The Full Story:

The Tally of Terribles

The Coronavirus attack and our isolation defense have taken their toll. To date within the US, 245,000 confirmed cases have resulted in 6,000 deaths. The White House projects that total COVID related deaths within the US could climb as high as 240,000. Absent antivirals and vaccines, our national stay at home response has shut down large sectors of our economy leading to 10 million unemployment filings within the past three weeks. Analysts estimate that the US economy could shrink 30% annualized in the second quarter for a loss of $1.4 trillion in US GDP, the largest quarterly drawdown since the Great Depression. People we know by name have contracted this disease. Some we know have died.

The Empire Strikes Back

Today, millions of small businesses around the country will apply for payroll subsidies authorized by Congress. Millions more will utilize SBA disaster loans, apply for tax credits and defer payroll taxes. Larger firms, states and municipalities will queue up for a $4 trillion loan pool backstopped by the Treasury and administered by the Fed. Overall, Congress has authorized $2.2 trillion in fiscal assistance to compliment the “unlimited” monetary assistance and zero interest rate policy provided by the Federal Reserve. Washington views these measures as “mitigation” and has already begun negotiations on another $2 trillion “stimulus” package to rebuild our nation’s infrastructure. Our national deficits and debt will bloat to levels unseen since WWII, but we are financing them at record low interest rates.

Pessimism Pays

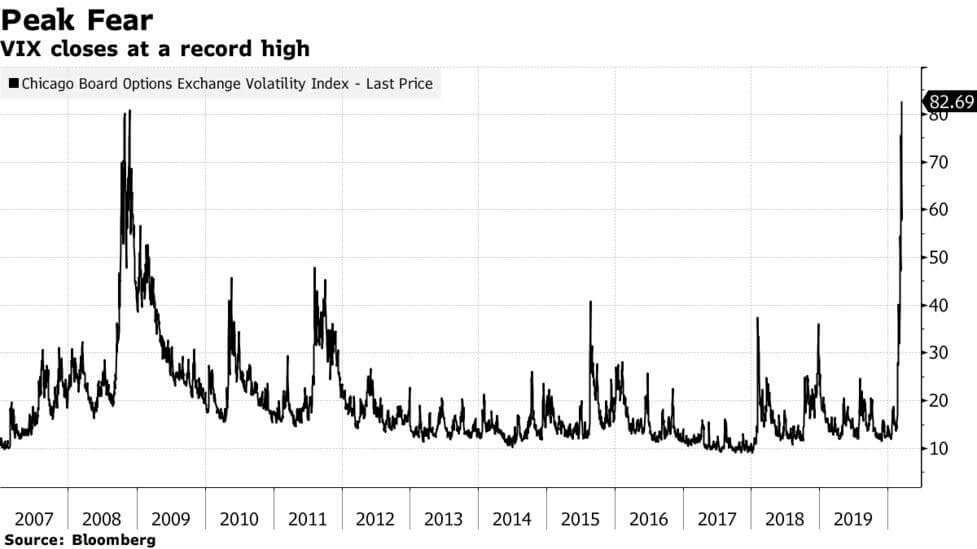

Markets move through distinct phases in and around crisis and recessions. Rapid recognition of the oncoming health and economic crisis led to the fastest deleveraging in history. The VIX index, which measures options volatility, provides the best visual to communicate the speed and scale of the panicked liquidations:

By this measure, COVID 2020 generated more fear faster than the Global Financial Crisis of 2008. During that period the VIX peaked on October 24th while the Dow Jones Industrial Average sank to 8,088. Three months later the Dow closed at 8,077. Three months after that the Dow closed at 8,076. Three months after that the Dow closed at 9,093. Three months after that the Dow closed at 9,972. In the current COVID crisis, the VIX peaked on March 16th while the Dow sank to 20,116. We opened today at 21,413.

