The Full Story:

The markets ended September on cue. With a thud. We projected that the market’s Pavlovian tendencies and September’s dismal historic track record would combine and initiate a “reason to sell” scavenger hunt. That happened. The hunters didn’t have to hunt hard, with Fed taper talk and DC legislative theatrics throwing monetary and fiscal gears in reverse, China’s capitalism crackdown, and pernicious inflation readings. In all, the S&P 500 shed nearly 5% on the month to finish the quarter flat. Encouragingly, analysts remain optimistic about the near-term growth path for corporate earnings. Third quarter earnings growth estimates for the S&P 500 have risen from 24% at the start of the quarter to 28% as of the close, while full-year estimates clock in at 43% growth vs. 36%. However, these same analysts have begun trimming earnings estimates for 2022 over concerns of rising input costs and lower profit margins. With the economy reopening and more economic supply on approach, what’s driving these longer duration inflation fears?

Fed Inflation Sedation

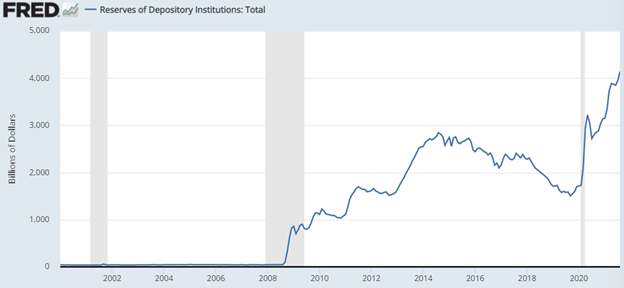

On September 22nd, the Federal Reserve released its Summary of Economic Projections. They increased their 2021 “core” inflation projection from 3.0% to 3.7% and their 2022 projection from 2.1% to 2.3%. These moves may not look like much, but they amount to upward adjustments of 20% and 10%, respectively. They also increased their policy rate forecast from .6% to 1% in 2023. This suggests four rate hikes by year-end 2023 and signals at least one for next year. Additionally, the Fed has solidly signaled their intent to begin trimming their asset purchase program by $15 billion a month, ending quantitative easing by mid-2022 in advance of any rate hikes. Frankly, none of this seems unreasonable to us. The marketplace is oversupplied with capital anyway as seen in the bank excess reserves held at the Fed (i.e., idle lending capacity):

Additionally, tapering isn’t tightening, it’s just incrementally-less quantitative easing. The Fed will thus remain stimulative, just less so for the next 9 months. Given their above-trend inflation and GDP forecasts, this downshift in monetary policy seems appropriate. Rates should drift higher amidst this subtle shift (which is the point) but shouldn’t unglue in a disorderly fashion. This rate of withdrawal should not spook investors, which was evidenced by the 1% advance in the S&P 500 the day of the release. In the Fed’s eyes, commodity shortages will abate, as some have already. The semiconductor issues will abate as more production capacity tools are unlocked. And labor shortages should abate as COVID emergency assistance programs wind down. Or will they?

Congressional Inflation Stimulation

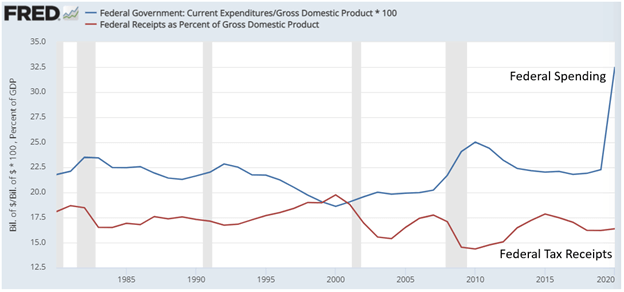

While the Fed has shifted its efforts to forestalling inflation, Congress seems intent on aggravating it. Historically, the federal government has spent approximately 20% of GDP while taxing 17% of GDP. This leaves an average deficit of 3%, which was OK when inflation averaged 3%. Last year, the government spent 32.5% of GDP while collecting 16.3% as seen in the chart below:

This equates to a deficit of 16%. We supported this historic stimulus needed to offset the historic economic damage wrought by the coronavirus pandemic. However, now, as the pandemic recedes, rather than tightening the spending spigot, Congress has proposed spending another $5 trillion over and above its normalized budget. Tax increases will offset $2 trillion or so of this with deficit financing offsetting the other $3 trillion that is over and above our normalized deficit.

