The Full Story

The U.S. dollar is fighting an uphill battle at the moment. Early in the pandemic, the dollar’s appreciation was consistent with its historical role as the world’s safe-haven currency. But an unprecedented degree of fiscal support, monetary support, and an uneven recovery are likely to impart a depreciation bias to the dollar in all but the most intense cyclical scenarios.

Fiscally, the CARES Act provided $2.2 trillion at the outset of the pandemic followed by a $900 billion follow-up bill at year-end with some smaller provisions in between. These massive packages in addition to typical spending, pushed the 2020 federal budget deficit to 15.3%, which was the largest deficit as a share of the economy since the World war II-ravaged 1945. And this week, Congressional Democrats advanced another $1.9 trillion relief bill to be passed through the budget reconciliation process.

Monetarily, the Federal Reserve’s commitment to make up for undershooting their past inflation target (2%) as well as returning the U.S. to full employment has them on a continued path of low interest rates and asset purchases. The Federal Open Market Committee (FOMC) of the Federal Reserve surprise no one last week when they kept the fed funds rate unchanged at zero. The FOMC also announced that they will maintain securities purchases—currently at $120 billion per month, and with no changes to the composition of its purchases—until “substantial further progress” toward its inflation and employment goals has been met. Key language in the FOMC statement included that the “pace of the recovery in economic activity and employment has moderated in recent months, with weakness concentrated in the sectors most adversely affected by the pandemic.” It was a slight downgrade from the prior meeting’s statement, which noted that the economy “continued to recover.”

Regarding their two main initiatives, inflation may very well be the most important issue to get right in 2021 and beyond, so I will explore it more in depth below. Employment has softened the past two months as the U.S. reimposed restrictions to battle the peak of the coronavirus pandemic. The January jobs report, which released on Friday, showed just 49,000 in net jobs additions and an unemployment rate of 6.3%.

So how has the dollar performed? Over the trailing year, the U.S. Dollar Index (DXY) is down almost 8% when compared to a basket of foreign currencies.

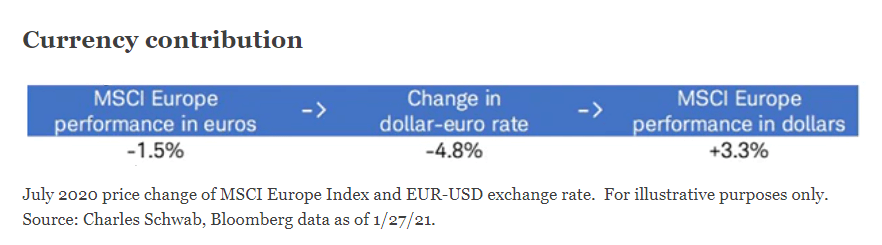

If you hold international stocks denominated in another currency, you not only experience the change in the stock price in that currency but also the change in the value of the currency when measured against the dollar. When the dollar falls, it provides a tailwind for US-based investors in international stocks. Using an example during this recent period, in July 2020, European stocks fell -1.5%, as measured in euros. However, the U.S. dollar fell -4.8% versus the euro, which resulted in European stocks posting a gain of +3.3%, measured in U.S. dollars.

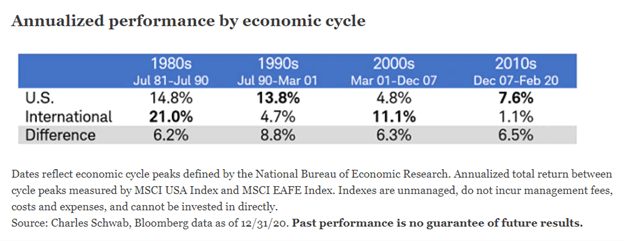

If the dollar continues to work downwards, it could act as a persistent tailwind to the performance of international stocks as measured in U.S. dollars. That is the pattern that we have seen in the past. It tends to move in long-term cycles. After international stocks outperformed in the ’80s, the 1990 recession led to a shift to U.S. outperformance. The 2001 tech bubble recession initiated a switch back to international outperformance, followed by the 2008 Great Recession which flipped the switch again to U.S. outperformance. Now, the coronavirus pandemic recession may once again signal the start of a new cycle of international stock outperformance.

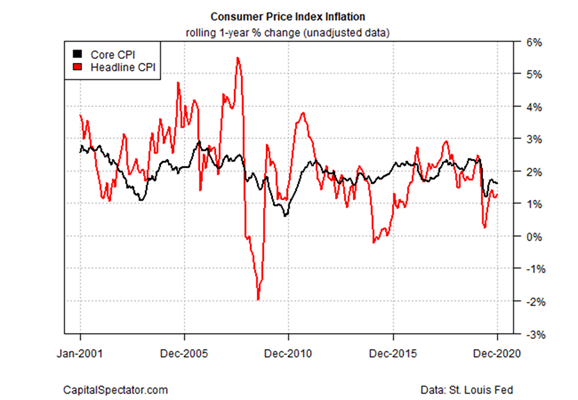

One concerning side effect that can emerge during periods of dollar weakness is rising inflation. We continue to watch inflation measures because of its impact on bond yields and Federal Reserve policy. But so far, the hard data offers minimal support for an uptick in inflation. The one-year trend for consumer prices (headline and core) is still well below pre-pandemic levels. Core CPI increased 1.6% for the year through December, well below the 2%+ trend that prevailed before the coronavirus shock. The comparable measures for the Eurozone and Japan were close to zero at 0.2% and -0.5%. Over the same period, the headline CPI inflation rate in China was 0.2% even as their economy grew.

Dr. Ed Yardeni theorizes that four deflationary forces (the 4 Ds) have been and will keep a lid on inflation. They are Detente (globalization), Disruption (technological disruption), Demography (aging populations), and Debt (too much propping up zombie companies). Inflation may rebound and stabilize in 2021, but at this stage it does not appear likely that pricing pressure will materially rise for any length of time above the pre-pandemic trend.

Have a great Sunday!

Timothy W. Ellis, Jr., CPA/PFS, CFP®

Senior Investment Strategist, Wealth Strategist