As I sat down to pen this week’s strategist, I became nearly paralyzed with possibilities. Rarely have I seen news cycles this boisterous with health, politics, sports, earnings, and economics all crowing for attention. At W&A, we pride ourselves on providing clarity to remove fear, so this week I will attempt to separate the news from the noise to help you prioritize what, and what not, to worry over.

The Noise

The Big Sell-Off:

The Dow Jones Industrial Average sold off 400 points to begin the week and 400 points to end the week. In between, the market rallied 300 points, making the net decline around 550 points. A number that large certainly draws attention, but remember that with the Dow at 29,000, a 550 point drawdown only equates to a 2% move. In fact, by the close of the week, the Dow sits a mere 3% below its January 17th closing high. This hardly amounts to a big sell-off. Furthermore, the Friday sell down was wildly predictable as traders often close out positions in periods of high uncertainty to avoid untradable weekend surprises.

Brexit:

As of today, Britain no longer resides within the EU. In a vote of confidence after some encouraging economic data, the British central bank left interest rates unchanged and the pound sterling rose nearly 1%. Much work remains as the EU and UK negotiate new trade terms, but for now, the future is history. The UK operated and enjoyed much success as a sovereign entity far longer than as an EU affiliate. Markets and investors prefer certainty. Structural clarity politically unlocks decisiveness economically. So… carry on.

Earnings:

With 200 of the S&P 500 earnings reports in, analysts now predict growth for the quarter. Microsoft, Apple, Intel, Amazon, and other large contributors blew past earnings estimates along with 73% of reporting companies. I threw this in the noise category because these numbers are backward-looking, and the positive opinion of Q4’s results already resides within the marketplace. Should the final tally prove positive, it would coincide with the belief that economic momentum accelerated into year-end. In other words, Q4 earnings are baked in the cake already… but they still taste good!

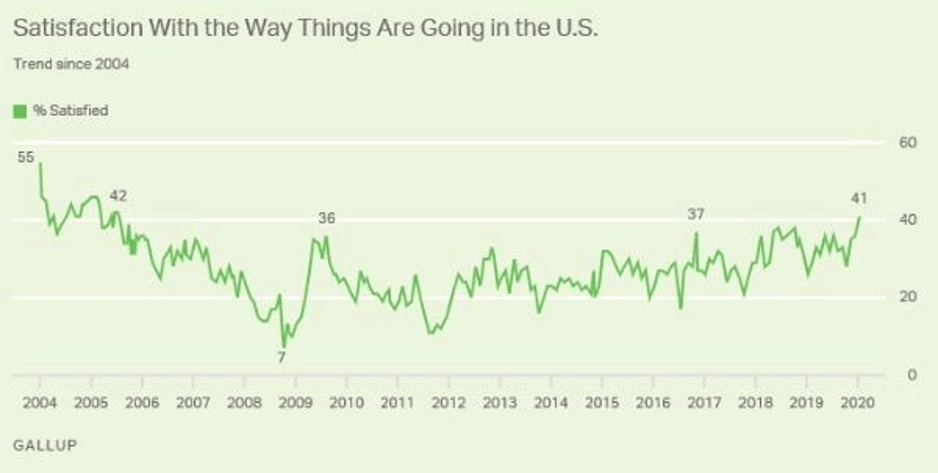

Impeachment:

No bribery, no fraud… no criminal impeachment. As to his political impeachment, Trump’s approval rating stands at the highest level of his presidency. His scores on the economy are even higher, and at the highest level overall since President Clinton. Not only is impeachment a non-issue for Trump, but it also appears to be strengthening his candidacy. Given all the Twitter tantrums out there, this chart will likely surprise you:

The News

US Economic Growth:

GDP in the United States grew 2.1% in the 4th quarter and 2.3% for the year. While 2.3% lags the 3% the White House may be targeting, it stands above our true potential economic growth rate that is closer to 2% (potential GDP equals the combination of our workforce growth rate and our productivity growth rate). Within the numbers, we saw a large contribution from trade (fewer imports vs. exports) and a surge in military spending, both very Trumpian. Investment spending and inventory drawdowns reflected residual trade policy uncertainty while the consumer retrenched somewhat but not at a concerning pace. Overall, 2019 proved successful despite tight monetary policy to begin the year and tight fiscal policy from trade negotiations. No signs within the report of an impending demise for this record-long economic expansion.

