The Full Story:

Truly successful investors seem to lack an amygdala. The amygdala quickly processes information and issues a fight or flight command for our motor functions to follow. Paradoxically, the most successful trades of all time typically originate in the most traumatic moments of all time. A week or so ago, CNBC held a follow-up interview with Bill Ackman of Pershing Square. The first interview aired on March 18th. I remember watching it somewhat awestruck as this historically levelheaded market master warned “hell is coming”. This seemed wildly uncharacteristic for someone who gorges on risk for a living. My amygdala instinctively activated and called upon my motor functions to “sell everything”. I was not alone, as the market dropped nearly 1,000 points during his dirge as millions of amygdalas fired simultaneously. While the cascading sell orders swamped the market, Ackman’s firm profited massively from a short-term short (betting stocks will fall fast) while they added longer-term risk (betting stocks will rise slowly). As Ackman clearly knows, fear creates opportunities, and his interview exacerbated fears that he simultaneously capitalized on. Recognizing Ackman’s con and the pure panic in the market, we overrode our amygdalas’ “sell everything” signal by closing out our short positions days later. Ackman’s recent follow-up appearance, after plenty of rebuke, masterfully explained away his trading profits born of the fear he exacerbated. But this episode acts as a powerful reminder for investors about the relationship between fear and profits. Simply put… the more fear, the more profits. After a rapid 50% run off the March lows, how much fear, and therefore how much more near-term profit, remains?

The Investors Intelligence Survey

Created in 1963, this weekly survey scans investment newsletters and ascribes bullish, bearish, or neutral ratings to each. Aggregating this data provides insight into market sentiment among professional investors. As of the most recent survey, 57% of investment advisors read bullish on stocks while 17% read bearish on stocks (the remainder are neutral). This translates into a bull/bear ratio of 3.35 compared with average readings below 2. Ratios over 3 correspond with high levels of overall bullishness and therefore low levels of fear. This may make professional investor amygdalas happy, but it also may suggest lower near-term profit potential for us should retail investors share their optimism.

The American Association of Individual Investors

Created in 1987, this weekly survey asks non-professional investors whether they expect the market over the next six months to rise, fall, or flatline. The typical survey respondent tends to be male in their mid-60s with $1 million in portfolio assets. Since inception, respondents on average have been 39% bullish and 31% bearish (the remainder are neutral). As of the most recent survey, 23% of non-professional investors are bullish on stocks, while 48% are bearish for a bull/bear ratio of .48, well below the long-term average of 1.25. This signals household amygdalas in distress, with a highly divergent view from the professionals… but does this pessimism suggest higher near-term profits?

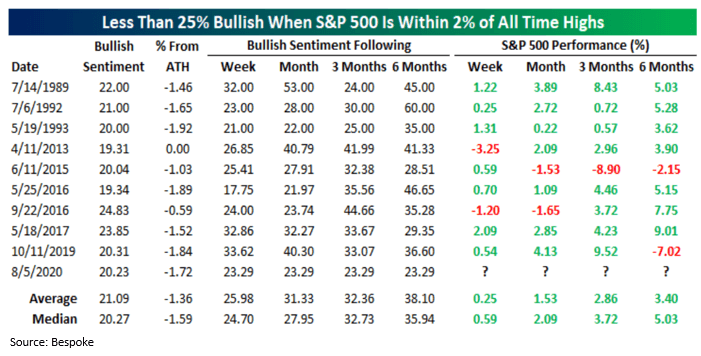

Bespoke Investment Management analyzed previous periods of bullish AAII readings below 25% with markets within striking distance of all-time highs. Here is what they found:

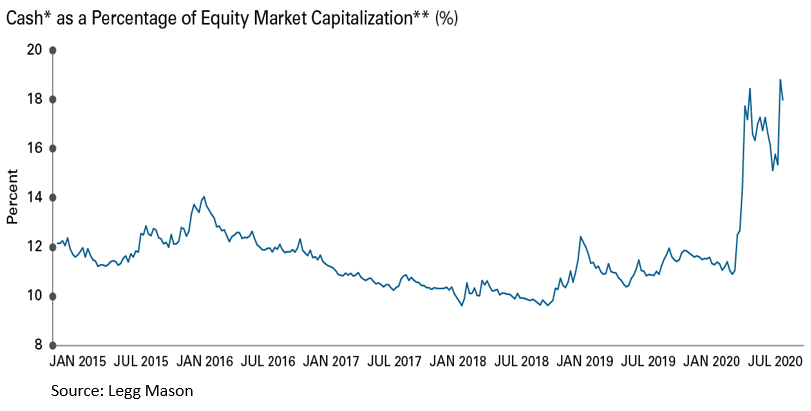

As seen above, there have been 9 periods since the AAII survey’s inception that match the current environment. Six months later, markets traded higher 78% of the time with a median return of 5%. While this appears promising, conversion of bearish sentiment into bullish sentiment only propels markets higher if it converts cash into stocks. For our contrarian sentiment thesis to work, we need a large starting cash reservoir. Fortunately, according to the chart from below, the reservoir runneth over.

Approval of a vaccine would undoubtedly lift main street spirits and retail investor optimism. When both non-professional and professional investors become fearless again we will become fearful. Until then, this rally still has legs.