Normally, I would quietly root for more fiscal stimulus because more spending equals more profits and higher stock prices. However, the timing and mix of incentives in these bills seems politically expedient but economically and financially misguided. Countercyclical fiscal policy argues for big spending programs when the economic engine needs fuel, not when it’s flooded! Our current economy, growing 3x above trend, has an historic labor and supply shortage. This has led to jarring increases in general price levels across the economy. For instance, I recently dined at a restaurant that tacked a 20% “labor surcharge” onto my bill. I had the privilege of paying more, for slower service… thanks 2021.

In fact, as of the latest JOLTS survey, America has a record 11 million job openings available to the 8.3 million people currently seeking employment. Clearing the inflationary bottlenecks across the economy after such sizable demand stimulus requires time and digestion. Instead, Congress has proposed even more stimulus, equating to 23% of total GDP ($5 trillion/$22.5 trillion). Yes, I know that this spending, theoretically, gets neatly metered out over 10 years, but even still, that pace adds .5% in additional GDP to our annualized potential growth rate of around 2%. Adding this much additional GDP at a time when labor is short, supply is constrained, and inflation is rising just invites more inflation. Confoundingly, in addition to increasing economic demand, these spending proposals may actually decrease economic supply.

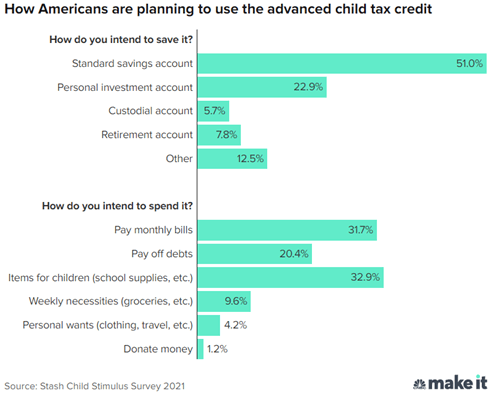

Expansions of benefits, tax credits, and support programs reduce labor incentives. If you make $100K working and I offer you $100K not to work, which would you choose? This isn’t a moral statement, it’s an economic one. Within the contemplated legislation, Congress will allocate $1.1 trillion in new spending over 10 years through childcare tax credits. In theory, this money should go to subsidizing childcare expenses to free up more labor supply to offset labor shortages and ease up supply constraints. In practice, it does not:

Without restrictions, this money just supplements income. Once received, parents decide how to allocate. It can go to childcare expenses, but it can also go to paying off debt, buying Bitcoin, or watching Netflix. Once installed, it will undoubtedly become a permanent subsidy. But more government spending does not mean more jobs; in fact, it may even mean less. According to a 2016 study by the St. Louis Federal Reserve reviewing 120 years of data:

Following a policy change that begins when the unemployment rate is high, if government spending increases by 1 percent of GDP, then total employment increases by between 0 percent and 0.15 percent. Following a policy change that begins when the unemployment rate is low, the same government spending increase causes total employment to change by –0.4 percent and 0 percent. Although the effect is larger during times of high unemployment, even then, the employment effect of government spending is low.

In other words, as the research shows, with unemployment levels already low, more government spending may actually reduce current employment levels. Negative change or no change in labor participation rates while ramping up economic demand through benefit expansions sounds nothing but inflationary to me, and it sounds that way to forward-looking profit prognosticators as well.

Fortunately, we expect that the weight of the above arguments, and many others, will lead to a significant scale down in the proposed legislation. In fact, the finalized package may need to be a half to a third of the current proposal to pass. That alone will begin reinflating analysts’ 2022 earnings forecasts as well as investor confidence as we close out 2021.

Have a great Sunday!

David S. Waddell

CEO, Chief Investment Strategist