The Full Story:

Thematic investors wagering on investment outperformance primarily choose between contrarian and momentum-based strategies. Momentum fans chase positive returns expecting them to continue, while contrarian fans chase negative returns expecting them to reverse. The success of either strategy hinges on capturing the imagination of investors followed by steady streams of capital. Timing the shift between these two styles is one of the great challenges for professional investors. Most choose a style and stay in their lane, opting for periodic outperformance and underperformance rather than risk accumulating timing errors. However, in extreme environments, persistence of style outperformance can lead to “towel throwing” transformations where proven contrarians become desperate momentarians. This leads to overcrowding, “this time is different” rhetoric, and the abandonment of fundamental assessments. We saw this in the late 1960s with the Nifty 50, in the late 1990s with the Dot Coms, and in the late 2010s with the FANGS+. These environments create significant marketplace distortions but also significant opportunities for the observant.

The Momentum Cash Out

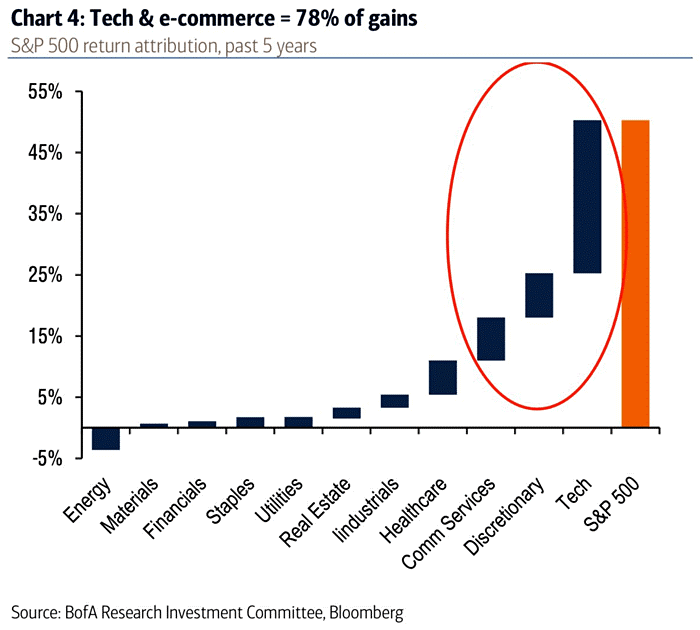

Facebook, Amazon, Apple, Netflix, Google and Microsoft have accumulated nearly $6 trillion in market capitalization (valuation) since 2013. They alone now account for 25% of the S&P 500, the largest concentration of capitalization ever seen within the index’s history. In fact, on their own Microsoft and Apple account for 45% of the valuation within the technology sector. Google, FaceBook and Netflix account for 66% of the communications sector, and Amazon alone accounts for 50% the consumer discretionary sector (up from less than 10% in 2013). Had you invested in ONLY these stocks back in 2013, you would have gained 481% through last Friday vs. a mere 76% by investing in the other 494 companies within the S&P 500. In fact, over the last 5 years, 78% of the returns for the S&P 500 came from advances in the tech, communications and consumer discretionary sectors as represented in the chart below :

