The Full Story:

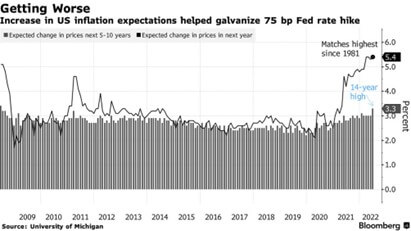

On Wednesday, the US Federal Reserve got into the oil business. Those of you that have not traded in your combustion vehicles for electric vehicles have no doubt noticed record gasoline prices at the pump. This time last year, US drivers paid $3 a gallon for unleaded fuel. This year, US drivers are paying $5 a gallon, for an “inflation” of 67%! Americans view inflation primarily in gasoline terms, and outsized movements at the pump tend to drive inflation expectations even higher. Note the correlated change in consumer inflation expectations below:

Not uncoincidentally, President Biden’s approval rating has dropped as the price of gasoline has risen. President Biden’s approval rating has fallen from 54% this time last year to 39% today, amounting to approval “deflation” of 28%. Given that no other price signal holds as much weight in consumer consciousness as the price of gasoline, it follows that no other price signal holds as much political weight as the price of gasoline either. This puts tremendous pressure on the White House. Not uncoincidentally, President Biden called Fed Chair Powell in recently to impress upon him that high gas prices have highly negative political consequences for ALL elected and appointed officials. In other words, saving their jobs requires saving consumers gas money. In response, the Fed increased its rate hike in June to .75% from the .50% broadcast. Sir, yes sir!

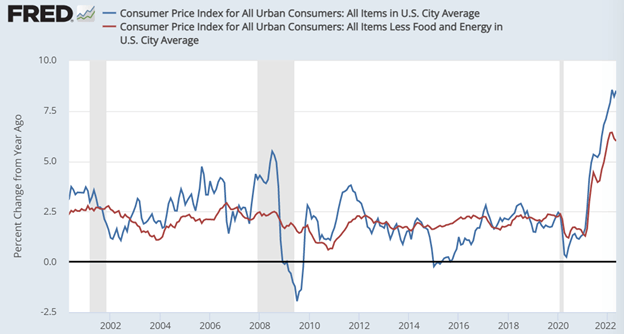

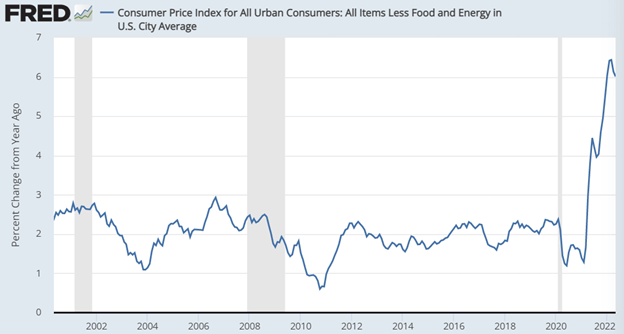

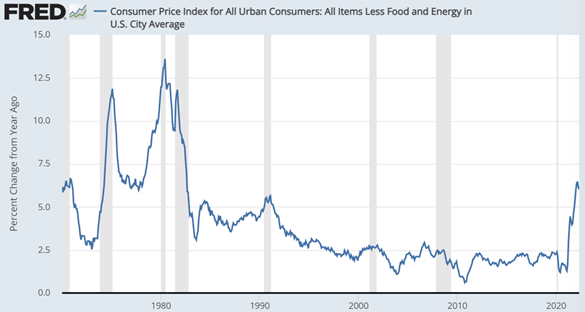

Traditionally, the Federal Reserve has omitted commodities like food and energy from its inflation gauges when setting policy. This reduces the volatility within the readings, which reduces volatility within the policy. Note the volatility difference between the Consumer Price Index and the Consumer Price Index ex-food and energy over the last 20 years:

Additionally, the Fed has little influence over the production of oil or the harvesting of wheat. They can influence commodity demand through rate policy, but not supply. Nonetheless, given heightened political stakes and heightened consumer inflation expectations, the Fed has migrated its attention away from traditional “core” inflation to non-traditional “headline” inflation. In our judgment, this is a policy mistake.

