected economic data and headline inflation rates remaining above wage inflation rates suggests that economic and inflation surprises could translate into earnings surprises. Analysts currently expect Q1 revenues to grow an anemic 1.8% (consistent with the Blue Chip no growth forecasts) while earnings fall 5.7%, marking the lows for the year:

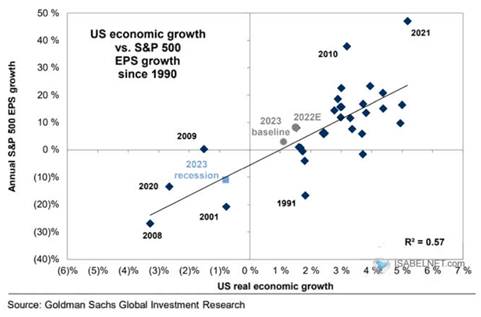

Should the economy remain resilient, this forecast either must roll forward or revert as earnings track the economy higher. Nothing is certain, but the correlation between GDP growth and earnings growth over the last 30 years makes a compelling case for upside surprise:

Surprising earnings growth either drives stock prices higher or stock valuations lower. Either way, the value proposition for investors improves.

Enjoy your Sunday!