The Full Story:

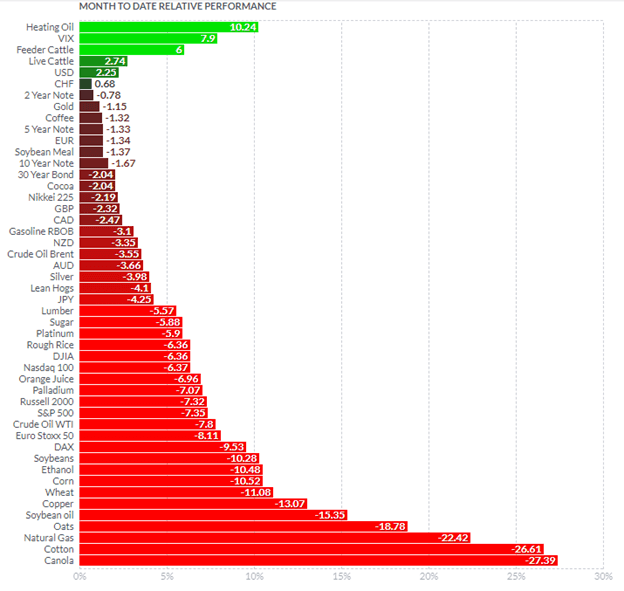

Jerome Powell took to the Hill this week and reiterated his “hike till it falls.” “It” can mean inflation without recession or inflation with recession. Either way, inflation will fall. Most prognosticators now believe that the Fed will provoke recession in pursuit of its objective. Some contend that we have already entered recession, citing the negative GDP print for the first quarter and the Atlanta Fed GDPNow tracker hugging the zero line. Even commodities (ground zero) have gotten into the act, with oil prices falling 14% from recent highs alongside an 11% drawdown in the GSCI commodity index overall. “Dr. Copper,” so named for its economic forecasting ability, has dropped 26% from its closing highs, falling nearly 20% in June alone. In fact, note the totality of the recession scenario sell-off in June based upon various futures contracts listed below (source: finviz):

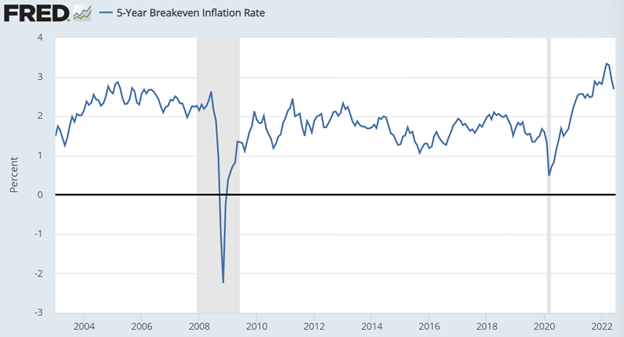

Ouch! Rarely have I seen such uniform declines. Clearly, the markets have aligned, and in doing so may bring about the disinflation the Fed seeks. In fact, the 5-year breakeven inflation rate forecast has fallen from 3.6% in March to 2.7% today. This remains well above the Fed’s 2% target but not wildly above its historical range:

In sum, inflation factors have improved, but only because the markets have decided that the Fed will break inflation with recession.

What If ?

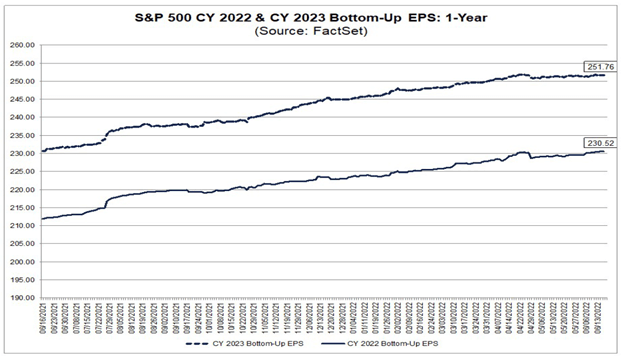

For stock market investors, recessions only matter to the degree that they impair corporate earnings. It is the drawdown in earnings they must quantify, not the uptick in unemployment. In the most recent COVID recession, corporate earnings fell 14% from peak to trough. The damage during the Great Financial Crisis was much greater when earnings fell 45%. During the Dot Com bust, earnings fell 23%. Since WWII, there have been 12 recessions. At the median, earnings fell 13%. Interestingly, the two Fed-induced recessions of 1980 and 1982, designed to break inflation, only saw earnings drawdowns of 3% and 13%, respectively. This suggests that well telegraphed recessions provide companies more opportunity to prepare. With prognosticators loudly chortling that recession will soon befall, surely no one will be caught by surprise. To wit, even with the recession telegraphing, analysts have remained optimistic about corporate earnings growth potential. Consider the stubborn earnings estimate curves below:

Halfway through 2022, analysts expect S&P 500 earnings per share of $230.52. Discounting 2022 earnings per share by the median 13% drawdown seen in recessions produces an earnings estimate of $200.55 for 2023. At the current trailing P/E of 17x, that equates to a price estimate for the S&P 500 of roughly 3400, accounting for an additional 10% decline from current levels.

What if ?

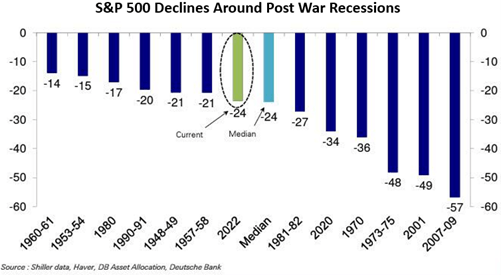

Combining the analysts’ earnings confidence with the average earnings drawdown of the two Fed manufactured recessions from the 1980s leads to a more optimistic scenario. An 8% earnings drawdown, multiplied by our 17x trailing P/E results in an S&P 500 value of 3600 or 5% below Thursday’s levels. If that’s the case, then the market has already discounted the recession. Compare our current condition with the market declines associated with the last 12 recessions:

Absent a crisis scenario, garden variety recessions tend to be readily recoverable for investors. Remember, in any given year the market corrects (-10% or more) at least once. Doubling that level hurts, but it’s survivable. With financial, household, and corporate debt levels reasonable as a percentage of GDP, we do not appear vulnerable to systematic collapse, a far greater earnings threat than recession. With the valuation correction largely completed in our view, the market now needs to price projected earnings. The optimistic analysts see earnings of $252 for 2023. The pessimistic prognosticators see earnings of $185 for 2023. That places the mid-point near $220. At 17x trailing, that marks the S&P 500 at 3700, precisely where opened this week.

Have a great Sunday!