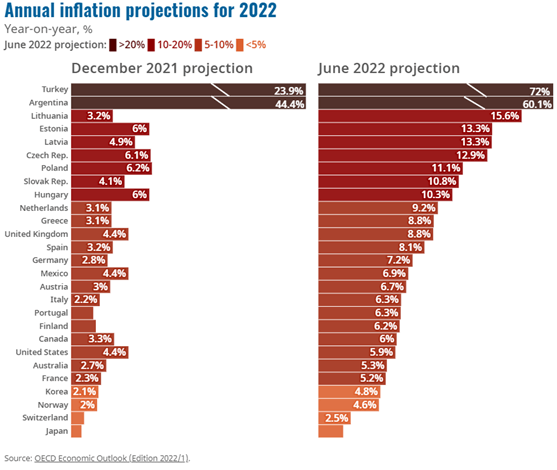

In their June economic outlook, the OECD attributed half of this year’s global inflation rate to Russia’s war with Ukraine. Note the pre-war and post-war divergences below:

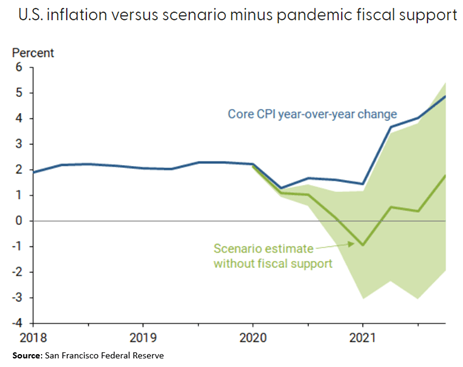

Clearly, Russian aggression has had a tremendous inflationary impact according to the OECD. But before Russia stoked inflation by attacking Ukraine, Congress stoked inflation by attacking COVID. In fact, the San Francisco Federal Reserve recently released a report attributing 3% of last year’s 5% core inflation rate to COVID fiscal stimulus as approved by Congress. Without these measures, the Fed itself projects that inflation levels today would approximate their 2% target level:

Therefore, according to the Federal Reserve and the OECD, outsized US fiscal spending and Russian aggression are the two major instigators of inflation. While Russia remains at war, COVID fiscal profligacy ended with the failure of Biden’s Build Back Better bill. Without it, fiscal spending has normalized back to pre-COVID levels, thereby removing fiscal inflationary pressure. Let’s revisit the CPI inflation chart from above, isolating only the “core” reading:

Note that since March, core CPI has fallen .43% to 6%. This amounts to a 7% inflation reduction in 2 months! And traditionally when inflation spikes quickly, it falls just as quickly:

Because higher prices reduce goods and services affordability, they also destroy demand, often culminating in economic recession (as noted by the grey bars above). This process has already begun in 2022 as recent economic reports on retail sales, housing and regional industrial activity have collapsed under the weight of higher price levels. Therefore, the economy has naturally begun adjusting price levels. However, given their new commodity price obsession, the Fed failed to notice. Well, not everyone.

Esther George of the Kansas City Fed voted against Chairman Powell’s .75% hike, stating “With high inflation and a tight economy, the case for continuing to remove policy accommodation is clear-cut. However, the speed with which we adjust the policy rate is important.” Translation: Fed policy decisions have lagging impacts, and since core inflation has begun descending as the economy has slowed, the pace of tightening should slow as well. Right on, Esther!

Unfortunately, with oil and food supplies disrupted, only a significant reduction in economic demand can bring down headline prices. Therefore, absent a mea culpa from Putin, Powell must drive the global economy into a recession to claim his prize. He has the power to do it, and that’s why markets plumbed fresh lows by week’s end.

From here until the end of June, we have three major contemplations. First, Powell will address Congress on June 23rd to hopefully clarify his “core” to “headline” policy flop. Second, the Fed will release May inflation data on June 30th which will largely inform its July policy decision. Third, investors like us must now recalibrate corporate earnings estimates in light of the Fed’s pro-recession stance. So much for the summer doldrums!

Have a great weekend… and Happy Father’s Day!