The Full Story:

I am an optimist. I believe that prosperity always finds a way. Over the past year, I have missed out on media opportunities because the networks and organizations preferred pessimistic viewpoints. When asked for my view on COVID, I acknowledged the dire health consequences, but also emphasized the economic renewal and robust expansion that would surely follow, and likely blow away expectations.

Early in the recovery, we have seen hundreds of economic reports that beat expectations, we have seen business originations at historic highs, and we have seen surging productivity gains. Even still, the nearly completed parade of first-quarter earnings reports blew past even my rosiest expectations. Join me in celebrating these numbers:

– At the end of March, analysts expected Q1 2021 S&P 500 earnings to rise 23.8%. The blended earnings growth rate of the 425 companies that have reported actual results stands today near 50%. That is the highest level of blended earnings growth since the Great Recession completely wiped out corporate earnings in 2009.

– Of the companies that have reported earnings, arecord 86% have beaten expectations.

– Of the companies that have beaten expectations, they have beaten them by a margin of nearly 25%… also a record.

– Companies have reported record net profit margins of 12.5% for the quarter.

– Away from the large-cap S&P 500 index, earnings grew 86% across the mid-cap S&P 400 index and 126% across the small-cap S&P 600 index.

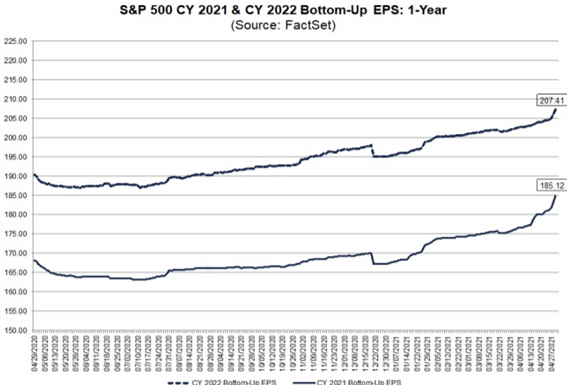

– Analysts now expect earnings to grow 32% for the full year compared with expectations of 26% growth at the end of March. Additionally, EPS (earnings per share) estimates for next year continue to rise as well:

– Currently, the estimate for 2022 S&P 500 earnings approximates $210 per share. Should the current P/E of 22 remain, that would produce an index level of 4620, compared with 4,230 today, for a projected gain of 10%.

While it’s hard for me to admit, even my level of optimism appears pessimistic in light of such results. The creativity, adaptability, and resilience of corporate America continue to astound, and the earnings power of this market absolutely justifies its continued achievement of all-time highs.

The Fight for $15!

On Friday, the US Bureau of Labor Statistics reported that our economy added 266,000 jobs in April versus the 1,000,000 expected, and that the US unemployment rate rose .1% to 6.1%.

Why the historic miss? Did the economy slow? Should we worry about a follow-on recession? Not exactly.

The Fed’s GDP Now predictor foresees 11% GDP growth for the second quarter. Furthermore, according to the most recent JOLTS (Job Opening and Labor Turnover Survey), there were 7.3 million jobs available in February for the 9.8 million people unemployed. With so many jobs available, why have so many Americans opted out of the labor force or remained unemployed? Some cite the closure of schools and the lack of daycare, which are contributors, but the aggregate level of unemployment benefits provides a powerful employment disincentive for millions of Americans.

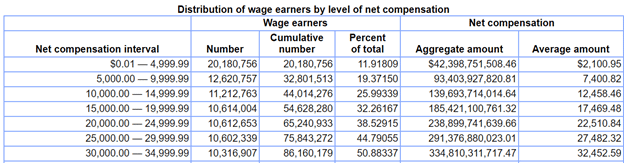

Let’s do the math. States pay an average weekly unemployment benefit of $325. In exchange for mandated lockdowns, the federal government currently supplements state benefits with an additional $300, equaling $625 a week in average replacement wages. $625 amounts to an annualized wage level of $32,500. This may not sound like much until you review the following statistics from the Social Security Administration:

Nearly 50% of all wage earners in the United States earn less than $30,000 a year. Therefore, millions of rational economic actors may be choosing unemployment wages of $32,500 over employment wages of $30,000. This likely explains our labor shortage and the persistence of the unemployment rate around 6%.

Fortunately for understaffed employers, the $300 federal subsidy will expire on September 6th. This will drop the parity threshold back down to $16,900 annualized and should replenish the labor force. However, a group of 38 congressmen led by Senators Wyden and Senator Beyer did lobby Biden to make unemployment benefits permanent within his recently proposed infrastructure bill.

Interestingly, dividing $32,500 by the 2073 work hours in a year produces an hourly rate of $15. Making unemployment benefits permanent at $15 an hour would effectively back door a $15 an hour minimum wage.

Throughout history, government price-control attempts have largely failed, and most often incited inflation. As the reopening of the economy increases the demand for labor, while extended unemployment benefits decrease the supply of labor, expect wage inflation to follow. On point, wages in April rose .7%, or 8.5% annualized.

Happy Mother’s Day!