The Full Story:

Prior to the pandemic, the US economy employed 152,523,000 people. Today, the US economy employs 147,553,000 people. Yet US GDP stands $1.2 trillion higher. This increase in “output per worker” of 5% is great news, but we cannot grow our economy on productivity gains alone. We need to grow our labor force as well. Confoundingly, the US labor force (those with jobs and those seeking jobs) has shrunk by 3 million people since the pandemic began. The explanations for this exodus include mothers staying home to oversee virtual classrooms, those who simply fear exposure to the virus, increased retirements for those opting to permanently extend their COVID furloughs, systematic mismatches between modern work requirements and obsolete skill levels, and work disincentives derived from massive and continuous “workforce assistance” programs from the government. Each of these factors likely plays a proportional role, and the decrease in COVID case rates alone could improve participation rates. But the right question to ask is can the US economy grow without a growing workforce?

Turning Japanese

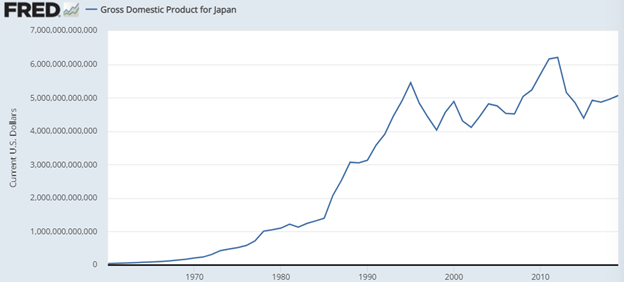

The United States Federal Reserve thinks a lot about Japan. The Japanese economy expanded at an astonishing pace between 1960 and 1995. Since then, the Japanese economy hasn’t budged. Japanese GDP hit $5.5 trillion in 1995 and ended 2019 at $5 trillion. That’s a 9% decline over 24 years!

When you inflation-adjust these numbers, the picture slightly improves with GDP rising 2% over the period, but that just means that Japan has experienced price DEFLATION over the last 24 years. Admittedly, Japanese monetary and fiscal authorities have made many mistakes over the last 24 years, but the source of their pain isn’t policy blunders, its simply demographics.

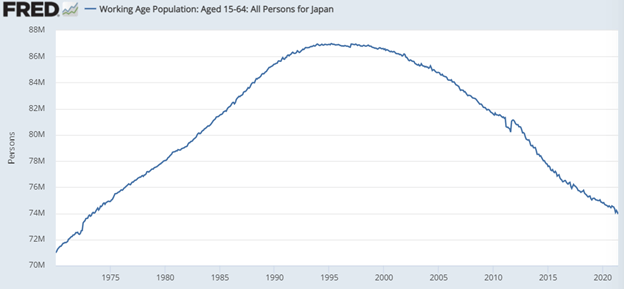

The Japanese working age population peaked at 87 million workers in March of 1995. As of June 2021, this number registered 74 million, amounting to a 15% decline in total labor force.

While productivity in Japan has increased, the greying of its population along with its aversion to immigration and its male centric work culture has led to a workforce decline that is too large to overcome. For Japan’s economy to grow, it needs its workforce to grow.

What about US?

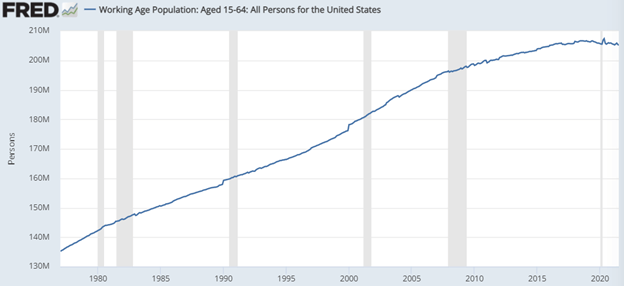

The US working age population in March of 1995 was 167 million. In June of 2021, this number hit 205 million or 23% higher in contrast to Japan’s 15% decline. Advantage, USA. Unfortunately, the US working age population has stalled out recently, making fewer potential employees available for the US economy:

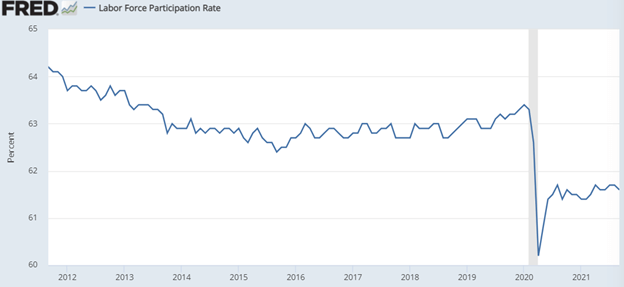

This plateau in workers creates a drag on GDP. Increasing workforce participation rate could present an offset, but unfortunately that number has declined as well:

