The Full Story:

Why should investors own bonds?

– To be a shock absorber for your stock portfolio.

– To earn more interest than cash with current money market rates at close to 0%.

– To provide a source of income to fund withdrawals from your investment portfolio.

Not all bonds are created equal.

The headlines you see about bonds are usually referring to prices and yields of U.S. Treasury bonds, which are influenced mostly by Federal Reserve interest rate policy, inflation, and the status of the U.S. dollar as the world’s reserve currency.

U.S. Treasuries are just one small component of the global bond market.

The global bond market is three times larger than the global equity market. The U.S. accounts for only 39% of the global bond market, with Treasuries representing only 35% of the total U.S. bond market according to the latest Wikipedia data.

Diversity of investment choices in the U.S. bond market.

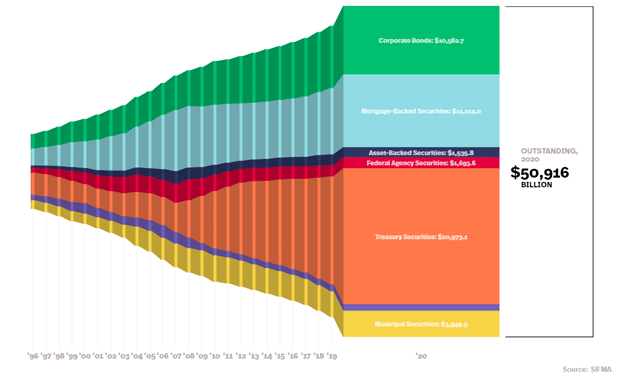

The Bloomberg Barclays U.S. Aggregate Bond Index (AGG) measures the average returns for the total U.S. investment grade bond market. In addition to U.S. Treasuries, which make up 39% of the AGG, Morningstar reports 26% of the AGG is in corporate bonds, 22% is in securitized bonds (think mortgages) and the remainder is municipal bonds and cash equivalents, with diversification across industries, credit ratings, and maturity. In addition to investment grade bonds represented in the AGG, non-investment grade bonds make up the remainder of the total outstanding U.S. bond market, which has grown significantly as shown in the SIFMA graph below.

Math matters a lot.

Two main factors influence bond returns – the price you pay for a bond and the yield you get on the bond. As market-based interest rates change for newly issued bonds, prices of existing bonds must adjust accordingly. The relationship is inverse. If interest rates go up, the price of your existing bond must go down for it to reflect current market interest rates.

Changes in bond returns can be more predictable than changes in stock returns based on one statistic.

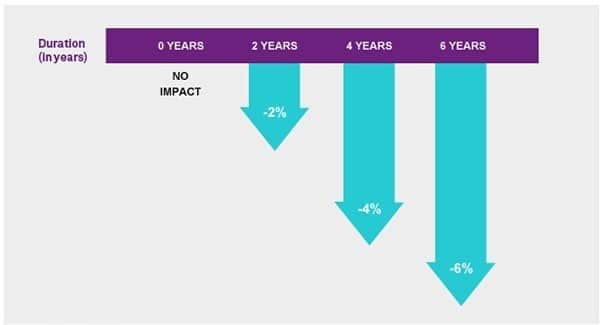

An important shorthand mathematical statistic, duration, can be used to predict the change in price of a bond given a change in interest rates. If one believes interest rates are trending up or down, a portfolio manager can adjust the duration of the portfolio to manage that risk.

Percentage Change in Bond Prices If Rates Spike Up 1%

The importance of active management in today’s bond markets.

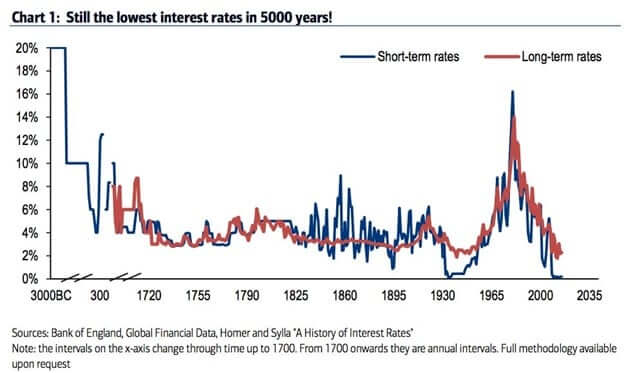

Managing duration is especially important now with interest rate spreads at historic lows. Bond managers with flexible investment policies can adjust duration to cushion against falling prices as interest rates rise. An interesting graph of the “History of Interest Rates” from the Bank of England shows current interest rates are the lowest in 5000 years.

How are the concepts above expressed by the W&A investment committee in our current bond portfolio?

– Five diversified bond mutual funds actively managed by leading experienced bond managers chosen by the W&A investment committee based on our own research and interviews with fund managers.

– Can cover global bond sectors with the flexibility to take advantage of changes in investment market opportunities and interest rate environments.

– Has an average duration of 3.17* years compared to 6.37 years for Bloomberg AGG

– Has a combined 12-month yield of 3.31% *

– Total return will also reflect bond prices that can fluctuate both up and down.

Managing the managers. Less interest rate risk and more credit risk in a low-interest rate environment.

This is the consensus opinion of the W&A investment committee as expressed in our current bond portfolio. In a low-interest rate environment, overall absolute levels of total returns to bonds are expected to be lower relative to long-term historical averages. To compensate for lower yields, we believe we can take on additional credit risk in a strong economic recovery. But to cushion against the downside risk of rising interest rates, we proactively keep our duration much lower than the overall bond market. We choose bond funds that complement each other to smooth out the ride. We continually monitor our bond manager outlooks as well as others on our watch list. Just this last week, I listened to six different webcasts from funds we own and funds on our watch list to hear their latest perspectives and updates to portfolios.

Conclusion: With the stock market seemingly going up almost every day, why own bonds?

Including an actively managed fixed income component in your investment portfolio makes sense to dampen out potential downside volatility of stock market returns, to earn more than cash in a 0% interest rate environment, and to provide a source of income to fund your withdrawals.

* 12 Mos Yield & Avg Duration calculation from MorningstarDirect as of 4/6/21. Yield is only one component of total return which combines yield plus price fluctuations. Yield also does not include management fees & expenses. Total return can be lower or higher than yield in any given period. The yield above does not represent actual W&A model returns as each investor’s returns will differ based on various factors. Past performance is not a guarantee of future results, and investments carry the risk of loss, including the risk of loss of invested capital.