The Full Story:

Markets gained another 4% this week, now standing 12% above its most recent low, despite a soft GDP report, big tech earnings disappointments, and China’s political retreat from economic reform (I’ll hit each of these topics with more detail below). Because the globe worries most about tight monetary policy in the U.S. leading to financial instability, bad news is seen as good news if it subdues the Fed. And it may. The Bank of Canada raised rates 0.50% this week rather than the 0.75% expected, and the European Central Bank raised rates 0.75%, as expected, but softened their forward guidance. Relying on the 2-year U.S. Treasury bond as a proxy for Fed policy rate expectations, yields fell from 4.5% to begin the week to 4.4% to close the week. The 0.10% change may seem small, but in the current yield game, it’s the direction that matters!

Growth-ish

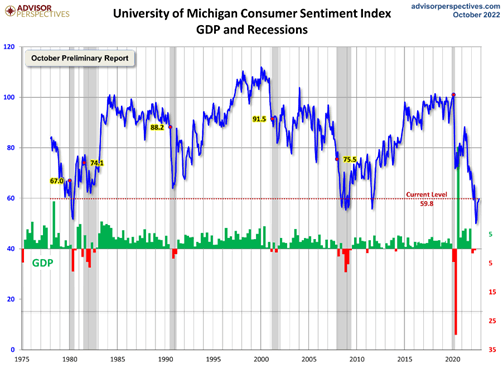

The U.S. Government released its preliminary Q3 GDP report this week. Encouragingly, the economy grew 2.6% overall in the second quarter. Discouragingly, energy exports, increased government spending, and smaller inventory builds accounted for the advance. Domestic final private demand, which excludes government spending, trade, and changes to inventories, grew a measly .08% — otherwise known as not at all, accounting for the weakest reading since the pandemic shutdown. Housing activity has collapsed under the weight of 7% mortgage rates, creating a major drag on GDP. Consumption, which accounts for the largest proportion of the economy, has also weakened considerably as COVID consumer savings levels evaporate. Consider these visuals on consumer savings (spending dry powder) along with consumer sentiment (spending enthusiasm):

With consumers out of stimulus ammunition, housing investment collapsing, retailer inventories now replenished, and outsized trade contributions unlikely to last, the GDP report depicted an economy slowing, not growing, despite the campaign-able headline number.

Market De-Fangs

Disappointing earnings results from Google, Meta (formally known as Facebook), Microsoft, and Amazon punished their individual stock prices this week without infecting the stock market overall. Given the outsized influence of the Mega Cap technology names, this is an extremely healthy indicator. To put the scale of these behemoths into context, Microsoft and Apple account for 50% of the S&P 500 information technology sector’s market capitalization; Google, Meta, and Netflix account for 40% of the communication services sector’s market capitalization, while Amazon alone accounts for 31% of the consumer discretionary sector’s market capitalization. As a group, they comprise 20% of the entire S&P 500 market capitalization. For the FAANGs to fall while the market rises suggests a rotation of capital within the market AND more overall buying than selling market-wide. Additionally, the share price comeuppance informs big tech management that the rules of finance apply to them as well. This brutal rebuke will undoubtedly induce less bloated, entitled, conglomerated franchises, improve risk/reward characteristics for shareholders, and rebalance distorted index weightings overall. Having the vaunted FAANGs 4% lower on the week with the broad market 4% higher may be the most encouraging development of the year!

China Reddens

In an ominous video that broke the internet, former Chinese President Hu Jintao was forcibly ejected from the National Congress as Xi Jinping became “ruler for life.” This grotesque show of autocratic power led to a swift marketplace firesale on all assets Chinese, as Hu’s removal signified the removal of his economic reform and openness agenda. While Xi’s consolidation of power has war vigilantes abuzz about an imminent military invasion of Taiwan, having lived in Hong Kong, I will contend that China has much more subtle ways of reassuming territories, if so desired. More concerning is the abandonment of the Chinese grand bargain. The Communist leadership in China has believed for the last 40 years that enriching the population provided them the safety and security to rule. By consolidating power at the state level while broadcasting a confusing and encroaching array of regulations, the Communist Party seems less compelled to support economic growth and development as a pre-condition to rule and more inclined to direct development for political purposes under the force of rule. In response, the largest China exchange-traded fund (ticker: FXI) fell 10% on the week. For the global economy, this issue of China’s growth has larger implications. China has provided the bulk of worldwide economic growth for decades, and without China as an economic engine, growth rates worldwide will downshift. The middle-income trap that has limited many developing economies as legacy political systems restrict GDP per capita growth may have sprung in China. Let’s hope not… for growth’s sake!

Mail Call!

Across our models, we made numerous trades this week. Across thousands of accounts, we booked tax losses, rebalanced allocations, and put more capital to work where appropriate. These technical activities align with our year-end strategy outlined in our September 25th email:

Here is our year-end playbook:

- Continue harvesting tax losses wherever possible

- Reinvest proceeds to maintain market exposure

- Add cash weekly or bi-weekly, and be fully allocated into asset allocations by Halloween

- Should the market cascade lower between now and then, accelerate purchases

This explains the cascade of confirmations in your mailboxes. Remember, we invest our own personal assets within the same investment models we recommend for you. When we trade, it happens in our accounts and your accounts simultaneously. We are truly all in this together!

Have a great Sunday!