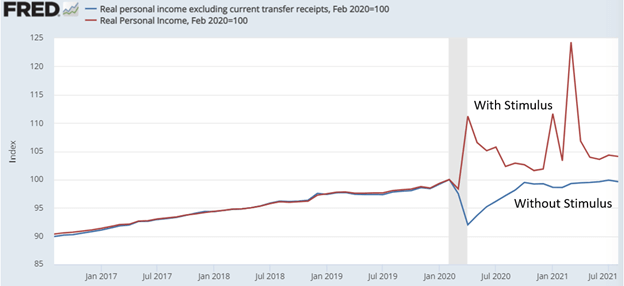

We had an encouraging uptick in participation prior to COVID as the political policy array and the strength of the economy drove unemployment rates low and wages up progressively. Since then, however, participation has disappointed. This makes sense as households have actually increased their wealth and incomes in the COVID economy thanks to government relief spending and despite labor dislocations. Consider the impact on incomes alone (indexed to February 2020), with and without government benefits (note: annualized incomes are calculated as the last month’s income, times 12):

Overall, incomes are 5% higher today than pre-pandemic, thanks to stimulus. Overall household wealth has increased an astounding 30% over the same time-period, thanks to stimulus. People work because they have to, but when incomes and balance sheets surge, some two income households become one income households and those contemplating retirement simply retire. Unfortunately, higher wealth and higher incomes create more demand amidst fewer workers.

This explains the record 11 million job openings for the 7.6 million unemployed (those participating in the labor force but identified as unemployed). The resulting tension should result in higher wages and in fact, wages are rising at their fastest pace in decades. In summary, we currently have a shrinking labor force and low labor participation rates alongside robust household finances with robust American appetites. This creates shortages and upward pressure on wages that can only resolve with increased labor supply or well above average labor productivity.

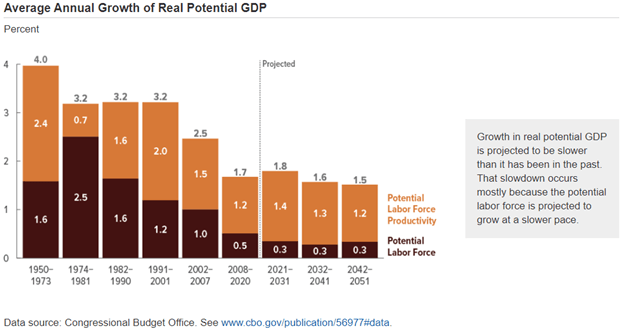

Unfortunately, the long-term labor outlook remains challenged. The Congressional Budget Office projects the labor force will continue to expand, but at a much lower rate than before:

The boomer boost in the 80s has burst, and more modern families have lower reproduction rates. Women in the United States currently deliver 1.6 babies, on average. For the population to remain constant they need to deliver 2.1, on average. Therefore, of the .3% annual growth projected in the labor force, all of it comes from net immigration. Without a dramatic shift in reproduction rates, participation rates, or immigration rates, labor force growth will continue to flounder and frustrate employers.

I’m Kilroy!

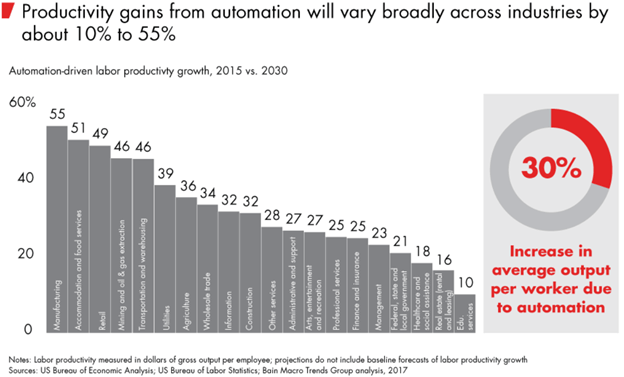

Malthusians wrongly assume that technology cannot overcome scarcity projections. We disagree. The rapid development of dexterous robotics (search YouTube), and artificial intelligence applications (“Alexa, grow productivity!”) will increase the supply of virtual workers to offset a lesser supply of physical workers. In a study by Bain, automation should enhance worker productivity by 30% by 2030:

If that’s true, then automation alone will add 1.8% annualized to GDP. The good news? Maybe the robots don’t kill us in the future after all, but instead they save our GDP growth rates!

For employers, this is my plea for you to take today’s profit margins and invest boldly in automation. The labor shortages currently plaguing your business are not going away. Greater labor productivity is the only antidote, reached through more efficient processes and more output per employee. COVID taught us many important lessons, including the value of virtualization and digitization. Don’t unlearn it!

Have a great Sunday!

David S. Waddell

CEO, Chief Investment Strategist