The Full Story:

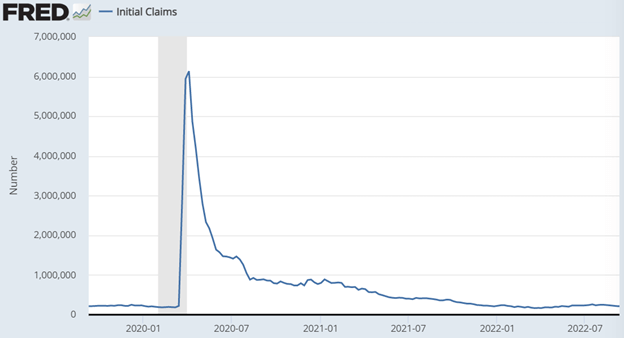

As FedEx detailed on Thursday, the lockdowns in China, the war in Europe and policy tightening in the U.S. have upended shipping volumes. Fewer goods circling the globe in boxes translates into less global GDP. Less global GDP means less corporate revenues and less corporate profits to share. Less corporate profits mean less employees. Less employees means less wage pressure. Less wage pressure means less inflation. The Fed believes layoffs will cure inflation. Unfortunately, we haven’t seen any. Note the chart below which chronicles unemployment claims:

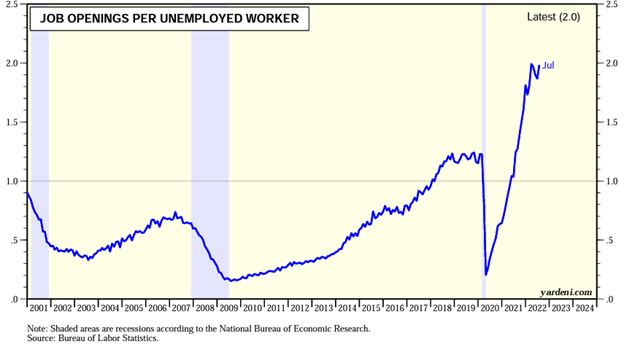

Initial unemployment claims have shown little uptick as of late and continue to plumb the record lows seen earlier this year. The Fed clearly still has work to do. But how many layoffs does the Fed need? This has become a hot topic of debate and has reanimated the long-forgotten Philips curve. For those who slept through macro-economics, the Phillips curve posits that inflation and unemployment are inversely correlated; i.e., more employment means more inflation, and more unemployment means less inflation. According to Phillips-curve adherents, dousing inflation by the end of next year would require the Fed to engineer a recession to drive the unemployment rate up between 4.5% and 7%. The increase in unemployment would depend on how aggressively the Fed wants to decrease inflation. If the Fed can stomach 3% inflation, it needs to destroy 2 million jobs. If the Fed wants to hit its 2% target, it needs to destroy 5 million jobs. But before the job reductions occur, the job openings must evaporate:

And while the pace of job openings has slowed, there are still two job openings for every one job seeker. Therefore, the Fed needs millions of “Looking for Work” signs tomorrow to replace the millions of “Help Wanted” signs today. That’s what Powell meant when he prescribed “pain” as the cure for inflation.

How Much Pain, Mr. Powell?

