The Full Story:

Despite concurrent lousy economic and earnings fundamentals, robust asset class returns last year forecasted robust fundamental gains for 2020. Fortunately, while the year has hardly begun, early economic releases have provided validation. As stated within a recent J.P. Morgan release, “The December global all-industry PMI (Purchasing Manager Index) came in positively at the end of the year reinforcing a view that activity will improve in the coming quarters. The all-industry activity PMI increased for the second month to an eight-month high. Improving trends in new order inflows, employment, and business sentiment also suggest that further headway should be made at the start of the new year. International trade remains the main drag on efforts to lift growth further, so any moves that reduce tensions and barriers on this front will be especially beneficial.”

Six days later, the US and China inked a Phase One trade deal which added additional psychological lift. 2020 economic renewal? It’s early but possible. Shifting to Q4 earnings, analysts expected yet another quarter of negative growth. Should they be proven correct, S&P 500 earnings will not have grown at all over the last year. However, early Q4 releases have amassed historically high revenue surprises. Given that revenues tie more closely to macroeconomic conditions, this could add further confirmation of economic acceleration. 2020 earnings renewal? It’s early, but possible. In fact, analysts now expect earnings growth of 9.5% for 2020 and 10.7% for 2021. Durable economic and earnings renewal with inflation low and interest rates anchored should push equity indices far higher into record-breaking territory. At least, that’s the consensus view.

The Bubble in Search of a Pin

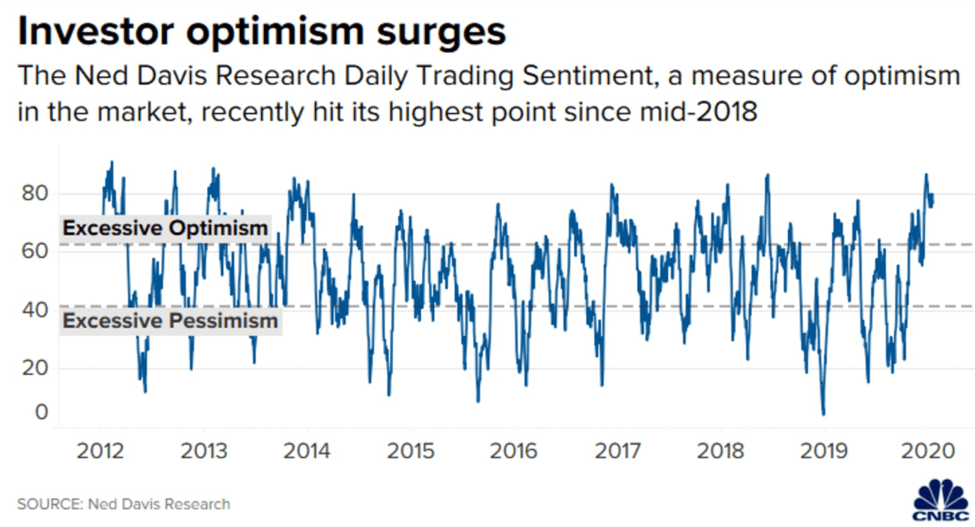

Quantitative easing from the Fed. A Phase One trade deal. Accelerating economic growth. Accelerating earnings growth. Discussions of additional tax cuts with Trump 2.0 the heavy favorite. A Super Bowl without the New England Patriots. What’s not to like? Basking in optimism, the S&P 500 hasn’t experienced a 1% pullback in over 70 trading days, the 6th longest streak in the last 20 years. The NASDAQ hasn’t had a 1% pullback in a record-breaking 16 weeks. Relative strength measures, moving average comparisons, breadth calculations and oscillator limits all sit at relative extremes. For visual confirmation, Ned Davis constructs a nice composite sentiment indicator included below:

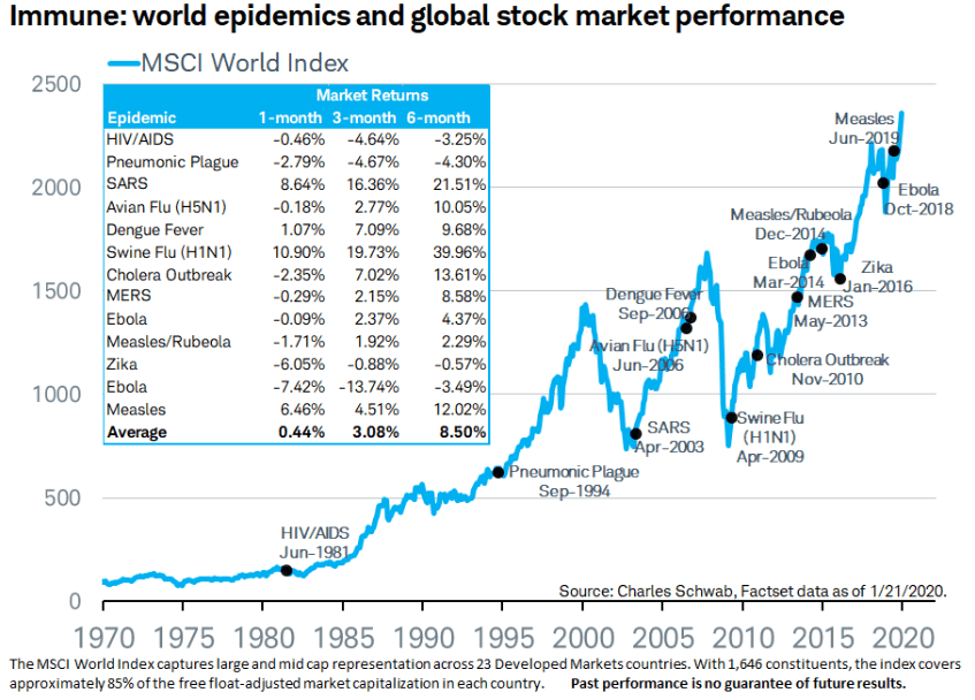

Per its 25-year history, when this indicator rises above 62.5, returns over the following year have averaged -7%, contrasting the +30% average returns logged when sentiment readings fall below 40. Clearly, when sentiment rises to this level, bullish consensus becomes vulnerable to a bearish counterpoint. While the threat of WWIII with Iran wasn’t enough to dissuade the bulls, the viral outbreak in China may be. While the coronavirus might instigate a natural sentiment correction, investors should maintain composure and take comfort in the longer-term market results following other pandemics: