The Full Story:

Markets reacted violently after Fed Chair Jerome Powell signaled an accelerating pace of tapering on Tuesday. A more aggressive Fed, warranted or not, causes multiple concerns. Faster tapering implies faster rate hikes, and not only do higher rates slow economic growth but the Fed also tends to over-tighten once they begin. While Omicron took the blame for this week’s sell off, it’s the reappraisal of the Fed policy path that rightly deserves the blame.

What the Fed Fears

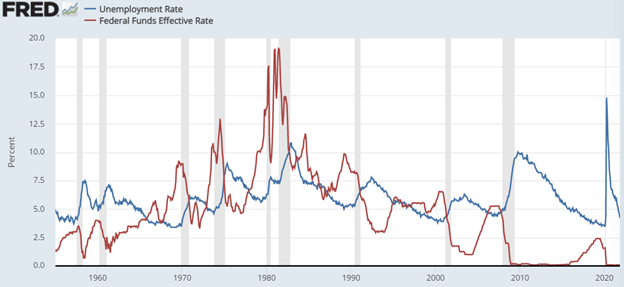

Friday morning, the Bureau of Labor Statistics reported a 4.2% unemployment rate for the US economy. In September, the Fed forecasted a 4.8% unemployment rate by year-end. The Fed therefore under projected significantly… with one more month to go! This rapid decline toward “full employment” has the Fed on edge. For perspective on the 4.2% rate, the US economy reached an unemployment rate low of 4.4% in 2007, prior to the Great Recession. Prior to the Great Lockdown in 2020, the US economy reached an unemployment rate low of 3.5%. In other words, we typically see unemployment rates this low at the END of an economic cycle, not at the beginning. Furthermore, we have NEVER seen rates anywhere near zero with an unemployment rate at this level:

This makes things tricky for the Fed. At previous 4.2% unemployment rates (20 occurrences), the Fed Funds rate averaged 3.5%. Also in September, the Fed projected a bottom in the unemployment rate near 3.5% for this economic cycle. At previous 3.5% unemployment rates (11 occurrences), the Fed Funds rate averaged 6.2%. In modern central banking, gradually lower unemployment levels meant gradually higher interest rate policy levels. In the heavily distorted stimulus-fueled post-COVID economy of today, unemployment levels have fallen too fast for the Fed to adapt.

What the Market Fears

While rate hikes seem warranted at such low unemployment levels, a debate will soon rage around the “neutral” level. Rates at the neutral level support economic growth without inciting above-target inflation… i.e., monetary nirvana. Unfortunately, arriving at monetary nirvana often requires trial and error. Most recently, the Fed removed three excessive rate hikes in 2019 to forestall recession. In retrospect, a Fed Funds rate of 2.25% seemed too tight, while a Fed Funds rate of 1.5% seemed just right, or “neutral.” Should 1.5% remain the “neutral” rate for this cycle, the Fed only has five .25% rate hikes in its quiver. Deploying any more than that might reprise the over-tightening, yield-curve inverting, recessionary invitation they issued in 2019. Concerningly, the Fed has forecasted a 2.5% “neutral” rate for this cycle, a full 1% above the market’s estimate. This has left investors rightly unnerved as the pace of job gains has spooked the Fed and risks rushing its decision-making. With even more fiscal stimulus on the way to add further distortion, the risk of a monetary policy mistake impairing growth has grown.

The Good News

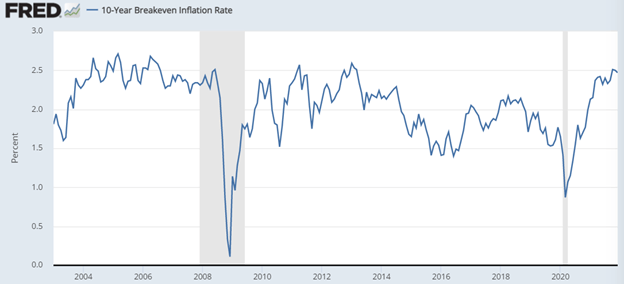

Fortunately, longer-term inflation expectations gauges express confidence that the Fed will figure this out. Let’s first examine the 10-year breakeven inflation rate. The chart below chronicles inflation expectations over the next 10 years by deducting the 10-year Treasury Inflation-Protected Security yield from the 10-year Treasury Bond yield. Currently, the yield spread suggests 2.47% inflation over the next 10 years, a bit higher than the Fed’s long term 2% projection but well within historical bounds over the last twenty years:

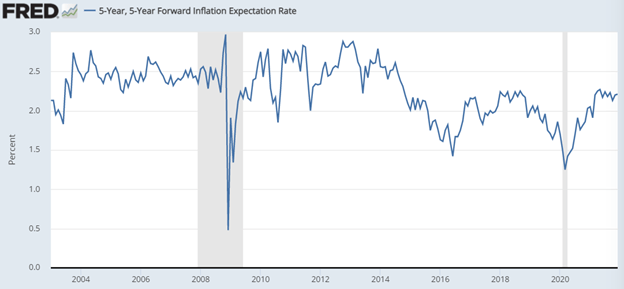

We can filter this 10-year view down further to adjust for stimulus-induced, near-term inflation distortions. The 5-Year, 5-Year Forward Inflation Expectations Rate measures 5-year inflation expectations beginning 5 years from now. Based upon this measure, 5-year inflation expectations 5 years from now fall to 2.2%, even more within historic bounds:

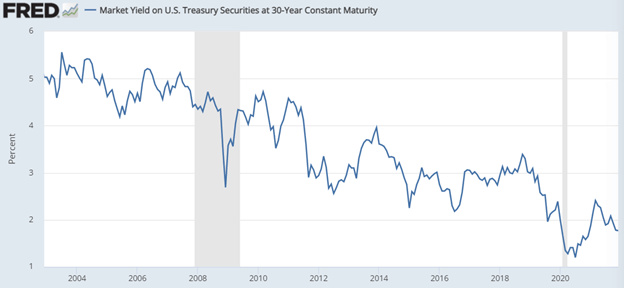

Lastly, since interest rates price off inflation expectations, if market participants truly believed we had years of inflation ahead, long-term interest rates would be rising. Instead, they are falling. Currently, the 30-year Treasury yields 1.77%:

Based upon these market-based gauges, inflation is not a longer-term concern. So, while the Fed’s near-term policy mix has fallen into question, the markets’ assessments of the Fed’s longer-term policy effectiveness have not.

Have a great Sunday!

David S. Waddell

CEO, Chief Investment Strategist