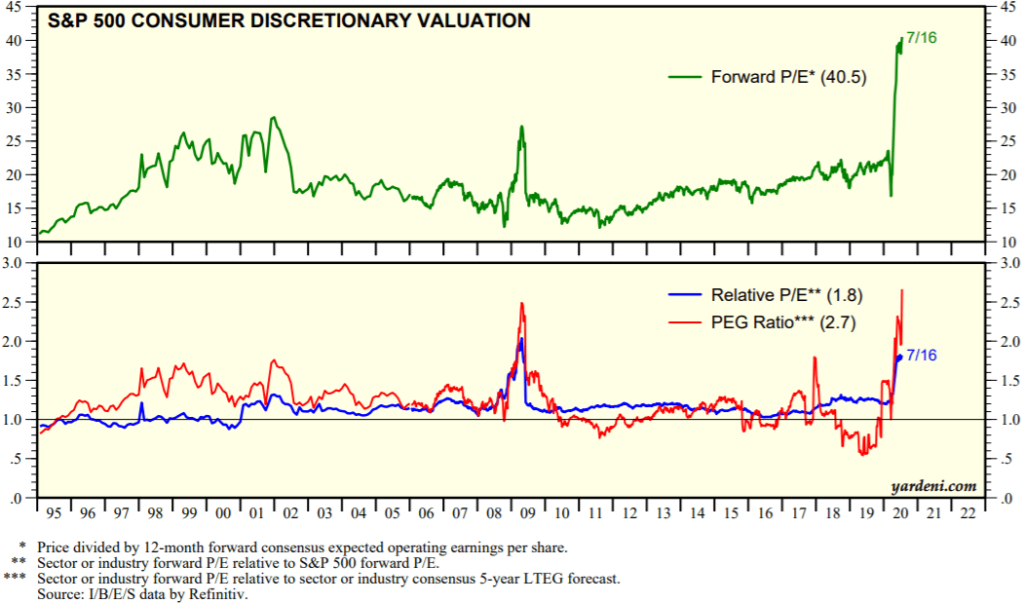

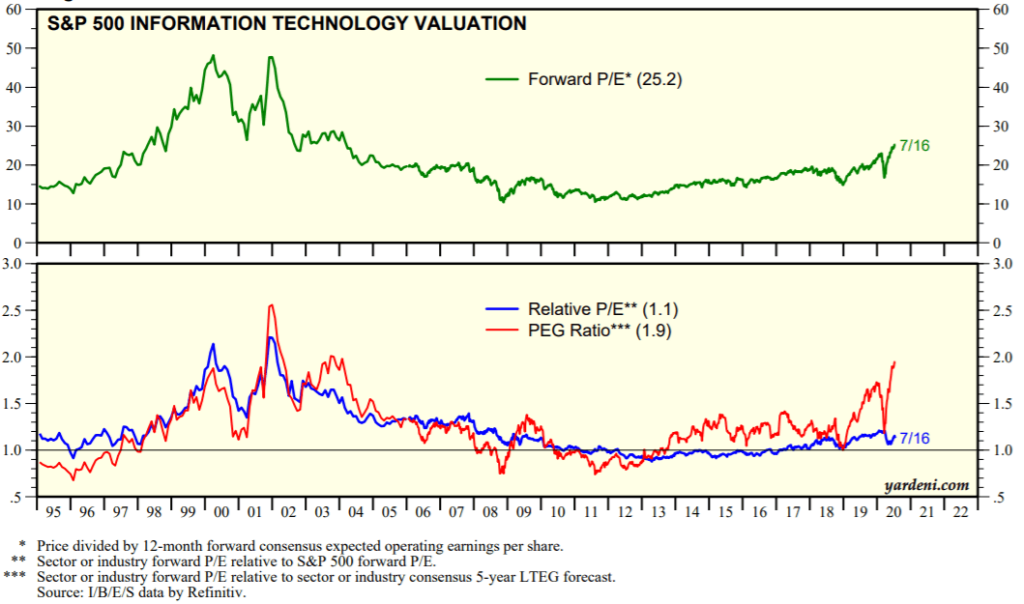

With these stocks playing such a large role now in the S&P 500 index, any description of the index itself must get filtered for proper assessment. For instance, the S&P 500 seems overvalued at 23x forward earnings, but stripping out these behemoths trading at 41x lowers the overall P/E multiple for the index to a more pedestrian 19x. Many FANG+ propagandists will cite the exemplary earnings growth rates of these companies as justification for their lofty valuations. To verify, we must then adjust the P/E ratio to a PEG ratio (P/E divided by the growth rate) to determine how much investors are paying for growth. Here are more comprehensive valuation assessments for the sectors in question:

For the consumer discretionary sector (also known as Amazon), 40.5x represents a record P/E while 2.7 represents a record PEG as well.

The 25x P/E for the information technology sector sits well below the extremes reached in the late 1990s but when you convert this number to a PEG to incorporate expected earnings growth, it sits just above the 1999 high.