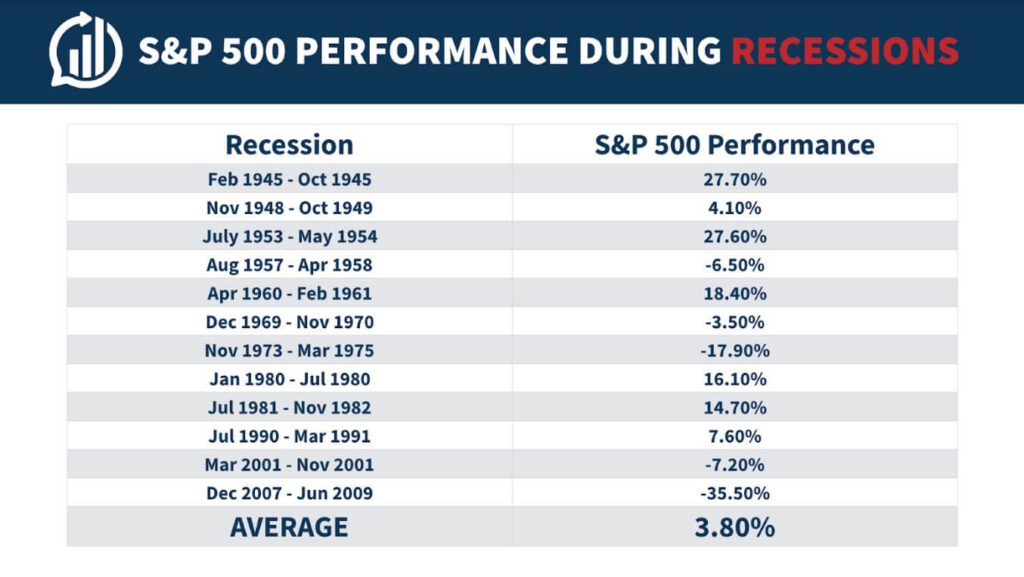

Once the panic phase passes, reality sets in, market volatility declines and fundamental debates begin. How bad will the recession be? How bad will earnings be? How many bonds will default? What shape will the recovery be? Will we recover? During periods of distress, projections hold negative biases. It’s human nature. Yet what drives markets higher is NOT whether reality is good or bad. What drives markets higher is whether reality is better than expectations. In fact, on average, stocks RISE during recessions:

Clearly, 2008/2009 added an outlier. I will assert that following the legitimate crisis in 2008, policy mistakes created an echo crisis in the first quarter of 2009 as the banks appeared insolvent. Had policy makers addressed these concerns adequately in the fourth quarter of 2008, we likely would not have plumbed new lows in the first quarter of 2009. Nonetheless, the data point remains that, on average, markets climb during recessions as reality exceeds lugubrious expectations.

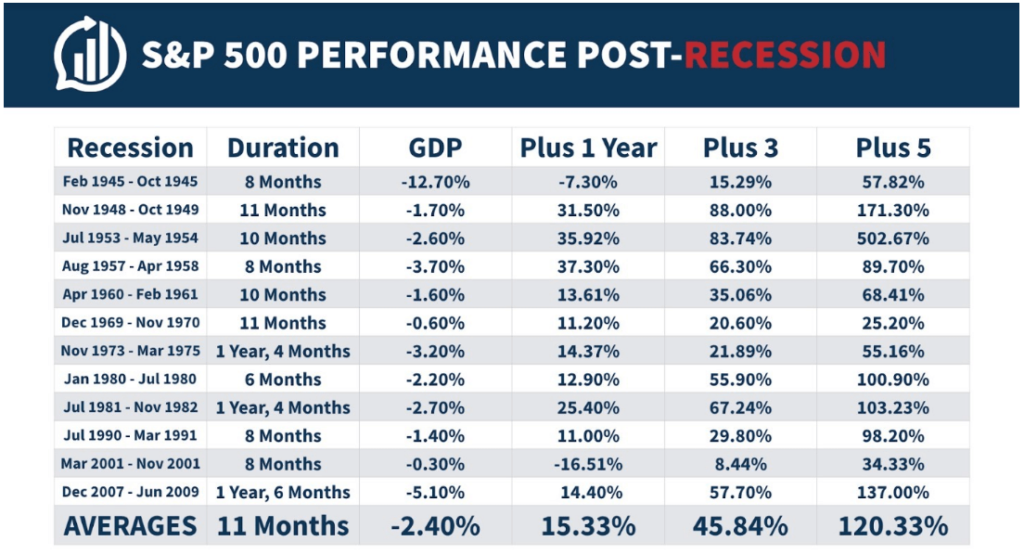

Just to extend the view here are the returns post-recession:

W&A Buys Probabilities:

In the summer of 2019, the combination of restrictive central bank policy and restrictive trade policy led us to hedge out 20% of our equity market exposure amid rising recession risks. The quick turnabout from the Fed in the fall moved us to reduce our hedged exposure by half, awaiting economic proof that the monetary easing from the Fed had boosted more than markets. Prior to the coronavirus outbreak, the economic evidence argued for removing our remaining hedge position as trade agreements began boosting real activity. Then the virus. As markets cascaded lower, our hedge position grew quickly in size. Recognizing the peak in the VIX, we halved our hedge position on March 20th. Recognizing the inception of recession, we fully eliminated our equity portfolio hedge within our models on April 1st.

Will the market spike lower from here? Perhaps. Bear markets often go through a bottoming process that includes retesting previous lows. Will the market go higher from here? Absolutely. This just depends on your timeframe. Referring to the charts above of the previous 12 recessions, markets rose 60% of the time during recession, rose 80% of the time one year after recession, and rose 100% of the time three years after recession. Remember, we invest in probabilities, not possibilities.