The Full Story:

By mandate, Congress holds the Federal Reserve responsible for general “price stability.” Congress does not hold the Federal Reserve responsible for “asset price stability.” Therefore, Fed officials largely ignore price gyrations in stocks, houses, bitcoin prices, etc. when setting policy, other than as anecdotal input. For instance, excessive valuations on the NASDAQ back in 1996 triggered Greenspan to coin the term “irrational exuberance,” and yet the federal funds rate remained constant. The Fed also largely disregarded the housing bubble in the late 2000s as general inflation levels were mostly within their target range. In fact, most Fed officials see asset price inflation as “good” inflation, and general price inflation as “bad” inflation. Therefore, as long as “bad” inflation behaves, “good” inflation can rise indefinitely.

Jerome Powell’s forceful response to the COVID pandemic led to the largest amount of monetary stimulus in history. The response in the asset markets was immediate. Between March of 2020 and January of 2022, crypto prices rose 1000%, stock prices climbed 100% and house prices rose 40%. These extreme advances led to a 30% surge in household net worth across the United States, the strongest advance in US history.

That is not “good” inflation, that’s “GREAT” inflation!

Unfortunately, excessive stimulus, supply constraints, and COVID shutdowns also ignited “bad” inflation, the most concerning and consequential of which is rent inflation. Rent inflation accounts for over a third of headline inflation and typically lags real estate price increases considerably. For example, housing prices began shooting higher around June of 2020, and yet rent inflation continued falling until February of 2021. It has grown steadily ever since.

In the most recent report, rent inflation rose 5.6%. That’s the largest annual increase since 1990. Even in the housing bubble of the late 2000s, rents didn’t rise this much. While the link between a hot stock market and hot inflation isn’t clear, the link between a hot housing market and hot rent inflation makes the link to general inflation crystal clear. Unfortunately for homeowners, for the Federal Reserve to whip today’s “bad” general price inflation, they need to whip the “good” asset price inflation in housing.

Setting their Sights

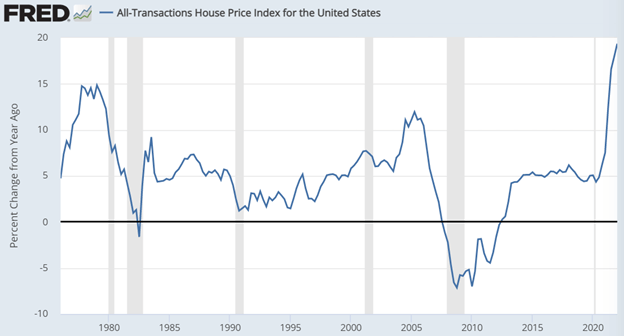

Over the last twelve months, house prices across the United States of America rose 20%. This escalation dusts the 9% peak annual increase seen at the height of the housing bubble. For visual reference of how extremely generous this environment has been to homeowners, see below:

For buyers, it’s a different story. While house prices have risen 20%, wages have only risen 5%, making ownership a stretch. To compound the difficulty, mortgage rates have doubled so far this year. Taken together, housing affordability for purchasers has cascaded to record lows:

In theory, with housing affordability at record lows, prices paid should begin declining and listings should rise as sellers panic and buyers strike. Let’s test the theory.

Nashville, TN has been one of the hottest residential real estate markets in the country. The All-Transactions Price Index for Nashville shows a 27% increase year over year, well above the national average (for comparison, during the housing bubble, Nashville home prices peaked at a measly 9% growth rate). The median sale price for a home in Nashville recently hit a record of $460,000 against the national average of $428,000.

According to Redfin data released this week, the winds have changed. The median sale price for a Nashville home ticked lower by 2% in June. Nashville homeowners must be well attuned to price trends as the number of home listings also rose 16% last month and stand 30.5% higher than this time last year.

Theory proven.

Nationally, the numbers are more sedate, but directionally consistent. The number of homes for sale nationally grew 2% overall in June, the first annual increase since July of 2019. The total number of homes sold fell 16% and listings rose 2.4%. Based upon these trends, consistent with the Fed’s mandate, real estate disinflation has begun. How far will prices fall? Unknown. But for reference, publicly traded real estate investment trust indices have fallen 20% year to date, while home values lost 30% during the Great Financial Crisis.

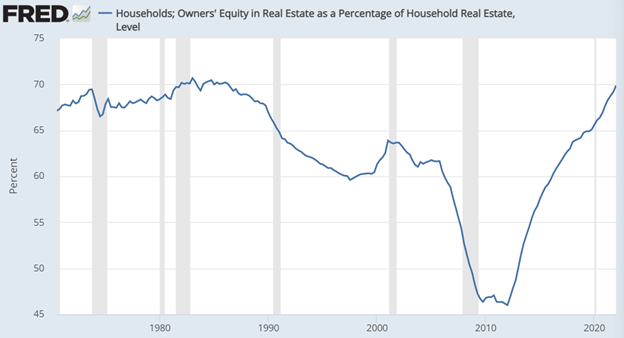

Before you yell “CRISIS!” know this: homeowners are much better positioned going into a price correction than they were in 2008. Examine the chart below showing homeowner equity levels:

This means that the Fed can force down house prices without imperiling homeowner solvency. Additionally, the US banking system reforms instituted after the crisis forced banks to fortify balance sheets. All 33 banks recently stress-tested by the Fed passed easily.

The Fed needs general price levels to fall. Consequently, they have raised rates aggressively and begun quantitative tightening to restrict aggregate demand. Asset markets have responded. Crypto markets have fallen 80%, the stock market has fallen 20%, and the bond market has fallen 10%. The housing market has yet to correct, yet it holds the most direct relationship to general inflation through rent computations. The Fed needs rental rates to fall as they comprise the highest weighting in inflation indices. This will require real estate prices to fall. Fortunately, homeowners and banks have strong enough balance sheets to withstand price declines… without triggering another Great Financial Crisis.

Have a great Sunday!