The Full Story:

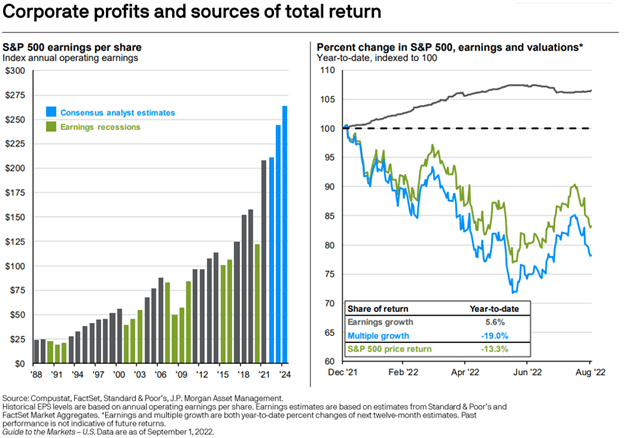

The market closed lower again this week, still smarting after the Fed’s scolding. We deserve it. The 17.5% rally off the June lows taunted the Fed. As investor sentiment rallied along with stocks, so did inflation expectations. Since happiness seemingly correlates with inflation expectations, if the Fed wants inflation expectations to fall, they need unhappiness to rise. That’s why the recent barrage of Fed comments has felt like corporal punishment. We are being punished for partying! The good news is that sentiment and inflation expectations are falling quickly, setting us up for some support near these levels. I don’t expect the market to rally from here, but I don’t expect a collapse either, barring an unforeseen event. Remember that earnings have been growing while the market has been dropping. This chart from JP Morgan captures the story well:

On the left side, we have past and projected earnings for the S&P 500. On the right, we have year-to-date performance for the S&P 500 and the contribution of earnings and P/E to that return. Note that earnings have contributed 6% to returns, while P/E compression has detracted 19% from returns through August. Analysts currently project continued earnings growth in 2023 and 2024. These growth rates may prove optimistic if recession bites, depressing the E. But if that’s the case, recession will also wipe out inflation, supporting the P/E. It may take more time to resolve the issues plaguing policy makers and the economy, but I don’t think it takes more downside than we have seen.

Biden vs. Powell

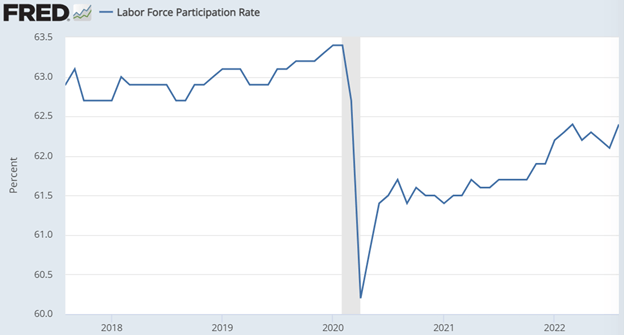

Friday’s employment report balanced things to like and things not to like well. The U.S. economy added 315,000 jobs last month, but because the labor force participation rose, the unemployment rate also ticked higher to 3.7%. The Fed wants to see the unemployment rate rise to 4%+, so this was a step in the right direction. The stubborn “great resignation” and “quiet quitting” has robbed the economy of labor supply and productivity. An uptick in the participation rate allows for an increase in labor supply to reduce wage pressures, relieving some pressure on the Fed to decrease aggregate demand to reduce labor demand. Households have drawn down savings levels recently, which may renew their interest in work. Note the drawdown but encouraging recovery in participation contained in this month’s report:

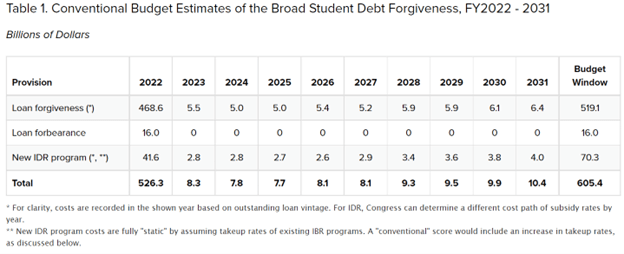

Adding workers faster than jobs accounts for the simultaneous uptick in employment and the unemployment rate. Something for everyone! Unfortunately, elimination of debt amounts to an increase in savings. According to Penn Wharton, the Student Loan Forgiveness subsidy will amount to $526 billion in stimulus this year… and a few more billion down the road:

This could weigh against progress made in the participation rate. It’s too early to tell. What is clear is that the combination of this $526 billion, the $400 billion recently passed on climate initiatives, and the $280 billion subsidy for semiconductors adds up to another $1 trillion+ of stimulus while the Fed tries to downforce demand. Having fiscal stimulus and monetary constraint policies at odds makes things much harder for the Fed. Not only do they need to mop up the excess stimulus of the past, but they now must also adjust for the stimulus of the present. This makes their pursuit of normalizing the labor market even more difficult. With any luck, gridlock will pause fiscal profligacy, raising the stakes even higher for the upcoming mid-terms.

Enjoy the holiday weekend!