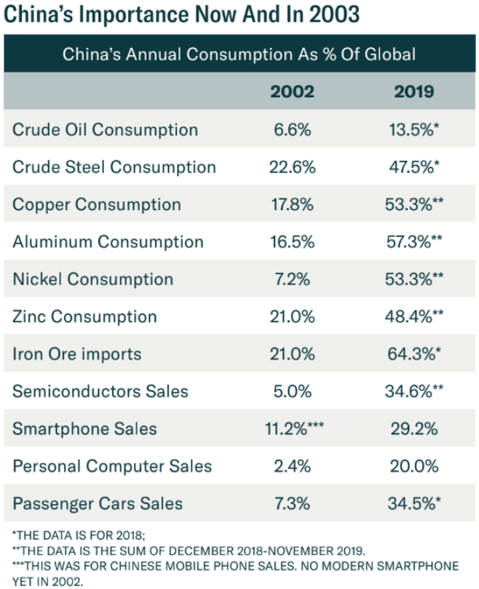

Coronavirus:

A three percent drawdown from recent highs is hardly newsworthy but the potential fallout from a worst-case scenario requires contemplation. Most importantly, it’s the Chinese economy that has the flu, and the Chinese economy matters far more today than it did in 2003. Consider these numbers:

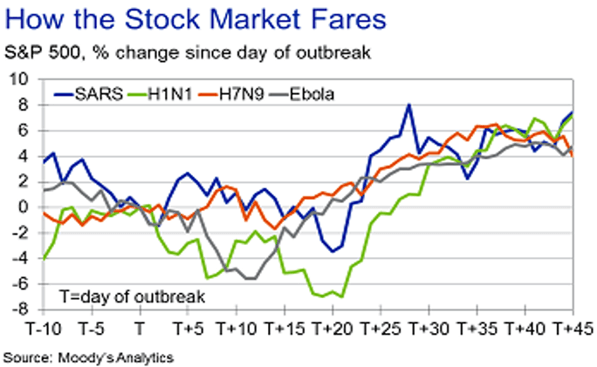

Overall, growth in the Chinese economy powers 35-40% of global GDP growth. Some fear if China catches a cold, the world will catch the flu. It’s possible, but still not probable. The IMF anticipated an acceleration in global GDP growth this year from 2.9% to 3.3% pre-coronavirus. To wipe out global economic growth, the coronavirus would have to subtract $3.6 trillion of economic activity. The SARS pandemic deducted $56 billion overall with 8,000 cases and 800 fatalities. Applying equivalency math, to get to $3.6 trillion, the coronavirus would need to infect over 2,500,000 people and cause more than 50,000 deaths. Using history as a guide, modern medicine, and containment methods should gain an advantage soon. I mentioned in the Yahoo finance interview that past pandemic panics lasted about 20 days. Here are some market results for substantiation:

Inflation:

The big indicator for 2020. In 2019, we watched the leading economic indicators like a hawk to assess recession probabilities arising from the Federal Reserve’s restrictive monetary stance. After cutting rates three times and printing $400 billion, the Fed has notably adopted a constructive monetary stance. As such, we have shifted our focus to inflation levels. The Fed reinforced its position this week that it deeply wants to see inflation rise and hold above 2% and will not restrict policy ever again until it does. We received data on the Fed’s preferred inflation gauge Friday. For December, core consumer inflation rose 1.6%, decidedly below 2%. In response, 10-year inflation expectations fell to a commensurate 1.6%, the yield on the 10-year Treasury fell to 1.5% and the US dollar fell nearly .5%. No current inflation plus the prospects of coronavirus deflation now have central banks considering MORE stimulus, not less. Fed Funds futures now price in an 84% chance of another rate cut in 2020. Forcefully stoking price inflation historically stokes asset inflation…meaning forcing prices higher will likely force markets higher as well.