The Contrarian Cash-In

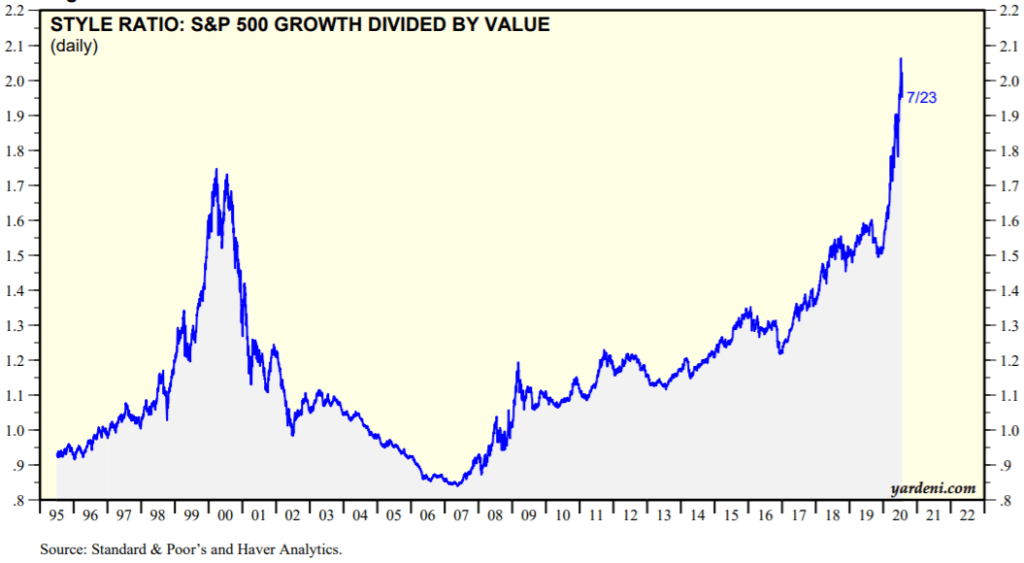

Never before have contrarian investors felt so much pain. S&P 500 growth/momentum names have outperformed S&P 500 value/contrarian names by an historic degree, leading storied value investors to either quit the craft or smuggle growth names into their portfolios for survival.

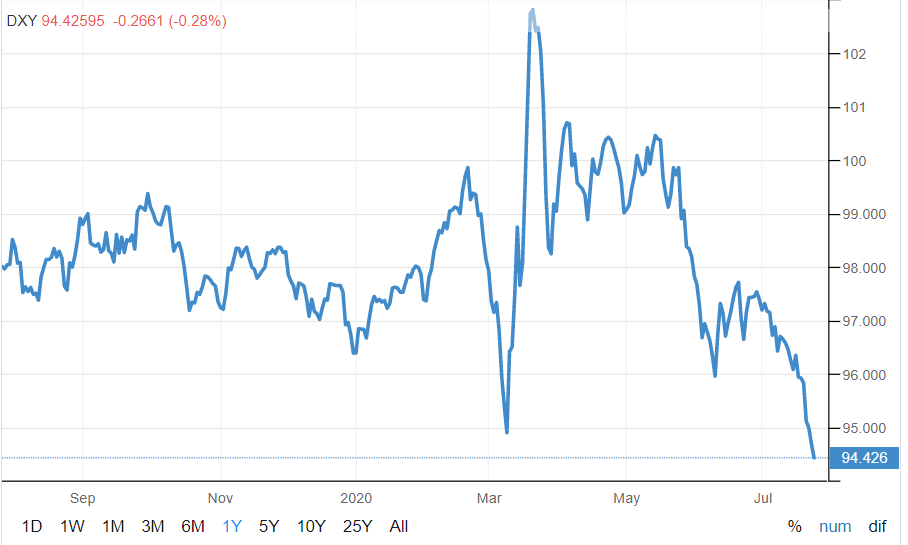

But it’s time to offer these contrarians relief as we believe COVID has pushed these momentum names too far. We haven’t even addressed fanboy stocks like Tesla, but the list of hot and beloved “newest economy” names reads long and may even include Pets.com at this point. Anyway, should the next 5 years play out like the early 2000s, which we think it will, investors will be better served by learning to love today’s unloved. Between 2000 and 2005, investors who stuck with S&P 500 growth stocks lost 31% of their capital while those who held S&P 500 value stocks made 13%, those who held emerging market stocks made 24%, those who held small cap stocks made 38%, and those who held the most reviled small cap value stocks made 121%. What created this investable rotation? Excessive valuations in the momentum names, a recession and a recovery, and a persistent decline in the US dollar. With the first two conditions obviously met, let’s check in on the dollar’s recent action:

Source: Yardeni

After the brief COVID “flight to quality” spike, the US dollar has collapsed. With these three conditions met, let’s test our rotation theory. Over the past three months, S&P growth stocks gained 20%, emerging market stocks gained 22%, and small cap stocks gained 23%. These divergences seem small, but it’s still early as these style changes tend to last for years. For those of you still chasing momentum, you might consider changing your style.