The Full Story:

On Wednesday,

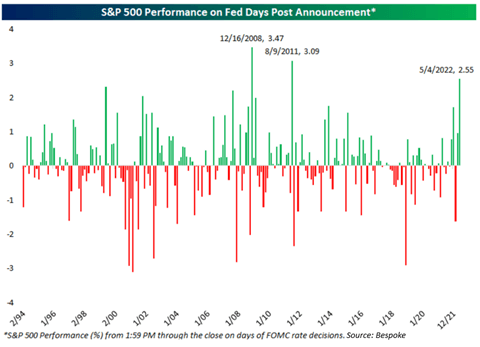

Federal Reserve Chairman Jerome Powell ignited one of the strongest post-announcement market rallies on record, despite hiking the Fed Fund’s rate .5%, committing to two more .5% hikes at upcoming meetings and laying out his plan to begin shrinking the Fed’s balance sheet by $47.5 billion per month starting in June. We have not seen a monetary squeeze of this magnitude since the early 1980s! So why rally?? The indices advanced because what matters to markets isn’t reality but the spread between reality and expectations. As we wrote last week, expectations had grown so historically despondent that less bad news could feel like good news. While the reality of the Fed’s war against inflation (and therefore against the economy) certainly wasn’t good news, the market expected .25% more in upcoming rate hikes than the Fed projected. This less bad news lit the powder keg of pessimism, exploding the S&P 500 2.55% higher in the last 2 hours of trading. This was the largest post-announcement rally we have seen in over a decade as chronicled below:

Powell also suggested that he believed inflation could be leveled without leveling the economy. Well, that’s also good news. If it’s true.

On Thursday,

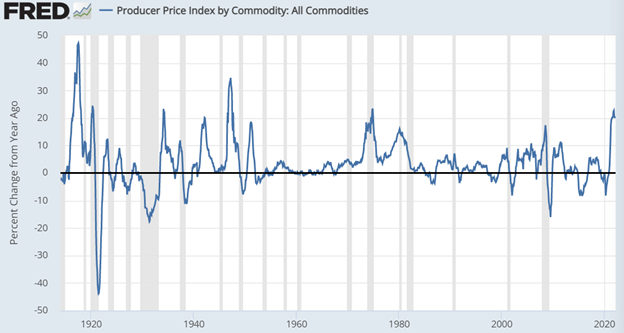

investors awoke to a surge higher in energy prices that cascaded into sharply higher interest rates, a sharply higher US dollar, and sharply lower stock valuations. While Powell reassured markets on Wednesday that the Fed could reduce inflation without recession, signs of persistent inflation on Thursday undermined this view. Take a long term look below at the path of commodity prices within the Producer Price Index:

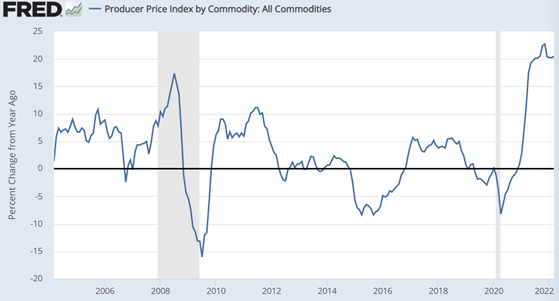

Clearly, we have seen commodity prices spike before. Oil embargoes, shortages or speculative fervor typically account for the surge. However, this go-round, COVID policy overstimulation paired with production shortages have broadened the participation beyond just oil. Historically, higher prices invigorate more commodity production, leading to swift reversals in commodity prices. Unfortunately, global politics has interrupted current supply expansion given restrictions on energy production and supply disruptions due to COVID, China, Russia, etc. Zooming in on the chart above, we can begin to see unusual “stickiness” for commodity prices at these levels:

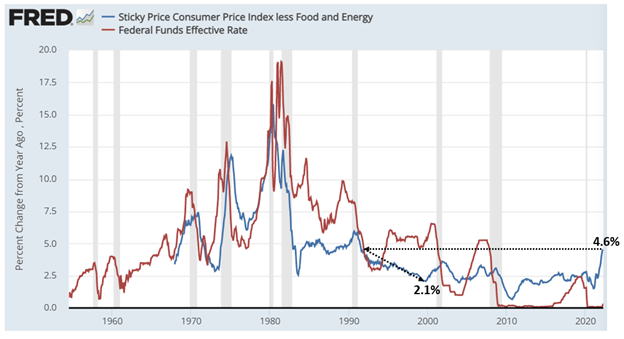

The Fed also tracks a broader measure of “sticky inflation” that incorporates CPI components that tend to vacillate less. These include rent, education, medical care services, trash collection fees, public transport, etc. Moves higher in this index cause more Fed concern as they do not reverse as quickly. Currently, the Fed’s core “sticky inflation” index reads 4.6%. The last time this measure read 4.6% was in 1991. It took 8 years for inflation to fall to the Fed’s desired 2% rate beneath a relatively high Fed funds rate. This occurred without a recession and concurrent with a raging bull market. Most other descents happened more quickly but were accompanied by recessions as seen below:

Powell may believe he can reprise the 1990’s and that inflation will naturally abate as rate hikes cool demand and high commodity prices stimulate supplies, but the evidence will need to grow more convincing to break the market out of this volatile, sideways range…and may require more patience than today’s ADHD investors are accustomed to.

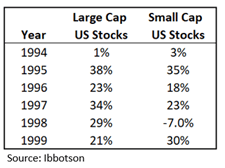

Extra Credit. For those who have faith that the Fed can reprise the late 1990s and are bold enough to dream… here were the results last go-round:

Not a prediction… but also, not fiction.

Have a great Sunday!