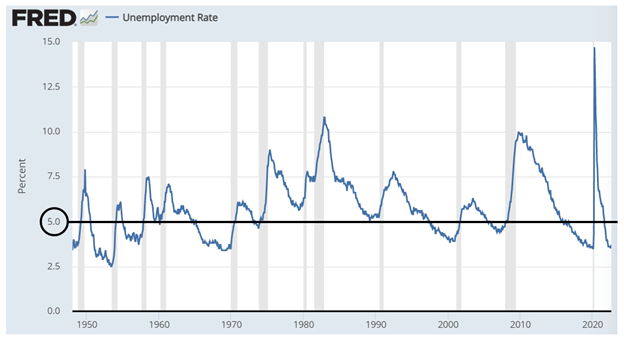

Of course, there are degrees of pain. During the COVID lockdown, 22 million jobs were shed which amounted to 14% of working Americans. During the Great Financial Crisis, 9 million jobs were shed or 6% of working Americans. During the 2002 recession, 2.6 million jobs were shed or 2% of working Americans. During the Volker recessions, 1 million jobs in 1980 and 2.8 million jobs in 1982 were shed, or 1% and 3% loss of working Americans, respectively. If the Fed must press unemployment up by 2 million to hit its Phillips-curve derived inflation target of 3% by the end of 2023, that is 1.3% of today’s working Americans. While “painful”, this reduction registers on the lighter side of the historical range. In fact, an increase to 5% unemployment, from 3.7% today, would still lie below the long-term average unemployment rate of 5.7% going back to 1948:

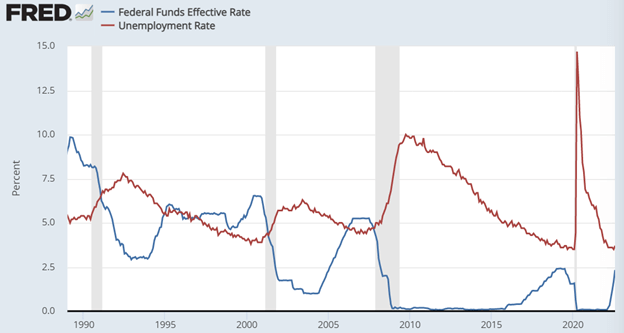

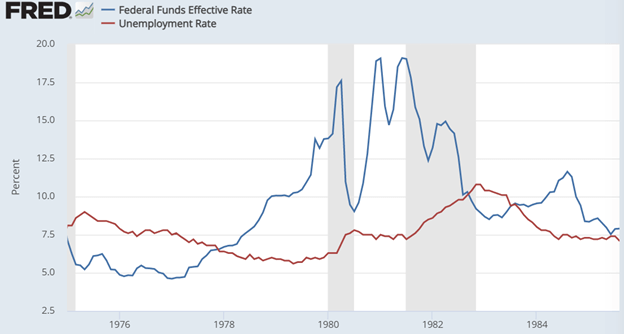

Unfortunately, the economy responds to infinite variables in addition to Fed policy. So, while the Fed might neatly land the economy at 5% unemployment and 3% inflation “ceteris paribus” (a nod to those of you who didn’t sleep through class), it is easy to see from the chart above that movements in rates tend to overshoot and undershoot their tidy targets. And while the Fed might like to see somewhere between 2 and 5 million Americans unemployed to fight inflation, those Americans vote. Note the speed with which the Fed has historically cut rates when unemployment rates begin to rise (I started this series in 1989 to reduce eye strain):

This relationship between rising unemployment and rate cuts held true even during the “unflappable” Volker era. Remember that the U.S. had only come off the gold standard a decade earlier, so the clumsiness of the rates reflects the inexperience of the Fed. Today’s Fed has more experience and more tools which reduce the wild rate volatility of yore. Nonetheless, look at the speed with which Volker cut rates as unemployment rose:

While the Fed may prescribe “pain” to stimulate layoffs, the historical record suggests they may get more than they bargain for, forcing them to reverse rates quickly in 2023. That is not the base case in the market right now, but that is mine for 2023.

WIFM (What’s In It For Me?)

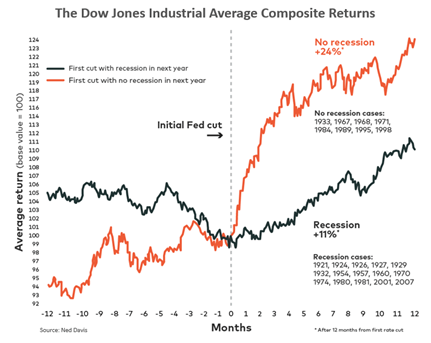

On average, markets rallied 16% over the following year after the first-rate hike. Without a recession during the year, returns jump to 24%. With a recession during the year, they fall to +11%. Therefore, should the Fed overdo austerity (likely) and need to reverse course in 2023, history bodes well for intrepid investors.

Have a great Sunday!